Looking at Vincom Retail's (VRE) 6,446 billion VND net profit for 2025, many investors would immediately assume a spectacular breakout year. Growth of 57.4% year-on-year, exceeding the target by 37%. But peeling back the layers of data, the real picture is considerably more nuanced.

Record Profit Driven by an Extraordinary Transaction

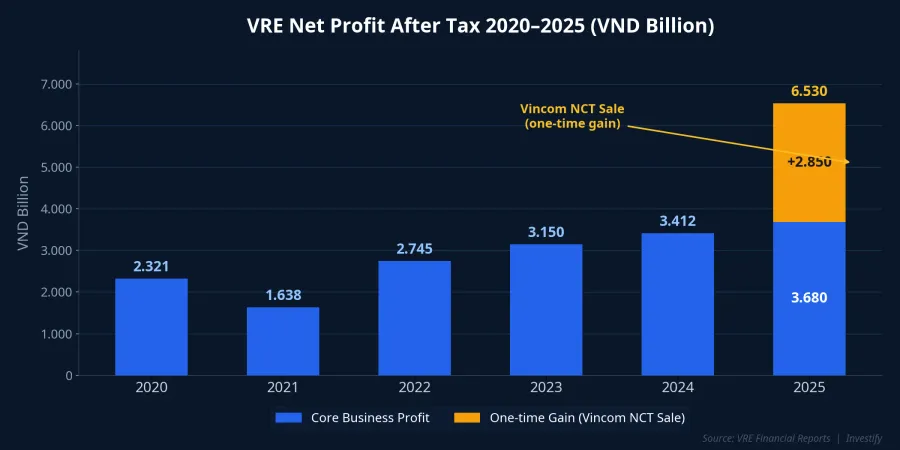

VRE closed 2025 with net profit after tax reaching 6,446 billion VND.Thanh Niên An impressive figure, but behind it lies a single transaction that contributed the bulk of the increase: the sale of Vincom Center Nguyen Chi Thanh.

In late October 2025, VRE completed the transfer of 99.99% of its stake in Vincom NCT Real Estate LLC — the entity owning this shopping center — for 3,630 billion VND.MekongASEAN According to BSC (BIDV Securities), the deal generated approximately 1,900 billion VND in one-time profit, booked in Q4/2025.CafeF

In other words, stripping out this extraordinary gain, VRE's core profit for 2025 was roughly 4,500–4,600 billion VND. Still the company's best-ever result, but the "57% growth" narrative becomes far less impressive. This is exactly why investors need to look beyond the headline into the actual cash flow dynamics.

2026 Plan: Lower but More Genuine

At the 2026 AGM, VRE set targets of 10,132 billion VND in net revenue (up 16%) and 5,375 billion VND in net profit after tax.Doanh Nhân On the surface, 5,375 billion is below the 6,446 billion achieved in 2025. However, compared against core profit excluding the one-time gain, the 2026 target actually represents roughly 15–17% growth. This is the real growth rate investors should focus on.

The 2026 revenue structure reveals a clear strategic shift. The leasing and related services segment is projected at 9,719 billion VND (up 14%), while real estate transfer revenue is just 413 billion VND. This reflects a "cleaner" VRE — one focused on recurring rental income rather than dependent on opportunistic asset sales.

However, three factors warrant attention. First, VRE plans to open only 1 new mall in 2026 (Vincom Plaza Dan Phuong, Hanoi, 25,000 m²), down from 3 new openings in 2025 — a notable slowdown in expansion pace. Second, shophouse handover at Vinhomes Royal Island and Golden Avenue (total investment over 5,500 billion VND) has been delayed from 2025 to 2026–2027. Third, operating costs across 90 malls nationwide remain under pressure from energy price volatility.

Occupancy Rate: The Real Bright Spot

What stands out in VRE's financial report is the occupancy rate. The entire system reached 88.1% at year-end 2025, up 2.7 percentage points from the prior year. Vincom Centers and Mega Malls maintained above 90%.VietnamBusinessInsider Notably, foot traffic increased 21% year-on-year, signaling a robust recovery in domestic consumption.

