The big picture reveals a paradox: since the US launched military operations targeting Iran on February 28, 2026, most Vietnamese investors have focused their attention on Brent crude prices. But there's a commodity surging just as powerfully as oil that very few are watching: urea fertilizer.

Global urea prices surged to $701.25/ton at their peak in early March, up approximately 81% from the $386.75/ton level at the start of the year. This is the highest since the 2022 fertilizer crisis.VietGiaiTri The impact of this surge doesn't stop at commodity markets; it's gradually spreading into agricultural costs, livestock feed prices, and ultimately the dinner tables of tens of millions of Vietnamese households.

Hormuz blockade: fertilizer trapped in the war zone

Immediately following the military campaign, Iran responded by restricting maritime activity through the Strait of Hormuz — a shipping lane that carries roughly one-third of globally traded fertilizer and nearly half of the world's urea exports.Dan Tri Over 20 ships carrying nearly 1 million tons of fertilizer were stranded in the Persian Gulf in early March.XaLuanNews

Urea prices reacted immediately: from $465.50/ton on February 27, they jumped to $531.50/ton on March 2, a 14% surge in a single trading session. When QatarEnergy — supplier of approximately 14% of global urea demand — suspended production due to its inability to export through Hormuz, the domino effect began spreading.VietnamPlus Fertilizer plants in India and Bangladesh were forced to halt production due to ammonia shortages, while China continued tightening its fertilizer export restrictions to protect domestic supply.

On March 19, urea prices shocked the market with a 12.1% single-day surge from $610 to $684/ton — the largest daily gain since the 2022 crisis. According to JPMorgan analysts, the world currently has only about 25 days of strategic fertilizer reserves before consequences begin seriously impacting global agricultural production capacity.VietGiaiTri

Not just urea: the entire raw materials chain under pressure

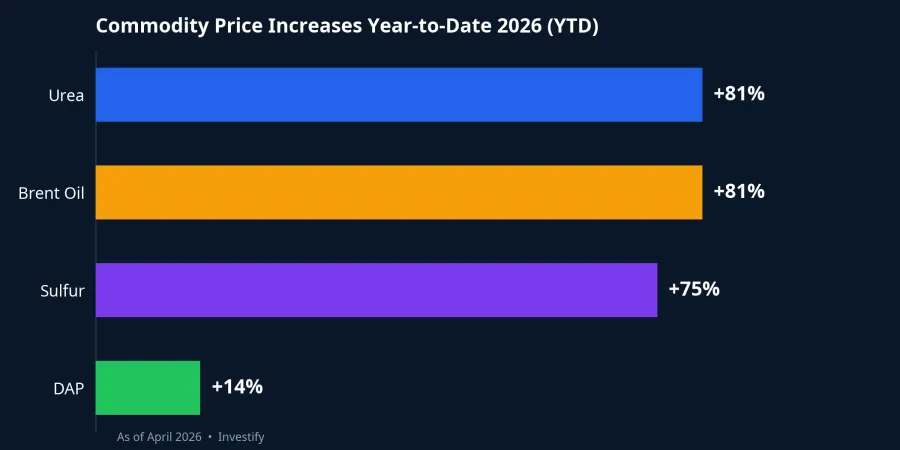

Capital flows are shifting across the entire agriculture-related commodity complex. As of early April 2026, the year-to-date (YTD) price increase picture reveals the severity of the supply shock:

- Global urea: $701.25/ton at peak, up approximately 81% YTD

- Brent crude: $110.19/barrel, up approximately 81% YTD

- Sulfur (raw material for sulfuric acid in fertilizer production): 6,733 CNY/ton, up approximately 75.6% from mid-February

- DAP (diammonium phosphate): $715/ton, up 14.4% YTD

- Vietnamese domestic urea: $752.50/ton, up approximately 85% YTD

A notable point is that Vietnamese domestic urea actually increased more than the global benchmark (85% vs. 81%), reflecting stockpiling demand and expectations of further price escalation among domestic distributors.

Vietnam is self-sufficient in urea, but vulnerable on DAP and NPK

The last time the world witnessed a similar fertilizer shock was in 2022, when the Russia-Ukraine conflict pushed urea prices above $900/ton. Unlike many regional peers, Vietnam holds a distinct advantage: its two major urea producers, Phu My Fertilizer (DPM) and Ca Mau Fertilizer (DCM), have a combined capacity of approximately 1.6 million tons of urea per year, meeting over 100% of domestic demand with room for exports.

Both companies use domestic natural gas under long-term contracts, meaning their input costs are virtually unaffected by soaring global gas prices. This is the key factor enabling significant margin expansion as selling prices follow the global market upward.

However, for compound fertilizers (DAP, NPK), Vietnam remains heavily dependent on imports. In 2025, Vietnam imported over 6 million tons of fertilizer, with China accounting for roughly half. Potash must be almost entirely imported, while declining domestic apatite ore quality forces local DAP manufacturers to increase their raw material import ratios. Global DAP prices currently stand at $715/ton; although the 14.4% YTD increase is lower than urea, the large import volumes mean significant cost pressure for farmers using compound fertilizers.

