As the strategic mineral war between global powers intensifies, Vietnam is quietly repositioning itself on the world's resource map. This policy shift creates rare opportunities for a small group of domestic companies, but comes with risks that investors must understand before taking action.

China Tightens Supply, Gallium Prices Surge

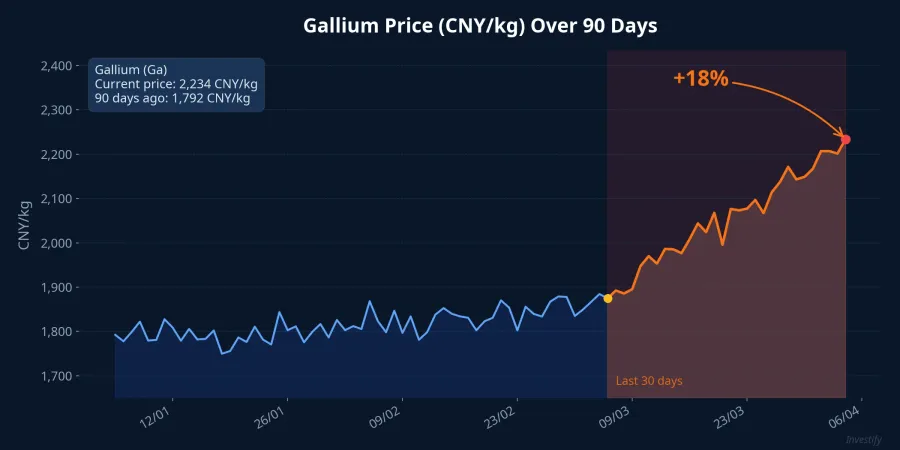

Gallium 99.99% prices in China are hovering around 2,150–2,250 CNY/kg, up nearly 18% in just one month and over 31% since the beginning of 2026. On international markets, China's FOB export price sits at approximately 400 USD/kg, reflecting the significant export licensing fees Beijing is imposing.Fastmarkets

Although China temporarily suspended its complete export ban to the US in November 2025, it maintains a case-by-case licensing regime for Gallium, Germanium, and Antimony. In other words, Beijing isn't "opening the door" but merely "cracking it open" selectively, retaining supply control as a geopolitical tool.Fastmarkets

Under this trajectory, nations dependent on Chinese minerals are forced to find alternative sources. And Vietnam is emerging as a strong candidate.

New Mining Law: Vietnam Shifts from Raw Exports to Deep Processing

The 2024 Geology and Minerals Law (No. 54/2024/QH15) together with Decree 21/2026/ND-CP has officially banned mineral exports in raw ore form, requiring companies to invest in deep processing before bringing products to international markets. Rare earths are classified as "special strategic minerals" that cannot be exported in raw form under any circumstances.VnEconomy

With substantial rare earth reserves, Vietnam is attracting attention from technology powers. South Korea has signed an agreement to establish the Korea-Vietnam Strategic Mineral Supply Chain Center, committing to transfer refining technology.Rare Earth Exchanges Japan, the US, and the EU are also accelerating cooperation.

This policy creates opportunities in two directions: companies owning mines benefit from rising mineral prices, while deep processing requirements create incentives to upgrade value chains. Over the next 3–5 years, companies investing in refining technology will gain a significant competitive edge.

Four Strategic Mineral Stocks to Watch

KSV: The Chosen One for Dong Pao Rare Earths

TKV Minerals Corporation (KSV) holds a pivotal role in the Dong Pao rare earth project in Lai Chau — Vietnam's largest rare earth deposit with reserves exceeding 11.3 million tons, accounting for more than half of the country's total rare earth reserves.Báo Đấu thầu

In 2025, KSV recorded revenue of VND 14,554 billion (up 10%) and net profit of VND 1,908 billion (up 56%). KSV has found a partner to test rare earth separation technology at Dong Pao, marking an important milestone in commercializing strategic minerals.CafeF

MSR: The World's Largest Tungsten Mine Outside China

MSR operates the Nui Phao mine (Thai Nguyen) — the world's largest tungsten mine outside China — with a fully integrated value chain through its MTC refining plant. This is exactly the "deep processing" model that the new policy envisions.

