What revenue reports don't tell you: 302 companies with annual revenue exceeding VND 1,000 billion have just been placed under a special tax audit. The reason? All of them reported consecutive losses in both 2023 and 2024. The list doesn't just include familiar FDI franchise names — it also features VNG, Xanh SM, MeatDeli, and Be Group. The question every investor should be asking: where did the profits actually go?

302 Companies Under Scrutiny

On March 31, 2026, the Tax Bureau issued Official Letter 1927/CT-KTr mandating a special audit of 302 companies with annual revenue of VND 1,000 billion or more that reported continuous losses throughout both 2023 and 2024.VietnamFinance The audit launched in April 2026 and must be completed before December 2026.

The list attracted market attention because it includes not only familiar FDI franchise businesses like KFC Vietnam and Lotteria, but also major names: VNG — the tech company with the most expensive stock on Vietnam's exchanges; Xanh SM (GSM) — the electric taxi brand under the VinFast/Vingroup ecosystem; MeatDeli — Masan's chilled meat brand; along with numerous others like Nguyen Kim, Vissai, and Pegas. The first 19 companies were placed under immediate audit in April 2026, including Pomina, Lotteria, and VNPT Technology.Thu Vien Phap Luat

The real risk lies here: when companies sell millions of products annually, generate trillions in revenue, yet consistently report losses, profits don't vanish on their own. They must flow somewhere.

Three Groups of "Trillion-Revenue Loss-Makers"

The phenomenon of high revenue but persistent losses concentrates in three main groups, each with different mechanisms and risk levels that investors need to distinguish clearly.

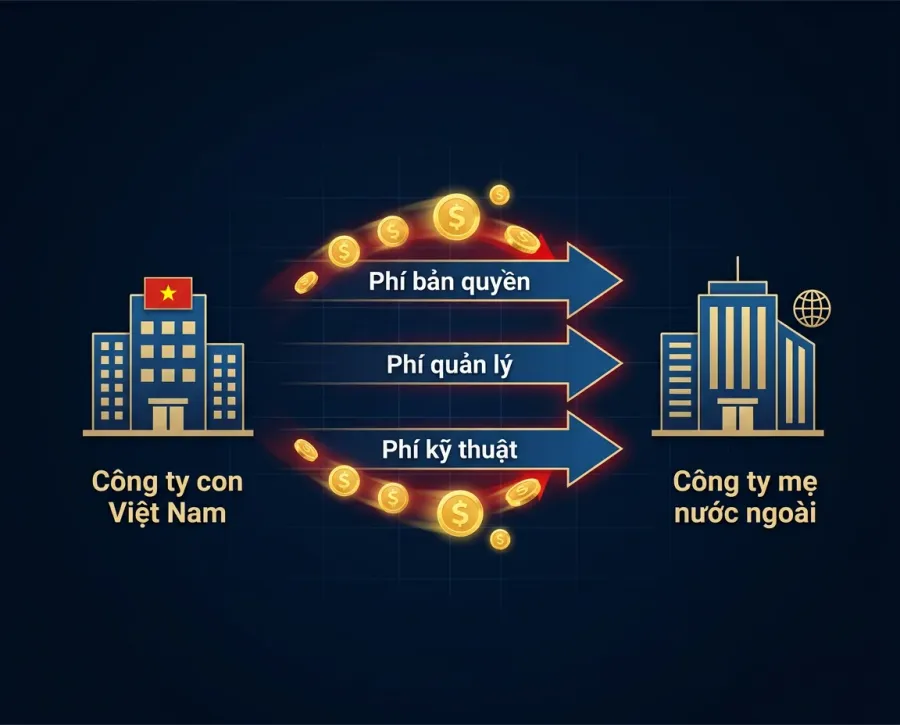

Group 1: FDI franchise businesses. KFC Vietnam is the classic example. The franchise model requires the Vietnamese subsidiary to pay a royalty fee of approximately 4% of revenue, plus 3% for regional advertising and 2% for national advertising.CukCuk In total, 9% of revenue flows to the parent company abroad before any profit is calculated, while the F&B industry's profit margin typically ranges only 5-10%. In other words, franchise fees nearly consume the entire profit margin.

