The big picture before Monday's April 6 trading session reveals three converging currents: geopolitical tensions at the Strait of Hormuz pushing oil prices to the $110/barrel range, the State Bank of Vietnam (SBV) issuing an interest rate "brake" order, and FTSE Russell preparing to announce its mid-cycle review results tomorrow on April 7. Each event carries its own mix of opportunities and risks, and the key takeaway is that investors need a holistic view rather than reacting to each headline in isolation.

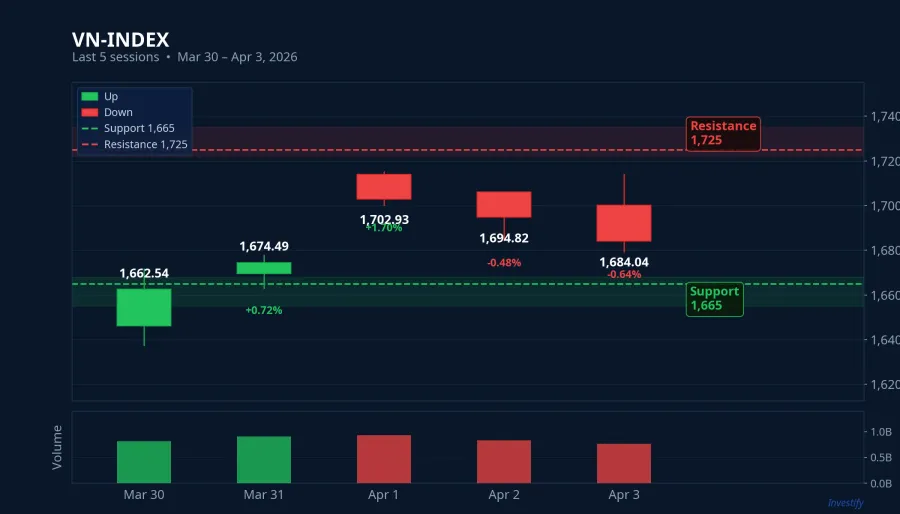

The VN-Index closed its most recent session at 1,684.04 points, down 0.64% with volume near 772 million shares. Foreign investors continued their net selling streak for 5 consecutive sessions, concentrated in banking, steel, and technology stocks. The market remains in a consolidation range of 1,665–1,725 points with visibly weakening demand.

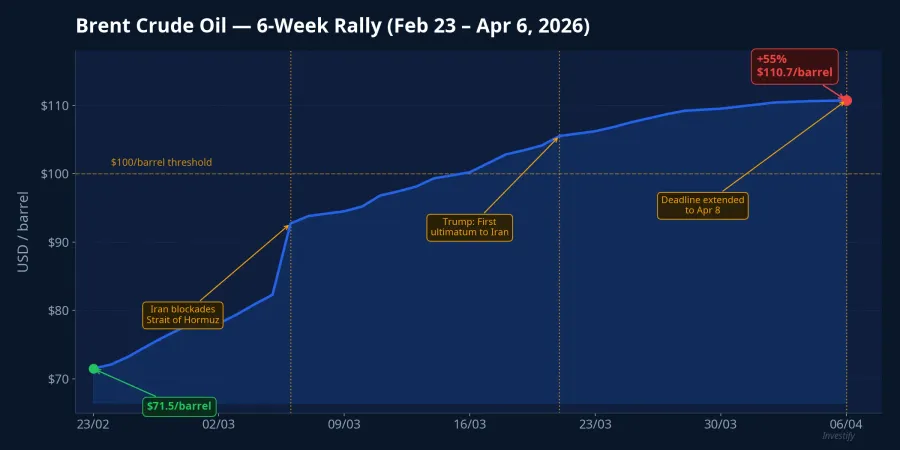

Trump Extends Iran Deadline: Brent Crude Surges Past $110

President Trump on Sunday, April 5 extended his ultimatum to Iran until Tuesday, April 8, demanding Tehran fully reopen the Strait of Hormuz or face strikes on energy infrastructure.Daily Caller This marks the third extension since the original March 21 ultimatum, signaling that Washington still prioritizes diplomacy before military escalation.

Iran has rejected the ultimatum and declared the strait will remain blockaded until it receives war damage compensation.Al Jazeera Oman is acting as a mediator with ongoing negotiations between the two sides, though no significant breakthrough has emerged.Fortune

Capital flows are shifting dramatically in energy markets. Brent crude on April 6 reached $110.71/barrel, up 1.54% from the previous session. Over 6 weeks, from $71.49/barrel on February 23, Brent has surged approximately 55%, primarily because the Strait of Hormuz — the shipping route for 20% of global oil — has been blockaded by Iran.Al Jazeera In the most recent month alone, Brent rose from $92.69 to $110.71/barrel, equivalent to a roughly 19.4% increase.

