Many investors are counting down to April 7, 2026 as a "turning point" for Vietnam's stock market. The common expectation is that foreign capital will flood in immediately after FTSE Russell announces its review results. The reality is very different, and misunderstanding the roadmap could lead investors to buy at the top or sell at the bottom at exactly the wrong moment.

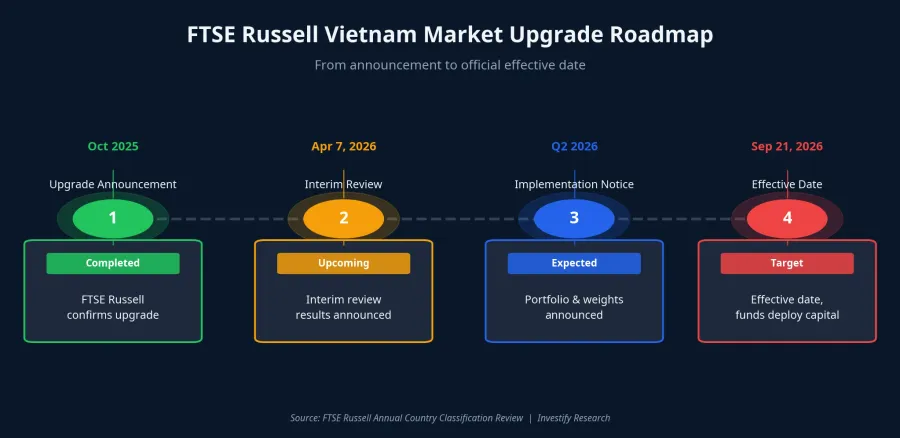

According to the official roadmap, FTSE Russell announced Vietnam's upgrade from Frontier to Secondary Emerging market status on October 8, 2025, with an effective date of September 21, 2026.LSEG The decision came with a condition: Vietnam must pass an interim review in March 2026 to confirm reform progress. The results of that review will be published on April 7. But from announcement day to the day passive funds actually deploy capital, there are still more than 5 months.

What Does FTSE Evaluate in the Interim Review?

According to official FTSE Russell documentation, the core criterion is foreign investor accessibility through global brokers (global broker access).FTSE Russell This is a key factor enabling index-tracking funds to replicate portfolios effectively.

Specifically, FTSE evaluates four criteria groups. First is trading through global brokers: foreign institutional investors can place orders through international securities firms without needing to open accounts directly in Vietnam. The Ministry of Finance issued Circular 68/2024/TT-BTC, effective November 2, 2024, allowing foreign institutional investors to buy stocks without having sufficient funds before placing orders (non-prefunded trading), removing a major barrier.Thời báo Tài chính

Second is the settlement and clearing system, evaluating the stability of the T+2 mechanism and readiness toward central counterparty clearing (CCP) standards. Third is the foreign ownership limit (FOL), focusing on mechanisms for handling situations when foreign room is full. Fourth is equal rights for foreign investors in voting, information access, and participation in corporate actions.

FTSE Russell emphasized that global broker access is not a mandatory criterion for maintaining emerging market status, but is an essential factor for supporting effective index replication and meeting the needs of the international investment community.VIR

Detailed Roadmap: From October 2025 to September 2026

The crucial point many investors miss: from April 7 to September 21, there are more than 5 months. During this period, no passive capital flows in through the upgrade mechanism. Index-tracking funds only deploy capital when the upgrade officially takes effect. Until then, the market may continue to fluctuate based on other short-term factors.

The next important milestone after April 7 is the Implementation Notice expected in Q2/2026, when FTSE publishes the official securities list and preliminary weightings. That is the real signal showing the roadmap is on track.

Record Foreign Net Selling: The Real Reasons

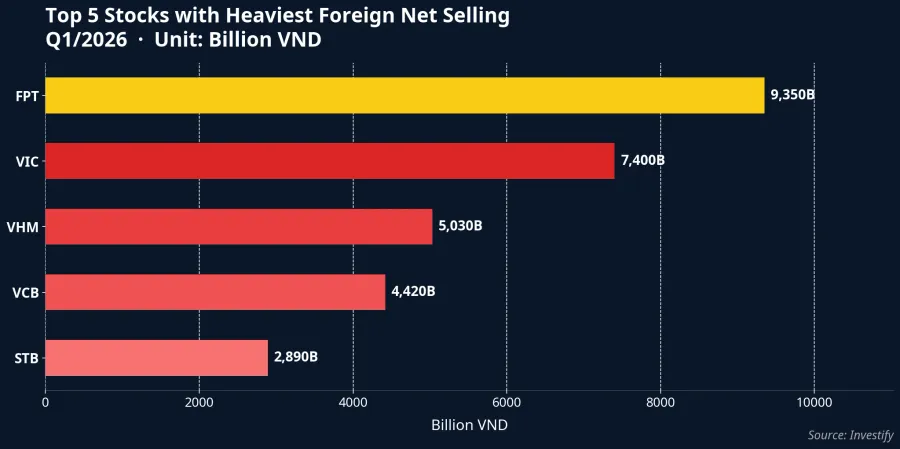

This is the question confusing many investors: Vietnam has been upgraded, so why are foreign investors selling aggressively? Foreign investors net sold over VND 32,000 billion across the entire market in Q1/2026.Người Quan Sát On HOSE alone, net selling reached nearly VND 30,400 billion, higher than the VND 25,900 billion in the same period of 2025.Tạp chí KT&TC March alone recorded over VND 18,000 billion, accounting for more than half the quarterly total, with 18 consecutive net selling sessions.DNSE

The most heavily sold stocks are all blue chips: FPT (approximately VND 9,350 billion), VIC (7,400B), VHM (5,030B), VCB (4,420B). But the reasons have nothing to do with the FTSE story.

