The big picture says one thing: on the morning of 8 April 2026, a chapter has truly closed. FTSE Russell published the results of its March interim review and confirmed that Vietnam is being upgraded from Frontier to Secondary Emerging Market, with an effective date of 21 September 2026. The announcement ends the delay scenarios that had unsettled the market all week and shifts the entire story onto a new track: from "will it happen" to "preparing to execute".

This is not strategically new. Back in October 2025, FTSE Russell had already issued a conditional commitment to upgrade Vietnam in September 2026, tied to the removal of pre-funding and the build-out of a failed-trade handling mechanism.LSEG But this morning is historic in terms of probability: from "will" to "has", from a hypothetical scenario to a roadmap with a calendar date attached. For the first time since 2018, when FTSE put Vietnam on its upgrade watchlist, investors can speak with certainty about a deadline.

Five milestones that define the 166-day path

To understand why the entire passive flow will not arrive in a single session, the announcement today has to be placed inside the broader timeline of ETF rebalancing. Four prior milestones plus one final date form the spine of the next 5.5 months.

October 2025 opened with FTSE's conditional commitment: the 21 September 2026 roadmap appeared in an official document for the first time. November 2025 brought the FTSE Russell FAQ that listed a tentative 28 Vietnamese stocks for inclusion in the FTSE Global All Cap Index, with bluechips such as HPG, VCB, VIC, VHM, MSN, SAB, VNM, DXG and several other large caps named explicitly.Vietnam News That list is based on end-2024 data and may shift at the formal review.

This morning, 8 April 2026, is the third milestone: the interim review confirmation. From May to August 2026, FTSE will progressively release the technical documents and the final constituent list so ETFs can prepare to rebalance. This is the stretch when market makers begin accumulating gradually, not the day before T. The final milestone, 21 September 2026, is the day Vietnam is officially counted into the FTSE Emerging basket at the regular rebalancing. It needs to be said clearly: that is the effective date, not the day capital starts arriving.

Inflow size: 5–6 billion USD, but spread across many waves

Estimates from local and foreign analysts span a fairly wide range but cluster in the 5–6 billion USD band of passive inflows over the 12–18 months following the upgrade. VinaCapital, in its October 2025 research note, estimated the upgrade could add roughly 5–6 billion USD of foreign capital to the Vietnamese market.VinaCapital Several outlets citing FTSE Russell's reference estimates also put the figure near 6 billion USD from passive funds tracking the FTSE Emerging Index.Vietnam Briefing The World Bank Group offers a more conservative range of 3–5 billion USD of portfolio inflows over the next several years.Vietnam Plus

Vietnam's expected weight in the various FTSE indexes also needs to be sized correctly: 0.34% in the FTSE Emerging All Cap Index, 0.22% in the FTSE Emerging Index, 0.04% in the FTSE Global All Cap Index, and 0.02% in the FTSE All-World Index.Vietnam News In practice, a large ETF like the Vanguard FTSE Emerging Markets fund (VWO, AUM around 90 billion USD) would allocate at the 0.22% weight — about 200 million USD — and spread its buy orders over many weeks to avoid market impact. Active funds benchmarked to FTSE Emerging may also rotate before or after T-day depending on strategy.

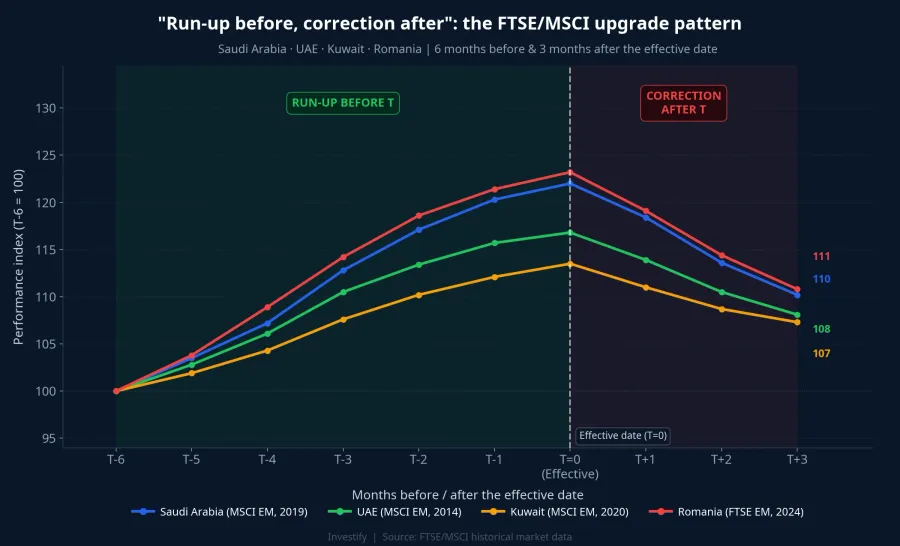

Lessons from Saudi Arabia, the UAE, Kuwait and Romania

The most recently upgraded markets produce a fairly consistent pattern: a strong run-up in the 4–6 months before the effective date, followed by a 1–3 month profit-taking correction once passive flows have largely been deployed.

Saudi Arabia (MSCI EM, 2019) rallied around 22% in the half year before T, then gave back roughly 10% in the next three months. The UAE in 2014 followed a similar script with a milder amplitude. Romania, the most recent market upgraded by FTSE (2024), also produced a "+23% then –10%" shape — almost identical to Saudi Arabia. Kuwait (MSCI EM, 2020) is the only example that held its medium-term uptrend, helped by a follow-on wave of active flows.

Four common takeaways for Vietnamese investors stand out clearly. First, the rally tends to happen before the effective date, not after. Second, the bluechips inside the basket are the clearest beneficiaries, not the broad market. Third, T-day is usually followed by a short-term correction driven by profit taking. And fourth, liquidity improves durably over the next 6–12 months as active flows arrive after passive flows.

Five things to do over the next 166 days

Based on the roadmap and the precedent markets, there are five concrete tasks individual investors should put on the calendar between 8 April and 21 September 2026.

One, track the official constituent list that FTSE will release between May and August 2026. The current 28-stock list is preliminary and may change. Two, separate the in-basket names from the broad market: the lessons from Saudi Arabia and Romania show that the headline index does not explode, but the bluechips inside the basket clearly outperform. Three, avoid FOMO buying close to T-day, because most passive flows are spread out in advance; chasing in the final week tends to land at a short-term peak.

Four, watch FTSE's next review in September 2026, where the final list is published and a few names that fail liquidity criteria may be dropped. Five, prepare mentally for the post-21/9 correction: history shows markets typically have a 1–2 month "sell-the-news" stretch, and long-term investors can use that to accumulate rather than sell along with the crowd.

The harder part is just beginning

This morning's FTSE Russell confirmation closes eight years of waiting since Vietnam first entered the watchlist. But the interesting twist is that the "recognition" part is over and the "execution" part has just begun. In the next 166 days, the market will see three sequential waves: release of the final constituent list, ETF trial rebalancing, and the effective date on 21 September.

For individual investors, discipline and a clear roadmap matter more than guessing the top. Precedent markets show that the winners are not those who buy earliest or buy most aggressively, but those who know which stocks will actually enter the basket and have enough patience to ride through the post-T correction.