What the early April fuel price stabilization fund reports reveal isn't just negative numbers. They show that the last line of defense for domestic fuel prices is collapsing faster than anyone predicted, even after the government injected VND 8 trillion from the state budget.

With only 11 days before the fuel tax exemption policy expires on April 15, 2026, data from three major fuel distributors paints a concerning picture: the stabilization fund has nearly lost its ability to suppress prices. The real risk lies in the market not fully pricing in the worst-case scenario.

Three Distributors, Three Levels of Depletion

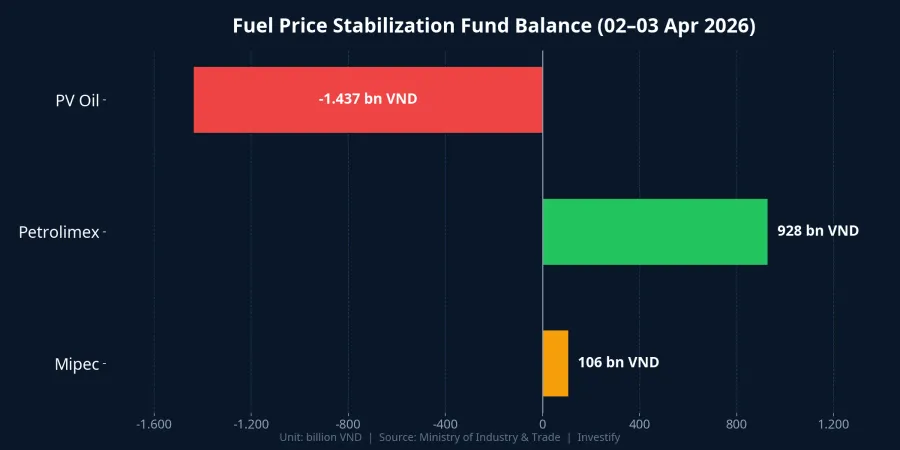

The stabilization fund balances at Vietnam's three largest fuel distributors reveal severe deterioration, particularly at PV Oil.

According to the report dated April 2, 2026, PV Oil's stabilization fund has plunged to negative VND 1,437 billion.PV Oil To put this in perspective: at the end of Q4/2025, PV Oil's fund was only negative VND 138 billion.Pháp Luật TP.HCM In just 3 months, the deficit multiplied more than tenfold. Holding approximately 20% of the national retail fuel market share, PV Oil is now subsidizing from its operating capital with zero buffer left to suppress prices.

At Petrolimex — the market leader with roughly 50% retail share — the fund balance as of April 3, 2026 stood at approximately VND 928 billion.Petrolimex Compared to nearly VND 3,088 billion at the end of Q4/2025, Petrolimex has burned through 70% of its stabilization buffer in just the first 3 months of the year. This rate of depletion signals that the cost of price suppression far exceeds the replenishment capacity.

At the smaller distributor Mipec (Military Petrochemical JSC), only about VND 106 billion remained as of April 2, 2026 — virtually depleted.Mipec

VND 8 Trillion from the Budget: Why It's Still Not Enough

On March 27, 2026, the Prime Minister signed Decision 483/QĐ-TTg, advancing VND 8 trillion from the 2025 central budget surplus to the Ministry of Industry and Trade to replenish the stabilization fund.VietnamPlus This advance must be repaid within 12 months once the market stabilizes.