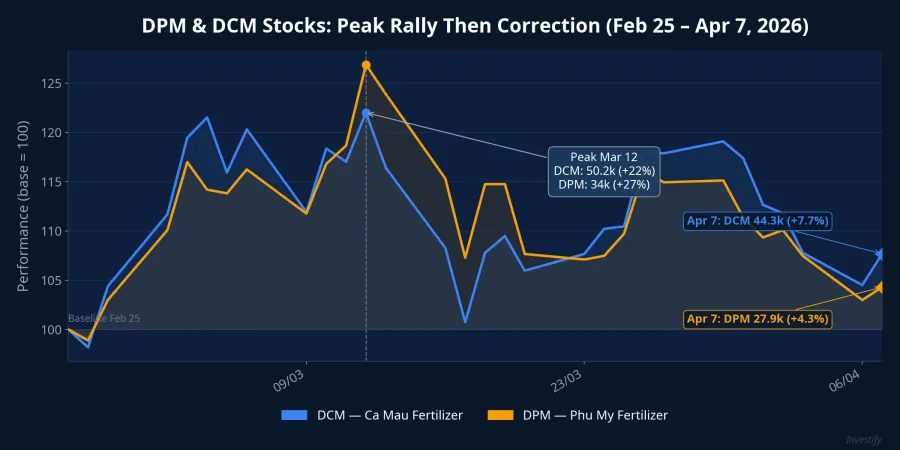

DPM and DCM: a "golden" quarter, but stocks already priced in

Securities firms forecast Q1/2026 as an explosive quarter for the two fertilizer giants. DCM is expected to achieve pre-tax profit of VND 1,306 billion, up 188% year-on-year.CafeF DPM is also forecast to see approximately 140% profit growth year-on-year.Dan Viet Both benefit from a simple formula: selling prices surge with the global market while gas input costs remain essentially unchanged thanks to long-term contracts with PVN.

Notably, DCM set its full-year 2026 after-tax profit target at just VND 1,200 billion, down 18% from the adjusted 2025 plan.Tin nhanh Chung khoan This means Q1 alone could match or exceed the full-year target. Yet the market is questioning whether elevated urea prices can be sustained post-conflict.

Looking at the price action, fertilizer stocks reacted swiftly from early March. DPM surged 27% in two weeks (from VND 26,800 on February 25 to a peak of VND 34,000 on March 12), then corrected to VND 27,950 on April 7, down 18% from the peak. DCM climbed 22% to a peak of VND 50,200 before cooling to VND 44,300, down 12% from the peak. Current prices already partially reflect expectations for a spectacular earnings quarter, narrowing further upside potential.

From fertilizer to dinner tables: the domino chain spreads

Fertilizer accounts for 20-30% of crop production costs in Vietnam. With domestic urea prices up 85% since the start of the year, although the pass-through to retail prices for farmers is delayed by existing inventory, pressure is building significantly.

The livestock industry — where feed constitutes 60-70% of production costs — faces dual pressure from both raw material prices and transportation costs. Livestock feed prices could rise 10% amid a prolonged Middle East crisis.Vietstock Since the beginning of the year, multiple companies have already raised prices by VND 100-300/kg, equivalent to VND 7,000-12,000 per 25-40 kg bag.Tin tuc Nong nghiep

During the April-June 2026 period, livestock production costs could increase 10-15%, farmer profits could decline 10-20%, and small-scale livestock farmers risk losses.Thoi bao Tai chinh Fertilizer prices typically transmit to rice and vegetable prices within a 1-2 harvest cycle. Vietnam's March 2026 CPI already reached 4.65% year-on-year — the highest in 5 years, driven mainly by energy and transportation costs.CafeF The risk of food price inflation in Q2-Q3/2026 is real as input cost pressures begin transmitting to retail prices.

Policy risk: the price intervention scenario

The government has several stabilization tools at its disposal. The 5% VAT applied since July 2025 allows fertilizer companies to deduct input taxes, reducing production costs. The Prime Minister has also issued a directive on strengthening price management and stabilization for 2026.VietnamPlus

However, this also represents the key medium-term risk for DPM and DCM. If food inflation escalates too rapidly, the government could require fertilizer companies to keep domestic selling prices below global levels, or restrict exports — similar to what China has already done. This would directly compress the profit margins the market currently expects.

Investment perspective: short-term opportunity, medium-term caution

Positive factors are undeniable: DPM and DCM clearly benefit from rising selling prices while input costs remain stable. Q1/2026 is forecast as a "golden" quarter with 140-188% year-on-year profit growth. Vietnam's urea self-sufficiency means less vulnerability compared to countries fully dependent on imports.

But the big picture reveals several risks worth weighing carefully. Stocks already rallied 22-27% before correcting, with current prices partially reflecting expectations. Policy intervention risk looms if food inflation accelerates too quickly. Most importantly: if the conflict ends or Hormuz reopens, urea prices could correct sharply — unwinding the entire windfall profit narrative.

The Iran-Hormuz conflict is creating a hidden shock that extends far beyond oil prices. From fertilizer to livestock feed, from rice paddies to dinner tables, the impact chain is spreading with a 1-2 quarter lag. Investors need to look beyond oil and gas stocks to see the full picture; because when urea rises 81%, the ultimate casualties are not traders, but tens of millions of farming households and consumers.