The big picture shows the market entering a pivotal week. April 6, 2026 marks the deadline for the temporary halt on strikes against Iranian energy infrastructure, which President Trump had extended.Al Jazeera Simultaneously, the OPEC+ meeting on April 5 has been called the most consequential session since the alliance was formed.The Middle East Insider These two events will define the direction of oil prices and global capital flows for at least the next two weeks.

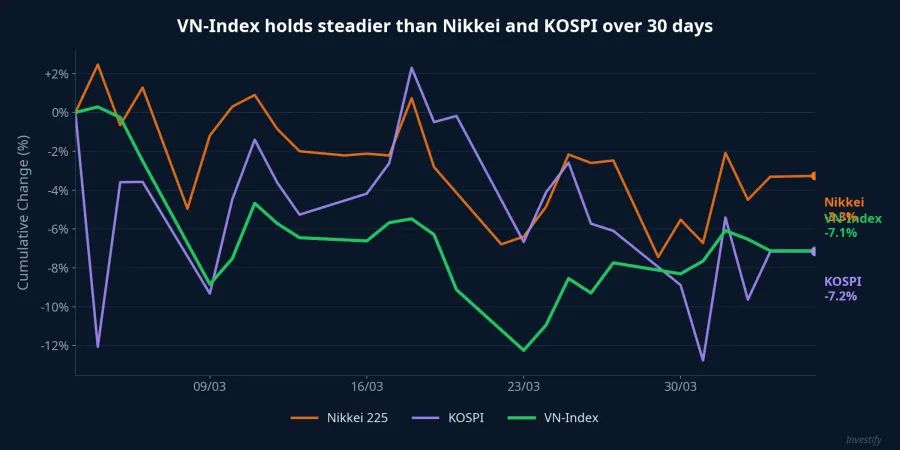

VN-Index closed the week at 1,684 points, down a mild 0.64% in the final session but still holding above the SMA20 support zone around 1,676 points. What stands out: while KOSPI and Nikkei both lost over 3% in the past month, VN-Index maintained significantly better stability.

Talks deadlocked, Hormuz still blockaded

Capital flows are reacting to every headline from the Middle East, and the latest signals are all negative. Iran rejected a 48-hour ceasefire proposal and refused to meet the US delegation in Islamabad.Townhall The 15-point peace plan presented by special envoy Steve Witkoff was dismissed by Tehran, which demands a guaranteed permanent ceasefire rather than a temporary pause in hostilities.CNBC

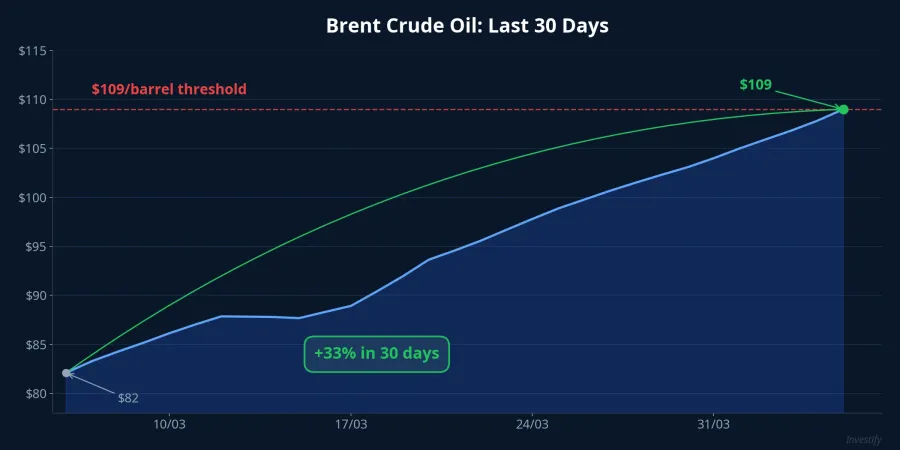

The Strait of Hormuz — a chokepoint handling roughly one-fifth of global crude oil and LNG shipments — has been blockaded by Iran since February 28. Approximately 2,000 vessels remain stranded in the area, with only a handful of ships flying Indian, Pakistani, Malaysian, and Chinese flags permitted passage.Bloomberg This is the detonator keeping Brent crude anchored at $109 per barrel — a 33% surge in just one month.

A mediating bloc comprising Pakistan, Turkey, Saudi Arabia, and Egypt is working to find an alternative venue for the next round of negotiations. However, the gap between the two sides remains vast, and each passing day pushes energy prices higher.

Three scenarios for VN-Index during April 7-11

Base case: prolonged stalemate, no escalation

Probability: highest — VN-Index range: 1,660 – 1,710 points.

Talks remain stalled, Hormuz stays partially blockaded, and Brent hovers between $105 and $115 per barrel. In this scenario, VN-Index clings to the SMA20 but lacks momentum to break above 1,710. Liquidity stays average, and investors prioritize defensive sectors while maintaining high cash allocations.

Bullish case: de-escalation signals

Probability: low to medium — VN-Index targets 1,715 – 1,740 points.

