While investors remain fixated on the Iran conflict, Brent crude above USD 111 a barrel, or the FTSE Russell upgrade story, a far more direct variable is quietly eating into listed-company profits: interest expense. Look at the numbers: a single percentage-point rise in lending rates would add roughly VND 34 trillion in annual financing costs across HOSE and HNX, equivalent to nearly 5% of total net profit for the entire listed universe. And this is no longer a hypothetical.

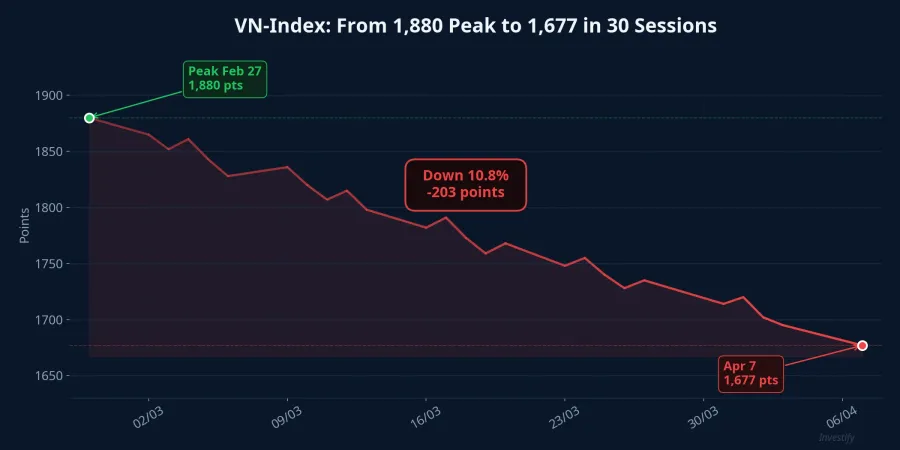

The VN-Index closed the session of April 7 at 1,677.54 points, up a marginal 0.15%, but down roughly 10.8% from the February 27 peak of 1,880. Foreign investors sold a net VND 800 billion in the session, concentrated in banks. Behind the mixed tape, the real test will be the Q1/2026 earnings season.

Rates reverse: from the 2025 floor to a three-year high

Average corporate lending rates have left behind the comfortable terrain of 2025 and are approaching a three-year high. According to State Bank of Vietnam data, the average lending rate at commercial banks is now 7.0–9.3% per year for both new and existing loans — 1 to 2 percentage points above the 6–7% level at end-2025.Doanh nhan & Cong ly

Four forces are pushing rates higher. First, credit is outpacing deposits: through end-February 2026, credit grew 1.4% versus just 0.36% deposit growth, opening a clear supply-demand gap.Nguoi Quan Sat Second, the SBV has drained more than VND 120 trillion on a net basis since the start of 2026, pushing overnight interbank rates to 5.92% and one-week rates to 6.98%.CafeBiz

Third, March 2026 CPI hit 4.65% — the highest in five years — leaving the SBV with no room to ease. Fourth, the funding race is heating up: deposit rates at some banks have jumped to 9.2% per year, dragging lending rates along.VietnamNet

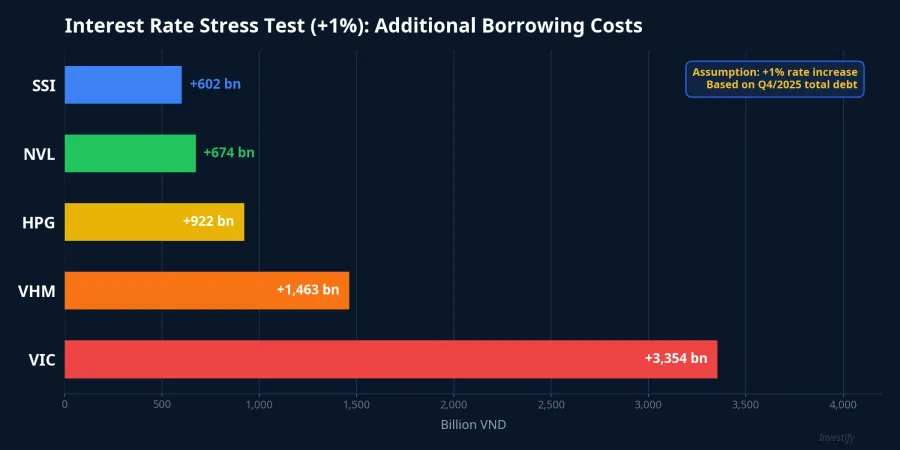

The 1% stress test: VND 34 trillion and the top five names

Total outstanding loans for HOSE- and HNX-listed companies reached roughly VND 3.39 quadrillion at the end of Q4/2025. The arithmetic is simple but weighty: a one-percentage-point rise in lending rates adds about VND 34 trillion to annual market-wide interest expense, close to 5% of total aggregate net profit. And the burden is not evenly distributed — it concentrates in a small group of heavily indebted champions.