Global capital withdrawal from emerging markets. Prolonged high interest rates in the US and Japan's monetary policy reversal have pulled capital back to these two markets. Capital outflows from emerging markets are a global trend, not specific to Vietnam.

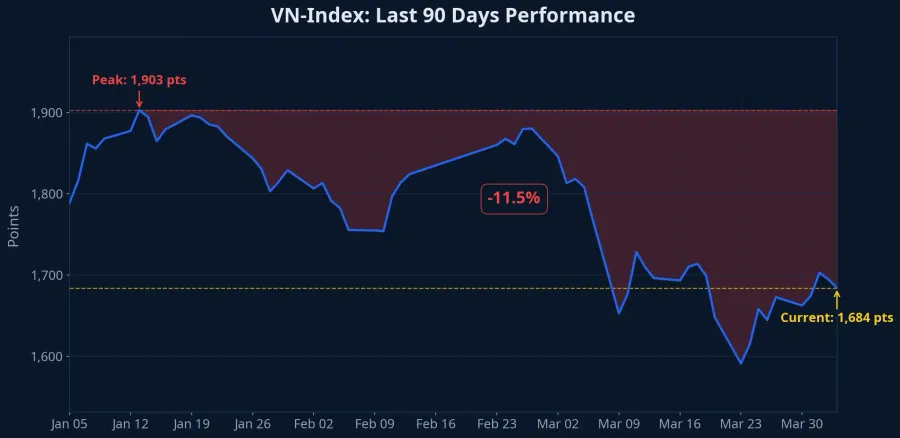

Profit-taking after the late-2025 rally. VN-Index peaked at 1,902.93 points on January 13, 2026, before declining to 1,684.04 points at the most recent session (April 4), equivalent to an 11.5% drop in less than 3 months. Blue chips that had gained 20-60% in the previous period became natural profit-taking targets.

Mechanical ETF redemptions. Several ETFs recorded strong outflows: VanEck withdrew $73.2 million, Fubon withdrew $13.7 million. The FUEVFVND fund certificate was net sold over VND 1,700 billion in March alone. This is mechanical activity, not an investment view: when investors withdraw money from ETFs, funds are forced to sell underlying stocks.

Exchange rate volatility and geopolitics. The USD/VND rate rose from 26,120 VND in late February to 26,340 VND in early April, a 0.8% increase in just over a month. Combined with Iran-US tensions and rising oil prices, hedging costs increased, reducing the attractiveness of risk assets in Vietnam.

Current foreign net selling is unrelated to the FTSE story. It reflects the intersection of global risk-off sentiment, mechanical ETF activity, and profit-taking after an extended rally.

Passive Capital Flows: How Much and When?

Estimated passive capital flows from FTSE Emerging Market index-tracking funds could reach approximately $6 billion.Vietnam Briefing Broader estimates from multiple sources suggest a wider range: HSBC projects $3.4 to $10.4 billion including both active and passive funds; the World Bank estimates approximately $5 billion short-term and up to $25 billion long-term through 2030.

Vietnam's estimated weighting in the FTSE EM All Cap index is approximately 0.4%, with 28 stocks expected to be included in the FTSE GEIS basket.VietnamNews

It's important to understand that passive funds don't "choose" to buy stocks; they are required to buy according to index weightings. When Vietnam officially enters the FTSE Emerging basket on September 21, 2026, index-tracking funds must buy at target weightings, with approximately 60% of total flows expected to deploy immediately. FTSE may split implementation into two phases (50% each) to reduce liquidity shock, with the remainder allocated gradually through rebalancing periods in Q4/2026 to Q1/2027.

Simultaneously, Frontier funds will sell their Vietnam holdings, creating a counterbalancing selling force. However, its scale is much smaller than the buying force from Emerging funds.

The 5-Month Window: Portfolio Positioning Strategy

From April 7 to September 21, 2026 is a unique period: the market has confirmed the upgrade story but large capital flows haven't arrived. VN-Index currently sits at 1,684.04 points, down 11.5% from the January 2026 peak. This could be an accumulation window for those who are patient and understand the mechanics.

Investors should focus on the 28 stocks in the FTSE GEIS basket, including prominent names like HPG, VCB, VIC, VHM, MSN, SAB, VNM.VietnamNews Prioritize stocks with high free-float and ample foreign room, since passive funds need to actually execute purchases; stocks with full foreign room or low free-float will benefit less.

The key point is not to FOMO on April 7. A positive review result doesn't mean money flows in immediately. The market may react with a "buy the rumor, sell the news" pattern. The next milestone to watch is Q2/2026, when FTSE publishes the Implementation Notice with the official list and preliminary weightings.

Regarding risks, investors should be aware of three scenarios. If FTSE determines reform progress is insufficient, the roadmap could be delayed, creating a negative shock. When Vietnam exits Frontier, Frontier index-tracking funds will sell, creating short-term pressure. And global volatility from geopolitical tensions, US interest rates, and oil prices can still overshadow the upgrade story in the short term.

Conclusion

April 7, 2026 is an important milestone in the upgrade roadmap, but it is not the day "money flows in." Foreign net selling of VND 32,000 billion in Q1 is not because of doubts about the FTSE story, but due to global capital withdrawal, mechanical profit-taking, and exchange rate volatility. The estimated $5-6 billion in passive flows will only begin arriving from September 21, 2026.

Understanding the roadmap correctly helps investors avoid FOMO on April 7, as well as avoid panic when seeing foreign net selling. Over the next 3-5 years, the FTSE upgrade will be the largest structural catalyst for Vietnam's stock market. But the opportunity belongs to those who understand the mechanics and know how to patiently wait for the right moment.