Portfolio Implications

Trump's choice to extend rather than strike reduces short-term escalation risk, but elevated oil prices continue to create sharp divergence across sectors.

Upstream oil and gas stocks are direct beneficiaries: BSR at VND 26,350 (+1.74% in the April 3 session), PVD at VND 33,600, and PVS at VND 40,400 may continue receiving support from improved profit margins tracking oil prices. Conversely, aviation and transport stocks face heavy pressure as fuel costs represent a large share of their cost structure. Oil prices sustained above $110/barrel will erode airline margins while pushing inflation risks higher — extending the trend of March CPI hitting a 5-year high.

SBV Issues Dispatch 2342: Interest Rate Brake Order

The State Bank of Vietnam has issued Dispatch No. 2342/NHNN-CSTT, directing the entire credit institution system to stabilize both deposit and lending interest rates.Thời báo Tài chính Specifically, credit institutions must strictly comply with deposit rate posting requirements and rate ceilings, while strengthening internal controls to detect violations. The SBV has committed to close monitoring and inspections of compliance.

The context behind this dispatch is clear. Since early 2026, the deposit rate race has intensified significantly, with many banks adjusting rates 4–5 times in March alone, pushing 6-month savings rates as high as 9% per annum.ZNewsCafeF The root cause lies in high credit demand and a widening credit-deposit gap, forcing banks to compete aggressively for capital.

Positive Signal but Enforcement Remains Uncertain

For banking stocks, the SBV directive helps ease concerns about the rate war eroding NIM (net interest margin). Banks with strong deposit bases like VCB (VND 57,700) and BID (VND 39,050) benefit more than smaller banks dependent on high rates to retain customers.

However, it is important to note that the dispatch is an administrative directive, not a legally binding regulation. Deposit mobilization pressure remains intense amid high capital demand, and the question is whether banks will genuinely "hit the brakes" or simply shift to gifts and deposit bonuses to circumvent the rules. If savings rates stop rising, capital outflows from equities to deposits would ease, providing psychological support for the broader market.

FTSE Russell Meets Tomorrow: Expectations vs. Reality

FTSE Russell will announce its periodic review results on April 7.Bloomberg This is a mid-cycle review following the decision to upgrade Vietnam from Frontier to Secondary Emerging Market in October 2025, with official implementation scheduled for September 2026.LSEG

Tomorrow's review will assess whether Vietnam has made sufficient progress in allowing international investors access through global brokers — a critical requirement for supporting index replication.LSEG Twenty-eight Vietnamese stocks are expected to be included in FTSE indices when the upgrade takes effect, with large-caps like VCB, BID, FPT (VND 74,000), and HPG (VND 26,650) expected to benefit from passive ETF flows.Vietnam News

The critical point investors must understand: April 7 is not when foreign capital floods in. This is merely a mid-cycle review; even with a positive outcome, passive capital flows will only materialize when the upgrade takes effect in September 2026. Investors should avoid FOMO-driven buying before the event and instead monitor actual foreign investor behavior in subsequent sessions.

Signals from Regional Markets

Asian markets opened positively this morning on April 6 as investors reacted favorably to Trump choosing extension over military strikes against Iran. South Korea's KOSPI surged 2.06% to 5,488 points, leading the region.Korea Herald Japan's Nikkei 225 rose 0.62%, led by financials.CNBC The Dow Jones closed the April 2 session at 46,504 points, down a modest 0.13%.

Positive signals from Asia may support VN-Index opening sentiment today. However, foreign capital continues its sustained net withdrawal from Vietnam, and cautious sentiment ahead of tomorrow's FTSE event may limit any liquidity improvement.

On the exchange rate front, USD/VND remains stable at VND 26,340 with no significant movement over the past week — indicating the SBV has maintained effective exchange rate control despite oil price pressures. Notably, VHM stands out with a 15.7% gain in one week (from VND 103,000 on March 30 to VND 119,200 on April 3), but foreign investors have been net selling this stock heavily — a divergence signal that warrants caution.

Action Checklist for the April 6 Session

Looking at the overall picture, the market sits in a consolidation zone with multiple variables awaiting clarity. Here are five key points to monitor:

- Energy stocks: BSR, PVD, PVS may open positively on high oil prices, but face reversal risk if Iran negotiation breakthroughs emerge.

- Banking stocks: Watch reactions to Dispatch 2342. BID and VCB may receive support if the market views the directive as stabilizing NIM.

- Prepare for FTSE day on Apr 7: Avoid chasing prices ahead of FTSE. Real capital flows arrive in September 2026.

- Maintain adequate cash allocation: VN-Index remains in the 1,665–1,725 range with no clear breakout signal.

- Monitor VHM closely: Strong gains but heavy foreign net selling; wait for trend confirmation before entering.