Group 2: Subsidiaries within Vietnamese conglomerate ecosystems. Xanh SM (GSM) — the electric taxi brand under the Vingroup ecosystem — has contributed approximately VND 24,715 billion in cumulative revenue to Vingroup.Nguoi Quan Sat However, the manufacturing segment (including VinFast and Xanh SM) recorded pre-tax losses of over VND 33,000 billion in 2023 on Vingroup's consolidated financial statements.VnExpress This is a "cash-burning" market expansion model, similar to Grab's strategy during 2015-2020.

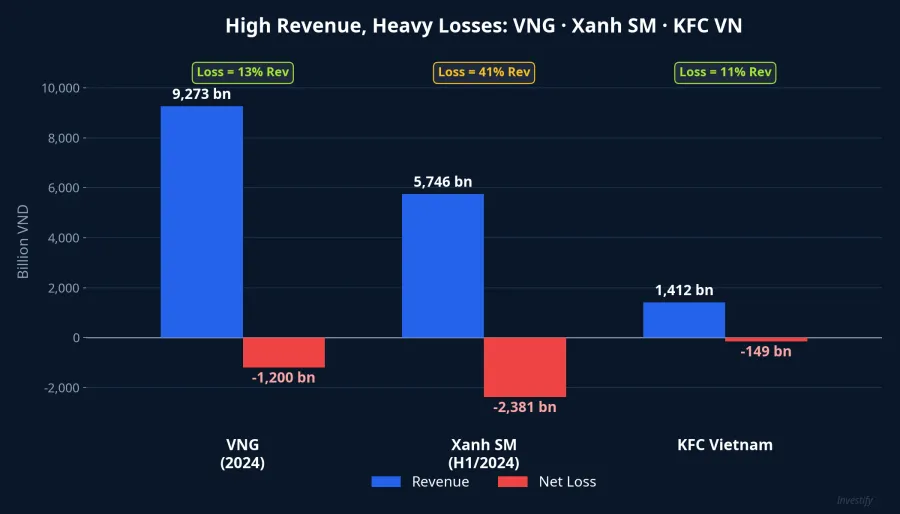

Group 3: Tech companies "burning cash" for growth. VNG (ticker: VNZ) — the company behind Zalo and ZaloPay — recorded net revenue of VND 9,273 billion in 2024, up 22% year-over-year, yet still posted a net loss of nearly VND 1,200 billion.VnEconomy This marks the third consecutive year VNG reported after-tax losses exceeding VND 1,000 billion. VNZ shares are currently trading at VND 319,900 per share — the most expensive on Vietnam's stock market — despite continuous losses.

Transfer Pricing: Where Do Profits Flow?

Transfer pricing is the practice where companies within the same group set internal transaction prices to shift profits from high-tax jurisdictions to lower-tax ones. Under Decree 132/2020/ND-CP, all related-party transactions must comply with the "arm's length principle," meaning prices must be equivalent to market conditions.Thu Vien Phap Luat

In practice, common forms in Vietnam include: royalty and franchise fees consuming 4-8% of revenue, enough to erode F&B profit margins; management fees and internal service charges (the easiest channel to abuse when there's no documentation proving actual value); inflated internal raw material purchases; and abnormally high-interest internal lending. Official Letter 1927/CT-KTr specifically emphasizes the need to scrutinize center service fees, technical service fees, and management support fees.TheLeader

What reports don't make clear: when Vietnam's corporate income tax rate (20%) exceeds that of Singapore (17%), Hong Kong (16.5%), or tax havens (0-5%), FDI companies have clear economic incentives to push costs into Vietnam and record profits elsewhere. Decree 132/2020 prescribes five methods for determining related-party transaction prices, but establishing "market prices" for internal services with no comparable external transactions is extremely challenging.

Not Everyone Is "Faking Losses"

The challenge for tax authorities is distinguishing between companies that are genuinely losing money due to legitimate business strategies and those whose losses are manufactured through related-party transaction arrangements to avoid taxes. Many cases on the 302-company list have perfectly legitimate structural reasons.

VNG is an interesting case: despite net losses, its operating profit turned positive at VND 302 billion in 2024 — losses primarily came from financial costs and investment depreciation.Bao Phap Luat Xanh SM is losing money because it's in the massive investment phase of expanding electric taxi market share. Meanwhile, Masan MEATLife (owner of the MeatDeli brand) returned to profitability from Q3/2024 after nearly two years of losses, with full-year 2024 revenue reaching approximately VND 7,650 billion, up 9.5% from 2023.Tuoi Tre

However, investors shouldn't dismiss the risk. Even when losses are genuine, being placed on a special audit list still creates short-term pressure on parent company stock prices.

