Looking at the Q1/2026 forecasts from securities firms, the profit picture across Vietnam's banking sector is diverging at an unprecedented level. While most listed banks maintain double-digit growth, one familiar name is heading in the opposite direction: Sacombank is projected to see profits decline by 31–46% year-over-year. With earnings season kicking off the week of April 6–10, this is a critical moment for investors to reassess their portfolios.

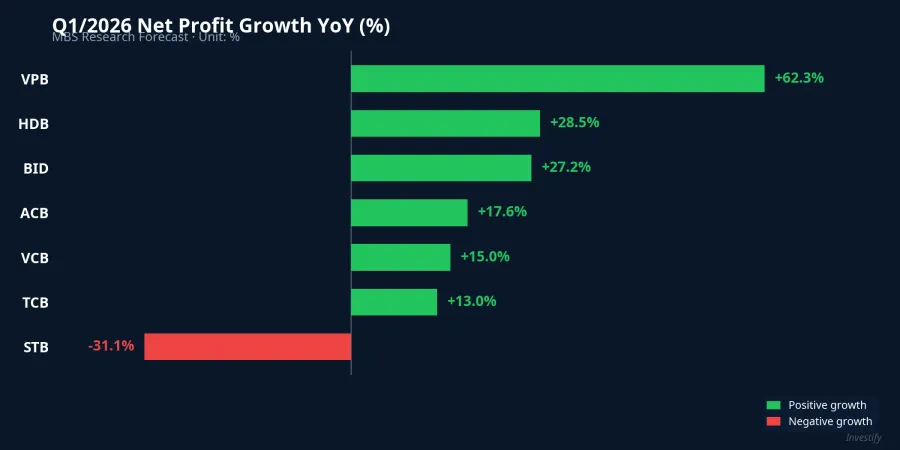

VPBank Leads Growth at +62.3%

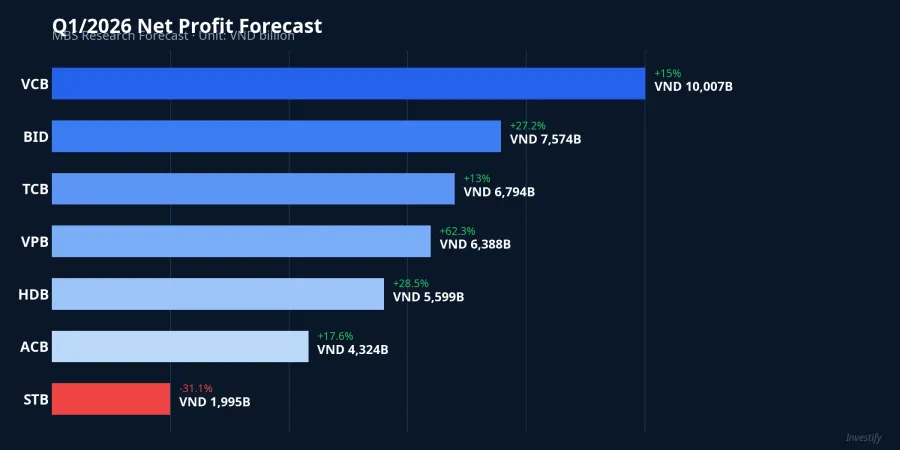

The most striking figure in the Q1/2026 forecast table is VPBank (VPB). According to MBS Research estimates, VPB's net profit could reach VND 6,388 billion, surging 62.3% compared to Q1/2025.MekongAsean

The main drivers come from two sources: net interest income (NII) rising sharply as credit expands, and provisioning costs declining significantly as FE Credit improves asset quality. This is the story the market has been waiting for over the past two years. The FE Credit investment was VPB's heaviest burden on the balance sheet, dragging down consolidated profits and causing VPB shares to trade at a discount relative to peers.

If FE Credit's recovery trend continues in subsequent quarters, VPBank will officially enter its "harvest phase" from the consumer finance restructuring process. Investors should watch two key metrics when reading VPB's Q1 report: FE Credit's non-performing loan ratio and consolidated NIM, as these will determine whether the 62% growth is sustainable or a one-time effect.

BIDV and HDBank: The 27%+ Growth Club

Right behind VPBank, two standout names are HDBank (HDB) with estimated net profit of VND 5,599 billion (+28.5%) and BIDV (BID) at VND 7,574 billion (+27.2%).CafeF

HDBank continues to benefit from strong credit growth, expected to rank among the sector's highest at over 20% expansion, alongside high net interest margins (NIM) and declining provisioning pressure. HDB's diversification strategy, combining consumer lending through HD SAISON with SME credit, is creating multiple complementary income streams.

Meanwhile, BIDV's advantage of low funding costs thanks to State Treasury deposits is showing clear results as deposit rates rise across the system. As private banks compete for deposits with higher rates, banks with cheap public-sector funding enjoy wider NIM spreads. What both banks share is a relatively modest profit base from the prior year, creating a favorable "base effect" for these impressive growth figures.

The Middle Pack: Vietcombank, ACB, Techcombank

Not every bank is posting spectacular growth, but the middle tier still shows stable health. Vietcombank (VCB) leads in absolute profit scale at VND 10,007 billion, though its growth rate sits at a modest 15%.MekongAsean This is understandable: when you're already the industry's top earner, growth naturally slows due to the large comparison base.

ACB recorded 17.6% growth with VND 4,324 billion in profit, reflecting a cautious but effective credit expansion strategy. ACB has long been known for its conservative risk management approach, prioritizing asset quality over growth speed, and this figure shows that strategy continues to deliver stable returns.

Techcombank (TCB) reached VND 6,794 billion, growing 13%, a more modest figure compared to market expectations. The main reason is NIM pressure from rising cost of funds (COF), while the prior-year profit base was already elevated. Fee income from guarantees and bancassurance shows signs of recovery, but not enough to offset cost-side pressure.

Sacombank: The Only Bank Posting a Decline

The most concerning case this earnings season is Sacombank (STB). According to SSI Research, pre-tax profit in Q1/2026 could decline by as much as 46% year-over-year.CafeF MBS Research also estimates net profit at just VND 1,995 billion, down 31.1%.MekongAsean

The core reason lies in the base effect. In Q1/2025, Sacombank recorded large extraordinary income from resolving legacy assets, including the Phong Phu Industrial Park. Without that recurring, the "true" profit reveals underlying pressure from declining NIM and rising non-performing loans. However, investors should distinguish between declines caused by one-off factors and those reflecting genuine business deterioration: Sacombank's full-year 2026 outlook remains positive thanks to plans to complete restructuring and recover legacy bad debts.

Three Lessons for Investors This Earnings Season

The Q1/2026 profit divergence offers three important lessons for bank stock investors.

First, don't paint the sector with a broad brush. The gap between VPBank (+62.3%) and Sacombank (-31.1%) spans nearly 100 percentage points within a single quarter. Picking the right stock matters far more than picking the right sector.

Second, be cautious with base effects. A sharp profit decline like STB's case may stem from extraordinary income in the prior year, not necessarily reflecting weakening business health. Conversely, unusually high growth like VPB's also needs evaluation for sustainability versus a low base.

Third, watch NIM and provisioning costs. These two factors are creating the largest differentiation among banks. Banks with stable NIM, low funding costs, and declining provisions will be the true "winners" of this reporting season. As deposit rates trend upward, competitive advantage will tilt toward banks with high CASA ratios or public-sector deposit funding.

The Q1/2026 earnings season begins the week of April 6–10. With this deep level of divergence across the sector, now is the time for investors to reassess their bank stock portfolios before the market reacts to actual numbers.