Additionally, VRE is developing a new format called Vincom Collection — a next-generation experiential commercial street concept with nearly 300 hectares of commercial land across Ocean City, Vinhomes Global Gate, and Vinhomes The Gallery.VnExpress If successful, this model could unlock significant new leasable floor area over the next 3–5 years.

Six Years Without Dividends: Where Is the Money Going?

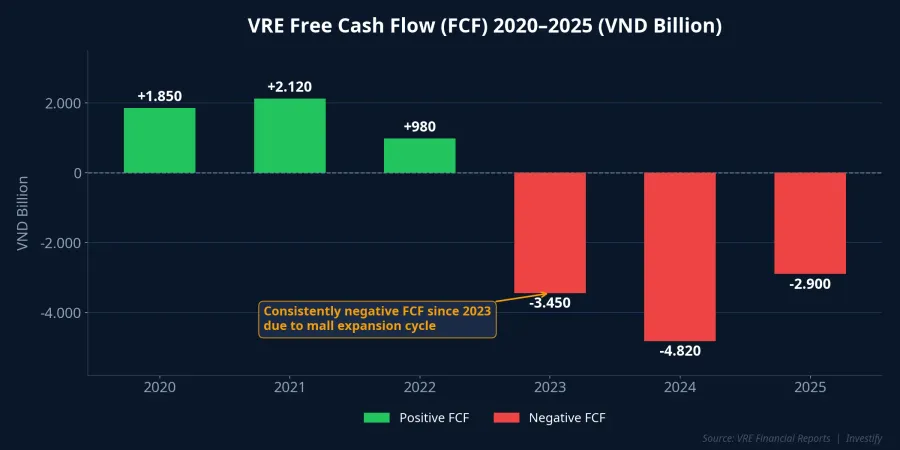

This marks the sixth consecutive year VRE has paid no dividends, retaining cumulative profits of approximately 27,000 billion VND.Doanh Nhân Free cash flow (FCF) has been deeply negative since 2023, indicating VRE is in the midst of a heavy investment cycle.

The capital is being deployed for three primary purposes: acquiring shophouses within the Vingroup ecosystem (over 5,500 billion VND at Vinhomes Royal Island and Golden Avenue), expanding leasable floor area to bring the total system to 90 malls with 1.91 million m², and funding the development of the new Vincom Collection concept.

The strategy has clear logic: building long-term income-generating assets. But for minority shareholders, waiting six years without receiving a single dividend payment is a major test of patience. The key question is when the investment cycle will end and free cash flow returns to positive territory.

VRE and the FTSE Upgrade Catalyst

VRE is among 28 stocks expected to be added to the FTSE index when Vietnam is officially upgraded to Secondary Emerging Market status in September 2026.Tin Nhanh Chứng Khoán FTSE Russell is expected to announce the phasing plan on April 7, 2026.

VRE shares rallied over 23% following the upgrade announcement in October 2025. This is a significant medium-term catalyst, as foreign capital from ETFs tracking FTSE indices will automatically flow into constituent stocks. However, investors should note that upgrade expectations have already been partially priced in.

Assessment: Value Opportunity or Growth Trap?

VRE occupies a unique position in Vietnam's commercial real estate sector. The market leader with a system of 90 malls, stable core business with double-digit growth. But investors must clearly distinguish between "headline" profit that includes one-time items and sustainable earnings.

On the positive side, occupancy rates continue to improve, rental revenue grows steadily, the Vincom Collection model opens new growth runway, and VRE directly benefits from the FTSE upgrade roadmap. On the risk side, mall expansion pace is slowing, six years without dividends creates shareholder pressure, and deeply negative free cash flow confirms VRE remains in a heavy investment phase.

The critical question for long-term investors: can the core leasing business sustain 15% annual growth once VRE has no more assets to sell? The 2026 results will be the definitive test.