The big picture reveals a risk that many Vietnamese investors have yet to price in: for the first time in nearly two years, a senior Federal Reserve official has openly discussed the possibility of raising interest rates. This signal comes at the worst possible time, as oil prices spike, US inflation resurges, and foreign capital outflows from Vietnam reach multi-quarter highs.

Beth Hammack's Market-Shaking Statement

On April 6, 2026, Beth Hammack, President of the Federal Reserve Bank of Cleveland, declared that the Fed may need to raise interest rates if inflation fails to cool down.This statement was particularly shocking because just a few months earlier, in late 2025, the Fed had cut rates three consecutive times. The federal funds rate currently sits at 3.50% – 3.75%, held steady through two consecutive meetings.

Hammack emphasized her preference for keeping rates unchanged "for quite some time," but did not rule out a rate hike if inflation proves persistent.Florida Realtors She also mentioned the opposite scenario: if high gas prices cause economic slowdown and rising unemployment, the Fed might need to cut rates instead. This is the classic dilemma of a supply-shock economy: fighting inflation while fearing recession at the same time.

The Energy Shock from the Iran Conflict

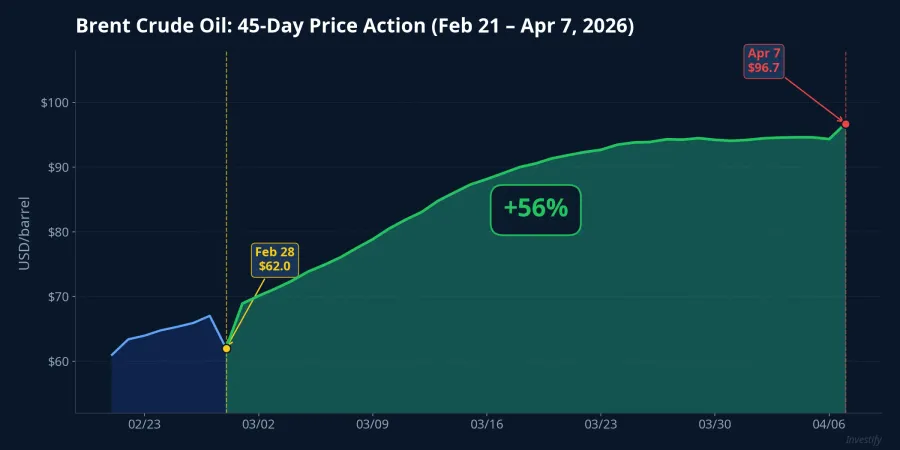

The most visible catalyst is oil prices. The Iran war and tensions at the Strait of Hormuz have pushed Brent crude from $70.77/barrel in late February to $110.19/barrel on April 7, a roughly 56% surge in just six weeks. In the past month alone, Brent rose from $92.69 to $110.19, approximately 19%.

US retail gasoline prices have also spiked to an average of $4.12/gallon, up about 80 cents in just one month.This is the sharpest increase since 2022, when the Russia-Ukraine conflict sent global energy prices to record highs. According to estimates from Goldman Sachs and BMO, every $10/barrel increase in oil can add 0.2 – 0.4 percentage points to US CPI over 6-12 months. With oil up nearly $40/barrel since the start of the year, inflationary pressure from energy is enormous.

US Inflation Comes Roaring Back

Capital flows are following a clear logic: oil prices rise → transportation and production costs climb → end-product prices increase → CPI spikes. Data from the Cleveland Fed's Nowcasting tool shows US CPI for March is estimated at approximately 3.16% year-over-year, jumping sharply from 2.4% in February. The official March CPI report will be released on April 10, and many economists forecast CPI could rise 0.8% – 1% month-over-month, the strongest monthly increase since 2022.Kiplinger

The Cleveland Fed's internal models even estimate that US inflation could hit 3.5% in April, the highest since 2024.If this scenario materializes, the inflation-taming progress the Fed has pursued for two years would be completely reversed. Pressure extends beyond energy: housing costs, transportation services, and food are all contributing to keeping core inflation elevated. The Fed raised its 2026 inflation forecast from 2.4% to 2.7% at its March meeting, but given current oil dynamics, actual figures could be significantly higher.

The Domino Chain Hitting Vietnam

USD/VND Under Dual Pressure

When the Fed signals tightening, the USD strengthens globally. The USD/VND exchange rate rose from 26,045 VND in late February to 26,331 VND on April 6, a roughly 1.1% increase over five weeks. The central exchange rate set by the State Bank of Vietnam (SBV) stood at 25,107 VND on April 6.Nhà Đầu Tư The widening gap between the central rate and actual trading rates reflects mounting depreciation pressure on the VND. If the Fed actually raises rates, the VND-USD interest rate differential would narrow further, reducing VND's relative attractiveness.

