The big picture shows global financial markets entering their most tense phase since the US-Iran conflict erupted in late February. With less than 24 hours before Trump's latest ultimatum expires, capital flows are shifting dramatically and Vietnamese investors need a clear risk map before the April 7 morning session.

Overnight Escalation: Three New Factors

The deadline is set for 8 PM ET on April 7 — approximately 7 AM on April 8, Vietnam time — demanding Iran reopen the Strait of Hormuz or face US strikes on infrastructure.CNBC

Unlike the previous deadline (April 6) that passed without military action, this time the situation is far more dangerous due to three converging factors.

First, Iran has officially rejected the proposed 45-day temporary ceasefire. Instead, Tehran issued a 10-point response demanding a permanent end to hostilities, war reparations, and sanctions relief before reopening the strait. Trump declared the proposal "not good enough."NPR

Second, Trump's rhetoric has escalated to unprecedented extremes. He declared April 7 would be "Power Plant Day and Bridge Day, all rolled into one" for Iran, and that "the whole country could be obliterated overnight."NBC News

Third, early on April 7, IRGC intelligence chief Majid Khademi and Quds Force commander Asghar Bagheri were killed in a precision Israeli airstrike. Khademi was the number-two figure in the IRGC and one of few remaining senior commanders. This dramatically raises the probability of Iranian retaliation.Fox News

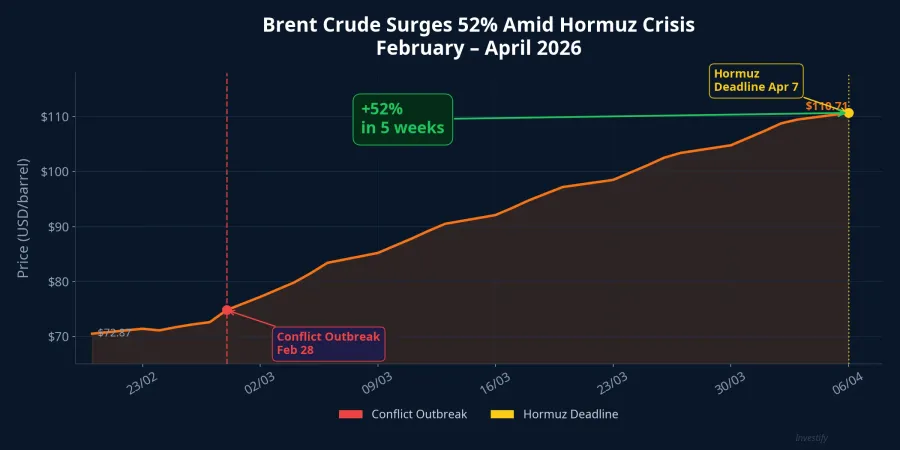

Brent Crude: From $72 to $110 in Five Weeks

The Strait of Hormuz carries approximately 20% of global oil supply. Since Iran closed the strait in late February, traffic through Hormuz has dropped an estimated 80-95%, with roughly 150 vessels stranded.

Brent crude has surged 52% since the conflict erupted, from $72.87/barrel on February 27 to $110.71/barrel on the April 6 session — the highest level since 2022. March alone saw a record monthly gain since Brent futures contracts were first introduced in 1988.CNBC

If Trump does strike Iranian energy infrastructure on the evening of April 7, Brent could quickly breach $125-140/barrel — a level CSIS estimates under a prolonged escalation scenario.CSIS

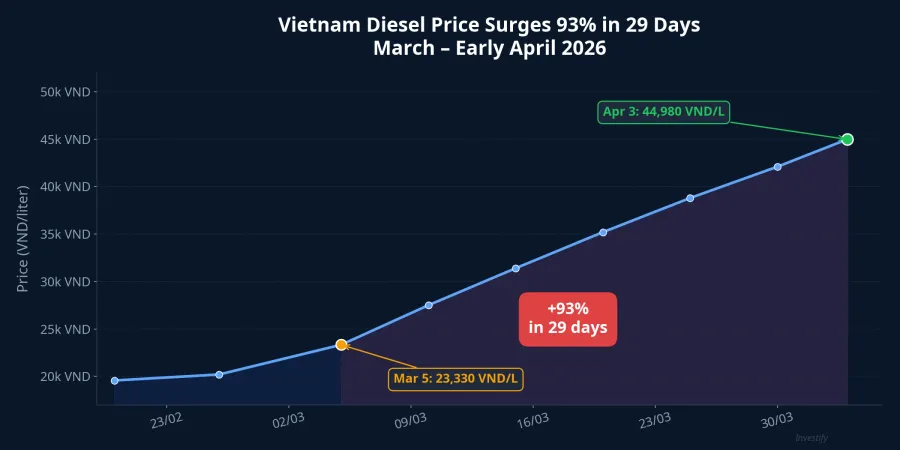

Vietnam Diesel Surges 93% in 29 Days

The most direct impact on Vietnam's economy is fuel prices. Diesel 0.001S-V jumped from VND 23,330/liter on March 5 to VND 44,980/liter on April 3, a 93% increase in just 29 days. From late February (VND 19,570/liter on February 26), the cumulative increase reaches 130%.

This is an unprecedented increase in modern Vietnamese fuel price history. Transportation costs, logistics, and the entire supply chain are under extreme pressure. Given Vietnam's manufacturing-and-export-heavy economic structure, every additional dong in diesel costs will ripple through goods prices within 2-4 weeks.

