As confirmed since October 2025, April 7, 2026 marks the final interim review before Vietnam officially joins the FTSE Global Equity Index Series as a Secondary Emerging Market.Bloomberg This is no longer a hypothetical scenario. The upgrade decision has been finalized, and the only remaining question is: which stocks will capture the largest capital flows, and over what timeframe?

This policy shift opens a rare opportunity for retail investors, but only for those who understand the timeline and capital allocation mechanics.

The 28 Stocks on the FTSE List

According to FTSE Russell's official documentation, the preliminary list includes 28 qualifying stocks, classified into three market capitalization groups.FTSE Russell

Large Cap (4 stocks): VIC (Vingroup), VHM (Vinhomes), HPG (Hoa Phat), VCB (Vietcombank). These four pillars carry the highest index weight and are expected to attract the bulk of passive capital flows. VIC and VHM represent real estate, HPG represents heavy industry, and VCB is the largest listed state-owned bank.

Mid Cap (3 stocks): MSN (Masan Group), SAB (Sabeco), VNM (Vinamilk). Three consumer brands familiar to foreign investors, with stable liquidity and a strong track record in disclosure practices.

Small Cap (21 stocks): SSI, STB, VIX, VJC, VRE, VCI, SHB, VND, GEX, KBC, KDH, FRT, DGC, EIB, HUT, DXG, DPM, PLX, PDR, DIG, KDC. This group spans multiple sectors including banking (STB, SHB, EIB), securities (SSI, VIX, VCI, VND), real estate (KBC, KDH, DXG, PDR, DIG), and industrials (DPM, PLX, DGC).

The list is based on data as of end-2024 and may be adjusted following the April 7 review results.Vietnam News

Passive Capital Flows: Scale and Allocation

The big picture reveals that expected capital flows will unfold in two distinct phases. Passive capital from ETFs and index-tracking funds alone is estimated at approximately $1.7 billion, set to flow in immediately after the upgrade takes effect in September 2026.VinaCapital Total flows including active funds could range from $3.4 to $10.4 billion according to HSBC estimates, with FTSE Russell estimating active flows alone at $5-6 billion.

Vietnam's weight in the indices has been preliminarily set at 0.34% in the FTSE Emerging All Cap and 0.22% in the FTSE Emerging Index. While these percentages appear small, the absolute size of funds tracking FTSE indices runs into trillions of dollars, meaning even 0.2-0.3% translates into billions for the Vietnamese market.

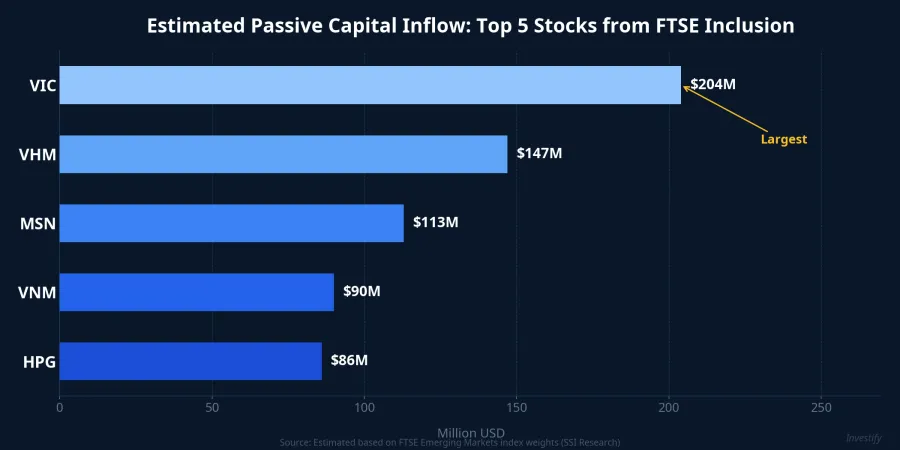

In terms of stock-level allocation, SSI Research estimates VIC will attract approximately $204 million, VHM around $147 million, MSN around $113 million, VNM around $90 million, and HPG around $86 million.SSI Research These five stocks account for the majority of passive capital flows, with the remainder thinly distributed across 23 mid-cap and small-cap names.

Disbursement Timeline: Three Critical Milestones

Over the next 3-5 months, investors need to track three decisive milestones.

April 7, 2026 is the first milestone: FTSE Russell publishes its interim review results, officially confirming the stock list for index inclusion. This is a confirmation date, not a disbursement date. Markets may experience heightened volatility around this point due to anticipation and front-running trades, but actual capital has not yet entered.