The State Bank Has Already Acted

The State Bank of Vietnam has not been sitting idle. In March, the SBV deployed forward USD sales with 180-day tenors to credit institutions with negative foreign currency positions, creating a psychological floor around the 26,850 VND level.Vietstock Simultaneously, the SBV aggressively drained liquidity through open market operations, pushing the overnight interbank rate to 11.42% per annum, nearly triple the mid-March level.Thanh Niên This is an indirect but effective tool: when VND interest rates rise, holding VND becomes more attractive, reducing the incentive to convert to USD.

Deposit Rates Climbing Fast

The direct consequence of the liquidity tightening is a sharp rise in deposit rates. Over 20 banks raised deposit rates in March, with many adjusting 2-4 times.CafeLand Savings rates at some banks have reached 9 – 9.3% per annum for long tenors.VietnamNet

For individual investors, this is a double-edged sword. On one hand, bank deposits are once again attractive with clearly positive real interest rates. On the other hand, rising capital costs weigh heavily on listed companies' profits, negatively impacting stock prices. Capital is flowing from risky assets to safe havens, and this trend will only reverse when the Fed sends clearer signals.

Foreign Outflows Surge, VN-Index Under Pressure

Against the backdrop of a strengthening USD and hawkish Fed positioning, foreign investors net sold over 32,000 billion VND in Q1/2026, exceeding the 25,900 billion VND from the same period last year.Người Quan Sát In March alone, foreign investors net sold over 16,000 billion VND on HOSE, with 18 out of 22 sessions seeing net selling and a streak of 10 consecutive sell sessions at month-end.Vietstock

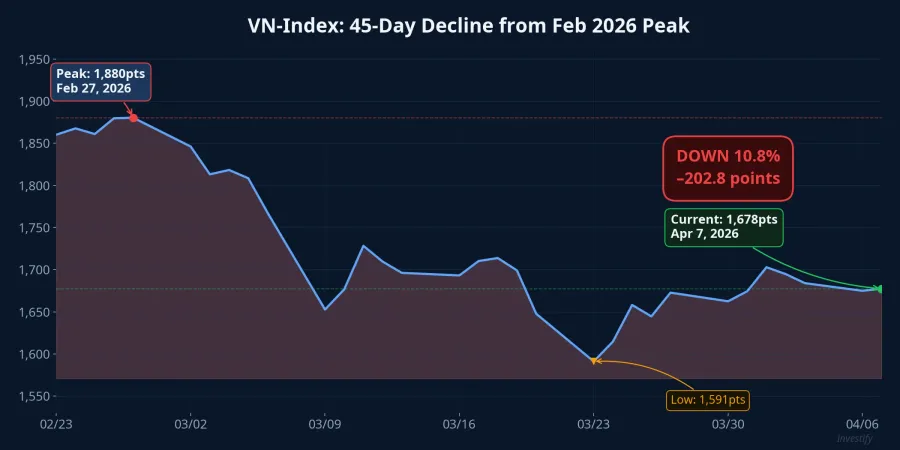

Selling pressure concentrated on large-cap stocks such as VIC, FPT, VHM, VCB, and HDB. When the USD strengthens, withdrawing capital from emerging markets to return to higher-yielding USD assets is rational behavior for international funds. The VN-Index dropped from 1,880 points in late February to 1,678 points on April 7, losing approximately 10.8% in just over five weeks — a significant decline reflecting the dual impact of geopolitical risk and macro pressure.

Three Scenarios for Investors

Base case (highest probability): Fed holds, hawkish tone. Brent hovers around $100-110/barrel, US CPI in the 3.3 – 3.6% range. The Fed keeps rates unchanged at its April 28-29 meeting but signals no cuts in 2026. USD/VND could rise another 1-2% toward the 26,500 – 26,600 range. Strategy: prioritize companies with strong cash flows, low leverage, benefiting from high energy prices (oil & gas, fertilizers). Allocate a portion to 6-12 month bank deposits to capture high rates.

Bearish scenario: Fed raises rates by 25 basis points. If US CPI exceeds 3.5% and Brent reaches $120-150/barrel, the Fed may be forced to hike for the first time in two years. USD/VND could reach 26,800 – 27,000. Defensive strategy: reduce equity exposure, increase deposits and government bonds. Avoid sectors sensitive to capital costs and energy input prices.

Bullish scenario: conflict de-escalation, oil drops quickly. If Iran tensions ease, Brent falls back to $85-90/barrel, US CPI would cool faster than expected. The Fed could return to a neutral tone, USD weakens, VND stabilizes. This would be an opportunity to buy oversold stocks, while locking in long-term deposits while rates remain high.

Two Key Events This Week

Two milestones demand close attention this week. The March US CPI report on April 10 will be the most critical test for the inflation scenario: if CPI exceeds 3.2%, markets will immediately price in higher odds of a Fed rate hike. Next, the FOMC meeting on April 28-29 will reveal whether Hammack's stance is an isolated voice or represents a broader shift within the Fed.

In Vietnam, closely monitor the SBV's actions in the foreign exchange market, interbank rate developments, and the magnitude of foreign net selling. These are the earliest indicators of how strongly external pressures are transmitting into the domestic financial market. The big picture still tilts toward caution, and in this environment, capital preservation matters more than chasing returns.