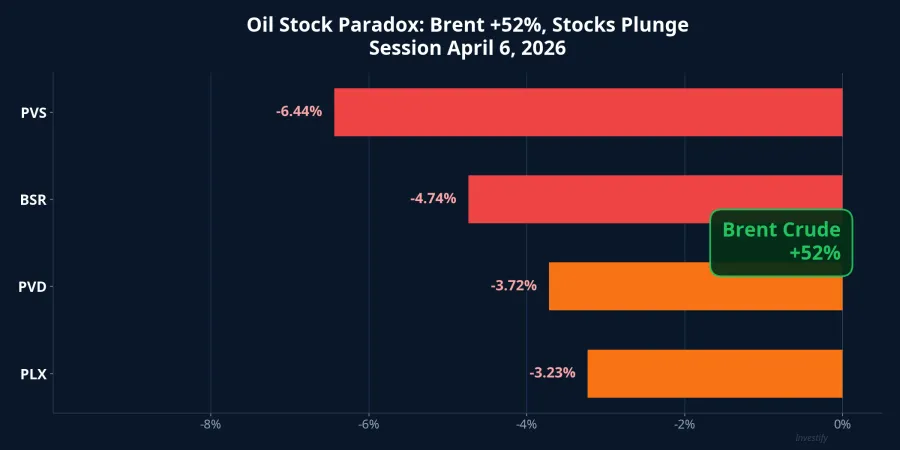

The Oil Stock Paradox: Brent +52%, Stocks Plunge

This is the most striking paradox in Vietnam's market during the Hormuz crisis. Brent surged 52%, yet oil stocks were deep in red on the April 6 session: PVS dropped 6.44%, BSR fell 4.74%, PVD declined 3.72%, and PLX lost 3.23%.

Capital flows are following risk logic, not supply-demand logic. Downstream players (PLX, BSR) face squeezed margins as input costs rise faster than regulated retail prices can adjust. BSR faces additional supply risk due to heavy dependence on Middle Eastern crude shipped through Hormuz. Foreign investors are actively reducing exposure in Vietnam, and RSI for oil stocks has fallen to the 33-39 range, indicating intense prior selling pressure.

However, upstream and services names (PVD, PVS) have better medium-term prospects if oil sustains above $100, as drilling and rig maintenance demand surges. PVD has seen two institutions registering to buy in.

Aviation and Shipping: Pressure from Both Sides

Aviation stocks are directly sensitive to Jet A1 prices. Cost per available seat-kilometer (CASK) increases approximately 0.4% for every 1% rise in fuel prices. VJC closed at VND 163,300 (up a modest 1.37% thanks to insider purchases of 2 million shares), while HVN fell 0.69% to VND 21,450. If Brent exceeds $120 and holds, airline margins will erode significantly; VJC has already dropped 23% over the past three months.

Shipping rates have surged as war risk premiums escalate (from 0.2-0.3% to 0.5-1% of vessel value). The Baltic Dirty Tanker Index rose 55% post-event. The tanker segment (PVT) should theoretically benefit from higher rates, but market-wide risk sentiment is dragging everything down. PVGas Trading has declared force majeure on LPG supplies, showing supply chain risks directly impacting corporate operations.

Gold Falls 10% Despite War

While oil surges, gold is defying its traditional safe-haven role. Gold prices have dropped 10.1% over one month, from $5,158.89/oz on March 6 to $4,637.70/oz on April 6.

The cause lies in expectations that the Fed will keep rates higher for longer due to oil-driven inflation fears. A stronger USD pressures gold — a non-yielding asset — while capital flows into oil and commodities instead. This conflict is fundamentally about energy supply disruption, not systemic financial instability, redirecting haven flows away from gold.

Three Scenarios Before the April 7 Morning Session

The VN-Index closed its latest session at 1,674.99 points, down 0.54%, caught in a compression zone between the MA50 (1,763 points) and MA200 (1,666 points) — a technical zone that typically leads to sharp breakouts when catalyzed by events. The USD/VND rate holds steady around VND 26,331, not yet reflecting significant pressure.

Scenario 1: Negotiations progress. If positive signals emerge before the deadline (Gulf states are mediating a 45-day ceasefire agreement), Brent could cool to $95-100. VN-Index could recover to the 1,700-1,750 range. Airlines and transport would be the biggest beneficiaries.CNBC

Scenario 2: Moderate escalation. Trump strikes Iranian infrastructure but with limited scope (power plants, bridges). Brent jumps to $125-140/barrel, VN-Index risks falling another 7-10% to the 1,550-1,600 range. Upstream names (PVD, PVS) may react positively short-term, but the broader market faces heavy selling pressure.

Scenario 3: Full escalation. Hormuz remains completely closed for over 2 months, Brent exceeds $150-160. VN-Index risks a deep 15-20% decline from current levels to the 1,300-1,400 range. This worst-case scenario demands maximum defensive positioning.

Strategy for Investors

Do not chase oil stocks when RSI is already in a depressed zone and net selling flows remain strong. The paradox of rising Brent but falling stock prices shows the market is pricing risk above opportunity.

Exercise caution with aviation stocks. VJC and HVN are at a crossroads: if Brent cools, these are the fastest recovery candidates; if Brent keeps rising, margins will erode.

Maintain a high cash allocation. With the deadline expiring early morning on April 8 Vietnam time, the April 7 morning session still lacks clarity on which scenario will unfold. Deploy capital defensively, prioritizing strong cash flow sectors: power, utilities, essential retail.

Monitor Asian market reactions. Asian markets traded mixed this morning, with the Nikkei 225 and Kospi slightly higher on negotiation hopes. This serves as an important reference signal for the VN-Index morning session.CNBC

This article uses market data as of the April 6, 2026 trading session. Trump's deadline expires at 7 AM on April 8, Vietnam time. Investors should continuously monitor overnight developments before making decisions.