Vingroup (VIC) tops the list with more than VND 335,420 billion in outstanding debt — the largest in the market, split between VND 114,000 billion short-term and VND 221,419 billion long-term. Each additional percentage point would lift the group's financing cost by about VND 3,354 billion per year. VIC closed April 7 at VND 143,400 (+1.27%), suggesting the market has yet to fully price in this pressure.

Vinhomes (VHM) sits right behind with VND 146,323 billion in outstanding debt, implying roughly VND 1,463 billion in additional interest expense per percentage point. For scale: VHM's interest expense in the first nine months of 2025 already reached VND 8,794 billion.VietnamBiz VHM closed April 7 at VND 115,000 (-1.71%).

Hoa Phat (HPG) carries VND 92,174 billion in debt, of which short-term debt accounts for 70% (VND 64,695 billion) — typical of a manufacturer running on working-capital cycles. An important nuance: short-term debt is far more rate-sensitive because it rolls over constantly, passing nearly the entire rate move into the P&L within a single quarter. HPG closed April 7 at VND 26,800 (-0.19%).

Novaland (NVL), with VND 67,391 billion in debt, would absorb another VND 674 billion. Notably, NVL went through a severe liquidity crisis in 2022–2023, and a renewed rate squeeze could materially slow its restructuring. NVL closed April 7 at VND 14,750 (+1.37%).

SSI — a broker rather than a property developer — still makes the top five with VND 60,161 billion in debt, nearly all of it short-term. Brokers run on leverage to fund margin lending, so rising funding costs directly compress the margin-lending spread. SSI closed April 7 at VND 27,500 (+2.04%).

Real estate: the eye of the rate storm

Listed real estate is in a uniquely fragile position. Total outstanding loans in the sector crossed VND 400,000 billion at end-2025, up more than 40% from end-2024.Vietstock In 2025 alone, real estate companies drew more than VND 276,000 billion in new loans, up 42% year on year.VietnamBiz

Lending rates for real estate also run well above the broader average: analysts expect them to reach 12–14% per year, 3 to 5 percentage points above manufacturing.VietnamBiz If sector rates rise by another percentage point, real estate alone takes on roughly VND 4,000 billion in extra annual interest expense — especially painful when inventories remain elevated and sales cash flow has yet to fully recover.

The other side: who gets to enjoy the cool breeze

Not every company suffers when rates rise. Firms with net cash (cash exceeding total debt) benefit directly from higher deposit yields, because their cash pile earns more while borrowing costs barely move.

PV GAS (GAS) stands out with the largest net cash position among non-bank HOSE listings: VND 6,876 billion in cash against just VND 2,972 billion in debt, for a net cash balance of +VND 3,905 billion. Each percentage-point rise would earn GAS about VND 39 billion more in interest income — modest in absolute terms, but crucially without any offsetting cost pressure. GAS closed April 7 at VND 77,300 (-1.53%).

Bao Viet (BVH) sits in a balanced position with VND 4,195 billion in cash versus VND 4,073 billion in debt, making it nearly immune to net rate moves. BVH closed April 7 at VND 79,900 (-1.60%). Among banks, Vietcombank (VCB) leads the whole market in net cash with roughly VND 15,543 billion; however, its business model is a special case — VCB benefits from NIM expansion but must also watch rising NPL risk.

Stocks or deposits: the allocation question

With savings rates jumping to 9.2% at some banks and 7.5–8.5% common at the Big 4, retail investors face a very practical question: does expected equity return still justify the risk? The VN-Index now sits at 1,677.54 points, down 10.8% from the February peak. If the market trades on roughly 12–13x P/E, earnings yield works out to just 7.7–8.3% — about level with a 12-month deposit, but without any mark-to-market volatility.

A reasonable allocation framework in this environment: trim high-leverage equities (especially real estate and construction); increase term deposits to lock in the rare 8–9% yields; prioritize low-debt names such as GAS, BVH, or FDI and technology companies with light balance sheets; and consider government bonds as a defensive sleeve with fixed yields.

Q1/2026 earnings will show the hand

The Q1/2026 earnings season, running from mid-April to late May, will be the real test for individual companies. Higher interest expense will flow straight into the "financial costs" line on income statements. Companies that locked in fixed long-term rates or reduced leverage early will demonstrate superior resilience. On the other hand, those reliant on floating-rate short-term debt — like HPG with 70% short-term debt, or SSI with nearly 100% — are the names to watch most closely.

Rates do not shock like a red-candle session or a geopolitical headline, but their impact is continuous and cumulative. Like water wearing down stone, every passing day chips away at profits — and it will show up clearly in the earnings reports about to hit the tape.