The big picture reveals a rare paradox: Vietnam's economy has just posted its strongest first quarter in 15 years, yet money flow on the stock market is trapped between three opposing forces. As someone who tracks global and regional capital flows, I believe this is not a bearish signal but rather a phase where the market awaits confirmation from corporate earnings data.

A Record-Breaking Quarter: 7.83% and Beyond

The General Statistics Office has just reported Q1/2026 GDP growth of 7.83% year-on-year, the highest Q1 reading in 15 years and well above the 7.07% recorded in Q1/2025.VnExpress

The two main growth drivers were the services sector (up 8.18%, contributing 50.32% of GDP) and industry-construction (up 8.92%, contributing 44.08%). Agriculture grew a more modest 3.58% but continued to anchor economic stability. Notably, growth was not concentrated in a single sector but spread evenly, signaling genuinely robust macro fundamentals.

Beyond GDP, a string of other indicators also set records. State budget revenue reached approximately VND 820 trillion, equivalent to 32.4% of the annual target and up 10.2% year-on-year. The budget posted a VND 299.3 trillion surplus, an impressive figure given that public spending had already risen 23.1%.VnEconomy Registered FDI reached USD 15.2 billion, up 42.9%, while disbursed FDI hit USD 5.41 billion — the highest in five years.VietnamBiz International tourist arrivals also hit a new record at 6.76 million, up 12%.Vietnam.vn

FDI: Where Is the Big Money Flowing?

The structure of Q1 FDI reveals a clear trend: multinational corporations are scaling up their manufacturing footprint in Vietnam. The number of new projects rose just 6.4%, but average project size was 2.4 times larger than a year ago, meaning each new investment carried significantly more weight.

Singapore led with USD 5.32 billion (52% of newly registered capital), followed by South Korea at USD 3.68 billion. Processing and manufacturing absorbed USD 7.07 billion, accounting for 69% of total registered capital. What does this money flow tell us? Vietnam is no longer just a low-cost destination; it is becoming a critical link in global supply chains, particularly as multinationals continue to diversify production away from China.

The Paradox: Record Macro, Sluggish VN-Index

Against this glowing macro backdrop, the VN-Index closed the April 4 session at 1,684 points, down 0.64% and still well below its peak zone. The last time the economy delivered a Q1 this strong, the stock market was in a clear uptrend. This time is different, because three headwinds are holding back the money flow.

Deposit Rates Are Climbing

The deposit mobilization race has heated up significantly. More than 20 banks raised deposit rates in March, with some hiking rates two to four times in succession.VnEconomy Twelve-month deposit rates at many commercial banks now exceed 6.5–7% per annum, while some smaller banks are offering 9–10%.24hMoney When bank deposits yield this much, the flow of money into equities faces direct competition. Retail investors — who account for over 80% of trading activity — must ask themselves: why take equity risk when banks pay nearly 10%?

Fuel-Driven Inflation Surge

Q1 CPI rose 3.51%, with March CPI alone up 4.65% year-on-year — the highest March reading in five years.VOV The transportation category surged 12.85%, driven by a 29.72% spike in gasoline prices and a 57.03% jump in diesel. Energy-driven inflation creates a double bind: the State Bank of Vietnam finds it difficult to ease monetary policy to support growth, while profit margins at many companies — especially in transport and manufacturing — are being eroded.

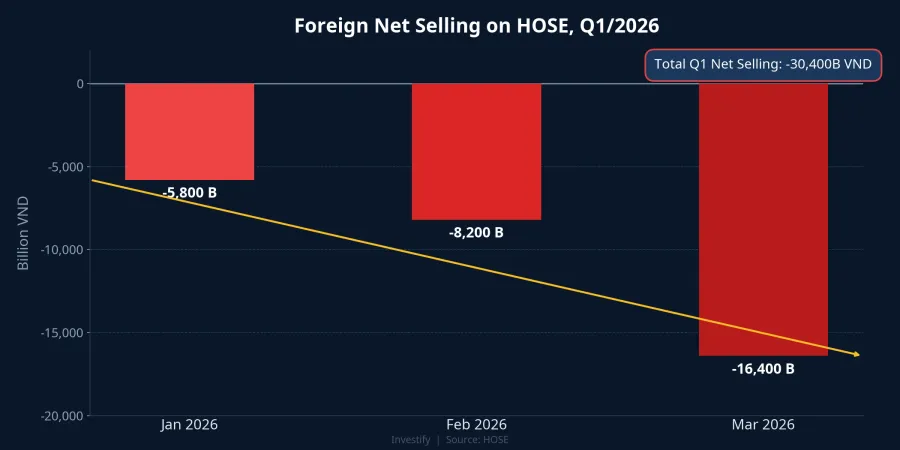

Record Foreign Net Selling

This is arguably the heaviest headwind. In Q1/2026, foreign investors net-sold approximately VND 30,400 billion on HOSE, surpassing the VND 25,900 billion recorded in the same period last year.Vietstock In March alone, 18 out of 22 sessions saw net selling, including a streak of 10 consecutive sessions at month-end. Selling pressure was concentrated in large-cap names like FPT, VIC, VHM, and VCB — the very pillars that the VN-Index needs to rally.

Capital flows are following global logic: with USD interest rates remaining elevated and the dollar strengthening, foreign capital is leaving frontier and emerging markets for safe-haven assets. Vietnam, despite its strong macro fundamentals, is caught in this broader current.

Medium-Term Opportunity: Where Will Money Flow?

Looking beyond short-term headwinds, the Q1 picture provides positive signals for several sector groups heading into Q2.

Infrastructure and construction materials: A budget surplus of nearly VND 300 trillion creates substantial room for public investment disbursement. Key projects such as the North-South expressway, Long Thanh airport, and the Ho Chi Minh City ring road are entering peak construction phases. Construction stocks (CTD, VCG, HHV) and materials stocks (HPG, KSB) stand to benefit directly from this disbursement cycle.

Industrial parks: With processing-manufacturing FDI accounting for 69% of total registered capital, industrial park real estate names (KBC, BCM, SZC, IDC) are supported by high occupancy rates and gradually rising rental prices. Every new FDI factory needs land, infrastructure, and supporting facilities. The USD 15.2 billion capital inflow will ripple into this group over the coming quarters.

Logistics: With trade up 23% and disbursed FDI at record highs, demand for seaports, warehousing, and freight transport is rising in tandem. Companies such as GMD and SCS are well-positioned to capture this long-term trend.

Waiting for Confirmation

The Q1/2026 macro picture is painting a solid foundation for growth. But the stock market does not reflect the past; it prices future expectations. And those expectations are awaiting confirmation from several key variables: whether interest rates will cool now that end-of-quarter pressure has passed, whether foreign capital flows will reverse, and whether the upcoming Q1 earnings season can generate fresh momentum.

In the near term, investors should observe rather than chase prices. But from the big-picture perspective, a 7.83% economy is not the foundation for a deep market decline. Money will find its way back once headwinds ease; and when it does, the sectors benefiting from FDI, public investment, and international trade will be the first destinations.