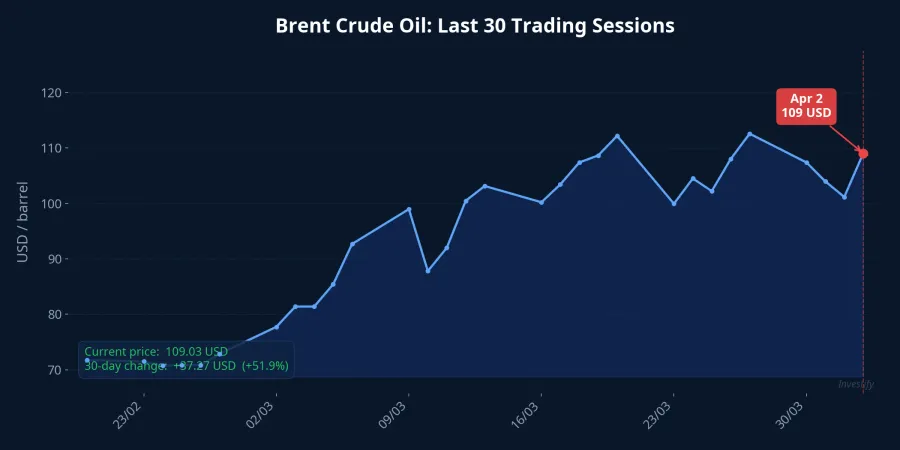

However, the reality shows that VND 8 trillion is insufficient to fill the gap. PV Oil remains over VND 1,400 billion in the red, while Petrolimex has less than VND 1,000 billion left for a distributor controlling half the market. The root cause lies in global oil prices: Brent crude has sustained above $100/barrel for weeks, hitting $109/barrel on April 2, surging due to US-Iran tensions and supply disruption fears through the Strait of Hormuz. With world oil prices at record highs, the cost of using the stabilization fund to cap domestic prices has far exceeded the ability to replenish it.

The April 15 Deadline: Will Three Taxes Return?

Decision 482/QĐ-TTg dated March 26, 2026 simultaneously reduced three taxes — environmental protection tax, VAT, and special consumption tax — to zero for gasoline, diesel, and aviation fuel, effective through April 15, 2026. This brought fuel prices down by approximately VND 5,600/liter compared to pre-exemption levels.

The Ministry of Finance has submitted a draft resolution proposing to extend the tax exemption from April 16 to June 30, 2026, for the National Assembly to consider under expedited procedures during the April 2026 session.Báo Chính phủ However, as of April 4, no official resolution has been issued. This is the biggest "blind spot" that investors need to watch carefully.

Three Scenarios and Their Market Impact

Scenario 1: Tax exemption extended to June 30, 2026 (most likely). E5 RON92 gasoline prices remain around current levels. The aviation sector benefits directly from continued low jet fuel costs. However, the central budget faces an estimated revenue shortfall of approximately VND 7,200 billion/month, creating a long-term balancing challenge for the Ministry of Finance.

Scenario 2: No extension, taxes revert to original levels from April 16. This is the worst-case scenario but cannot be ruled out. RON95 gasoline could surge above VND 30,000/liter. Distributors like PV Oil have no fund buffer to suppress prices, meaning retail prices would reflect nearly the full tax burden. Aviation stocks VJC and HVN would face heavy pressure as fuel costs account for 35–40% of total operating expenses. PLX and OIL would also be negatively affected as distribution margins get compressed under the price control mechanism.

Scenario 3: Partial extension (reduced taxes rather than full exemption). Gasoline prices increase moderately by VND 2,000–3,000/liter. Moderate pressure on both businesses and consumers, but sufficient to create sentiment effects in the market.

The Domino Effect: From Fuel Prices to Inflation

What the stabilization fund reports don't explicitly state is the cascading impact. Diesel prices have climbed to multi-year highs, directly affecting transportation and logistics costs. If fuel taxes return, the domino effect from fuel prices will spread to goods, services, and push inflation higher, especially with global oil prices still anchored above $100/barrel.

For investors, the two stock groups requiring closest attention are aviation (VJC, HVN) and fuel distribution (PLX, OIL). Under the tax extension scenario, aviation benefits directly; under the tax reversion scenario, both groups face pressure. Regardless of which scenario materializes, volatility will concentrate in the week of April 7–11 as the National Assembly convenes and makes its decision before April 15.

The real risk isn't just the negative numbers in the stabilization fund. It's that the market hasn't fully priced in the worst-case scenario, and the window to react is narrowing by the day.