How Should Investors Read Financial Statements?

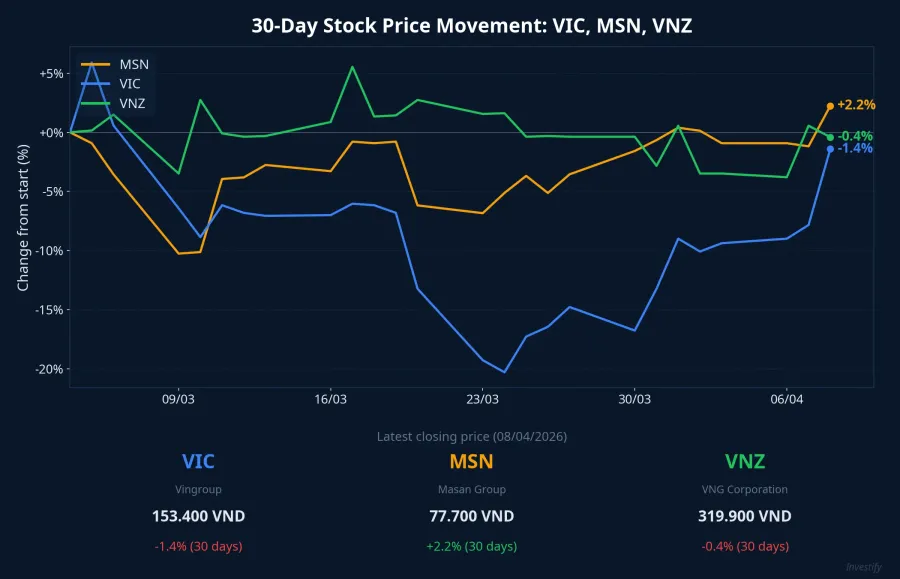

When analyzing listed conglomerates with complex subsidiary ecosystems like Vingroup (VIC — VND 153,400/share), Masan (MSN — VND 77,700/share), or VNG (VNZ — VND 319,900/share), there are five key areas investors should focus on.

Compare consolidated vs. separate financial statements. When the parent company shows strong profits but consolidated statements show losses or thin margins, that's a sign subsidiaries are dragging down results. The larger the gap, the deeper investors need to dig.

Examine related-party transaction disclosures. This is the most critical section for spotting anomalies: internal receivables and payables surging disproportionately to revenue, outsourced service costs and royalty fees exceeding industry norms, or related-party loans with abnormally high interest rates.

Cross-reference revenue with operating cash flow (OCF). If revenue is large but OCF remains negative for extended periods, this is a serious warning sign. VNG presents the opposite case: despite net losses, OCF remains positive, showing core business operations still generate cash.

Monitor management expense fluctuations. Management costs surging disproportionately to revenue scale could indicate abnormal internal management fees.

Audit opinions. Pay special attention to "emphasis of matter" paragraphs or qualified opinions related to related-party transactions.

Impact on Listed Parent Stocks

The 302-company tax audit creates both risks and opportunities for market investors.

Tax recovery risk is the biggest concern. If tax authorities determine that related-party transactions violate arm's length principles, companies could face tax recovery assessments reaching hundreds of billions of dong, directly impacting the parent company's consolidated financial statements. Reputational risk is also significant, especially given Vietnam's recent FTSE Russell upgrade to secondary emerging market status; being associated with a transfer pricing investigation could affect perception among international institutional investors.

However, if companies prove their losses are legitimate — from expansion investments, long-term strategy — the audit could become a transparency opportunity, boosting market confidence in governance quality. Looking at the 30-day price movements, VIC, MSN, and VNZ shares haven't shown a pronounced negative reaction, suggesting the market is in wait-and-see mode for audit results rather than panic.

Lessons for Investors

302 companies with trillion-dong revenue but persistent losses isn't a black-and-white story. Among them are FDI businesses with royalty structures that "consume" profits, tech startups "burning cash" for growth, and cases that require tax authorities to investigate further.

The most important lesson: don't just look at revenue or profit on the front page of financial statements. Turn to the related-party transaction disclosures, cross-reference operating cash flow with revenue, and check audit opinions. That's where the real story begins — and where the real risks, or opportunities, reveal themselves.