September 2026 is the second and most important milestone: the upgrade officially takes effect, and passive funds are required to deploy capital according to the new index weights. This is when the $1.7 billion in passive flows actually begins entering the market.

Subsequent rebalancing periods in Q4 2026 and 2027 will continue allocating remaining active capital as fund managers complete their evaluation and investment decisions.

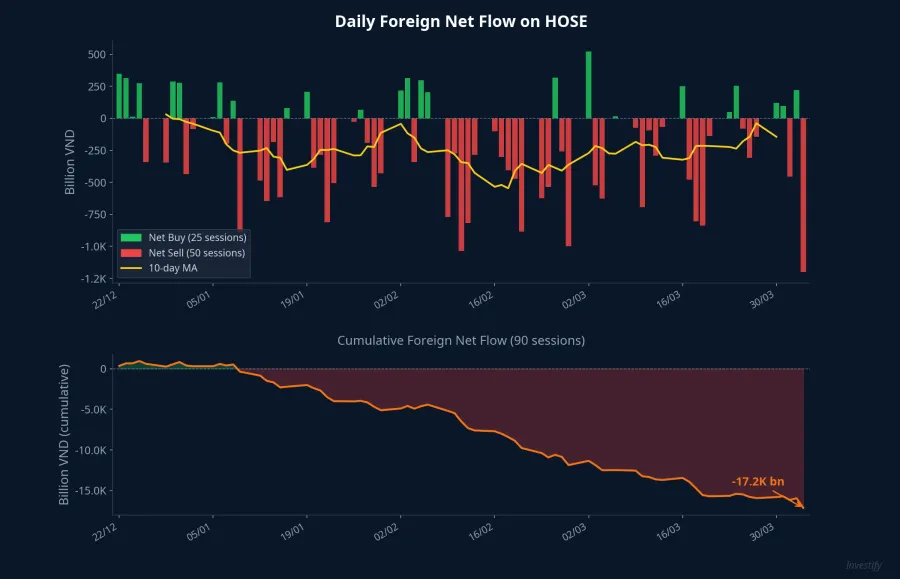

The Net-Selling Paradox: Why Foreign Investors Keep Pulling Out

One of the biggest questions right now lies in the paradox between the upgrade outlook and actual capital flows. According to Bloomberg, foreign investors have net withdrawn approximately $1.1 billion in the period leading up to April 2026.Bloomberg

Three structural factors explain this phenomenon. First, many large-cap stocks rallied strongly during 2025-2026, creating profit-taking pressure ahead of the event. Active funds tend to realize gains when prices already reflect expectations.

Second, funds tracking frontier market indices are mechanically forced to sell as Vietnam exits that classification. This is structural selling unrelated to outlook assessment. Meanwhile, emerging market index-tracking funds cannot deploy capital until the upgrade takes effect in September.

Third, the timing gap between selling and buying creates a 5-month window (April to September) during which net flows may remain negative. In other words, this is a "sell first, buy later" phenomenon that is entirely predictable under the index rebalancing mechanism.

Strategy for Retail Investors

The period from April to August 2026 represents the accumulation window for investors who understand the mechanism. While frontier funds sell and emerging funds have not yet bought in, prices of many FTSE-listed stocks may not yet fully reflect the passive capital that lies ahead.

Prioritize large-cap stocks: VIC, VHM, HPG, and VCB carry the largest index weights and are certain to remain in the index. Passive capital allocated to this group accounts for over 60% of total flows, making the price impact significantly clearer than for small-cap names.

Monitor foreign ownership room: Funds' ability to buy depends on remaining foreign ownership headroom. Stocks at or near their foreign ownership limit (such as VCB) may not see significant additional purchases despite being on the list. Investors should check foreign ownership room before banking on passive inflows.

Exercise caution with small-caps: The 21 small-cap stocks carry very small index weights. Passive capital allocated to each individual stock is negligible, so do not expect all 28 stocks to rise uniformly. The divergence will be stark.

Allocate capital over time: Avoid concentrating all capital at a single point in time. Spread purchases across the 5-month window, taking advantage of heavy foreign net-selling sessions to accumulate at more attractive price levels.

Conclusion

April 7 is not the day capital flows in — it is the day the list gets confirmed. Real money only arrives from September 2026 onward, when passive funds are required to deploy according to the new index weights. Investors who understand the timeline will use the next 5 months to accumulate strategically, rather than chasing FOMO during the announcement week. That is how to turn the upgrade policy into a genuine investment advantage.