In 2025, revenue reached VND 7,443 billion, with EBITDA of VND 2,175 billion (up 22%), and tungsten alone contributing VND 4,458 billion (up 33%).VnExpress With tungsten prices remaining elevated, MSR targets profit of VND 1,700–2,500 billion for 2026.Dân trí MSR shares have surged over 96% year-to-date, reflecting strong market expectations.

HGM: A Rare Antimony Producer Outside China

HGM mines and refines Antimony at the Mau Due mine (Ha Giang) — one of the few Antimony producers outside China globally. As Beijing restricts Antimony exports, HGM becomes an alternative destination for US and EU importers. However, stock liquidity is very low (only about 2,700 shares/session), requiring investors to be patient and accept price volatility risk.

BMC: Titanium-Zircon Awaiting a Deep Processing Catalyst

BMC mines and processes Ilmenite (titanium ore), Zircon, and Rutile in Binh Dinh — raw materials for TiO₂ production (industrial pigment) and high-end ceramics. This is a debt-free company with stable operations but small scale. The raw ore export ban could serve as a catalyst if BMC invests in titanium slag plants, multiplying product value several times over. Liquidity is also very low (approximately 2,600 shares/session).

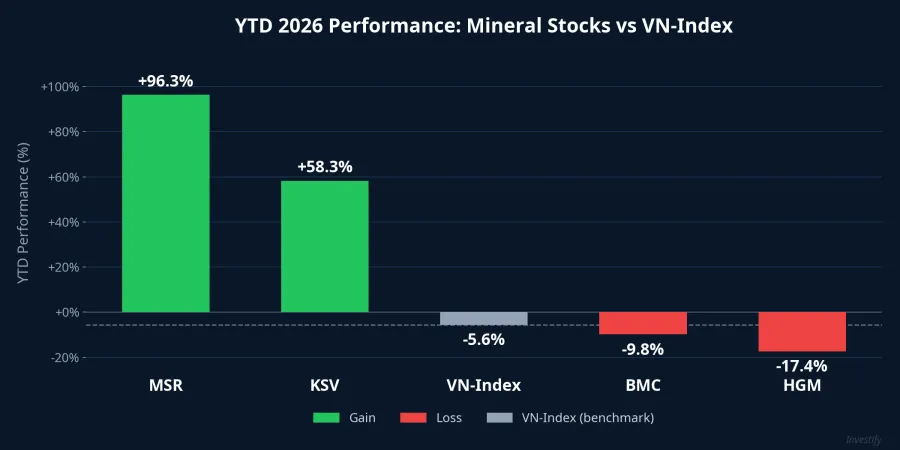

YTD 2026 Performance: Sharp Divergence

Looking at year-to-date 2026 performance, strategic mineral stocks show stark divergence. MSR leads with an impressive +96.3% gain, followed by KSV at +58.3%, while the VN-Index has declined 5.6%. Conversely, BMC (-9.8%) and HGM (-17.4%) have yet to catch the trend. This shows the market is being highly selective: only companies with deep-processed products and clear international partnerships are being repriced.

Risks to Consider

Strategic mineral stocks offer significant potential but carry substantial risks:

- Low liquidity: HGM and BMC trade only a few thousand shares per session, making large-volume trading difficult and leaving them vulnerable to price manipulation.

- Regulatory risk: Mining permit timelines (especially the Dong Pao project for KSV and the Mau Due mine extension for HGM) may face delays, directly impacting business plans.

- Commodity price volatility: Tungsten, Antimony, and rare earth prices fluctuate sharply with cycles. A 20% decline could wipe out short-term growth expectations.

- International competition: Australia, Canada, and the US are ramping up mineral self-sufficiency, potentially reducing the competitiveness of Vietnamese products in the medium term.

Long-term Outlook

Vietnam sits in a uniquely favorable position as three factors converge: abundant resources, policies prioritizing deep processing, and the supply chain diversification wave away from China. As refining plants come online and international cooperation agreements materialize, the KSV, MSR, HGM, and BMC stock group could see significant revaluation.

However, this is a story for patient investors willing to accept low liquidity and volatility in exchange for growth potential over a 3–5 year horizon.