Iran agrees to meet or signals a short-term ceasefire. Brent corrects below $105. Market sentiment improves rapidly, capital rotates out of defensive positions, and large-cap stocks lead the recovery rally. Airlines and retail — the sectors most squeezed by oil prices — could see the sharpest rebounds if this scenario materializes.

Bearish case: military escalation

Probability: medium — VN-Index could test 1,610 – 1,630 points.

The April 6 deadline expires without an agreement, the US resumes strikes on Iranian energy infrastructure, and Brent surges above $120. Exchange rate pressure and inflation spike simultaneously, VN-Index breaks below the SMA20 and tests the 1,610 zone. Capital flees equities for gold and foreign currencies — the last time a comparable scenario played out was during the early days of the Russia-Ukraine conflict in 2022.

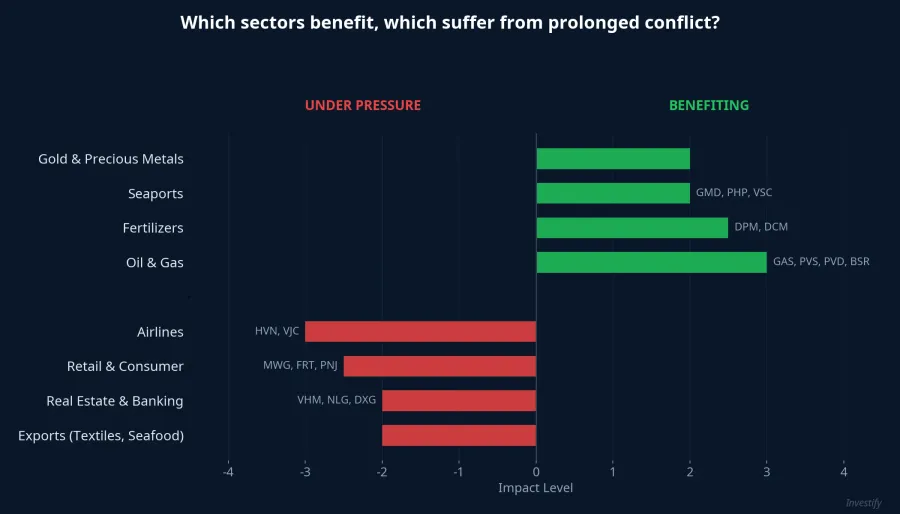

Winners and losers by sector

When conflict drags on, the sector map across Vietnam's stock market splits into sharp contrasts.

Beneficiaries include oil and gas (GAS, PVS, PVD, BSR), fertilizers (DPM, DCM), seaports (GMD, PHP, VSC), and gold. High oil prices directly boost oil and gas sector revenue; global fertilizer supply disruptions create advantages for exporters; and rising freight costs from rerouted shipping lanes mean higher cargo volumes flowing through Vietnamese ports.

Under pressure are airlines (HVN, VJC), retail and consumer goods (MWG, FRT, PNJ), real estate and banking (VHM, NLG, DXG), and textile and seafood exporters. Fuel costs account for 30-40% of airline operating expenses, so every oil price spike directly erodes profit margins. For retail, inflation drives up input costs while consumer purchasing power weakens.

The domino effect: how rising oil prices erode the economy

The big picture reveals a domino chain taking shape. Based on historical data estimates, every $10 increase in Brent crude per barrel pushes Vietnam's CPI up by 0.1 to 0.25 percentage points while dragging GDP down by 0.1 to 0.2 percentage points. In a worst-case scenario where Brent exceeds $129 per barrel, CPI could rise by an additional 0.2 to 0.5 percentage points and GDP could decline by 0.3 to 0.4 percentage points versus the base case.

The chain reaction follows a clear sequence: oil prices surge, transportation costs spike, inflation climbs, the State Bank of Vietnam faces pressure to tighten interest rates, and equity valuations get dragged down. With domestic diesel prices already up over 50% in one month, any further oil shock creates a dual squeeze on both inflation and growth.

Five signals to watch next week

Rather than predicting which scenario will unfold, investors should closely monitor five critical signals to adjust portfolios in time.

First, the April 6 deadline: will the US resume strikes on Iranian energy infrastructure, or extend the pause once more? This is the single most important short-term variable.

Second, the Brent price threshold: a break above $120 calls for immediately shifting to defensive positioning; a drop below $105 would meaningfully improve market sentiment.

Third, the OPEC+ outcome on April 5: will the alliance maintain its planned 206,000 barrels-per-day production increase, or reverse course to stabilize prices?

Fourth, foreign capital flows and exchange rates: sustained net selling pressure combined with a strengthening USD is a critical warning signal about potential capital withdrawal.

Fifth, VN-Index technical levels: support at 1,670 – 1,680 points; resistance at 1,710 – 1,730 points. A decisive break in either direction would confirm the short-term trend.

Next week will be a week where capital flows react to each news headline. Maintaining a reasonable cash allocation, prioritizing stocks with strong operating cash flow, and staying ready to adjust portfolios as scenarios shift — that is the most appropriate strategy right now.