The big picture reveals a striking paradox: container freight rates have doubled, yet no one on the Vietnamese stock market is truly "winning." Five weeks after the Strait of Hormuz was effectively sealed off, both export and shipping stocks are under selling pressure. Capital flows are shifting defensively, and investors need to understand who's paying the highest price.

Hormuz Closure: Global Supply Chains in Turmoil

Since late February 2026, when US-Israeli forces struck Iran and the Strait of Hormuz was blockaded, the entire east-west shipping network has been severely disrupted. Drewry's World Container Index (WCI) as of April 2, 2026 stood at $2,287 per 40-foot container, with Shanghai-Rotterdam rates at $2,543 and Shanghai-Genoa reaching $3,529.Shipping Telegraph

Ships are forced to detour around the Cape of Good Hope, adding 6,000 nautical miles and approximately $800,000 in fuel costs per mother vessel voyage. Spot rates on the Far East to Northern Europe route have surged 31%, while Far East to US West Coast rates are up 29% since end of February, according to Freightos data.Freightos Carriers have imposed War Risk Surcharges ranging from $500 to $1,500 per TEU.

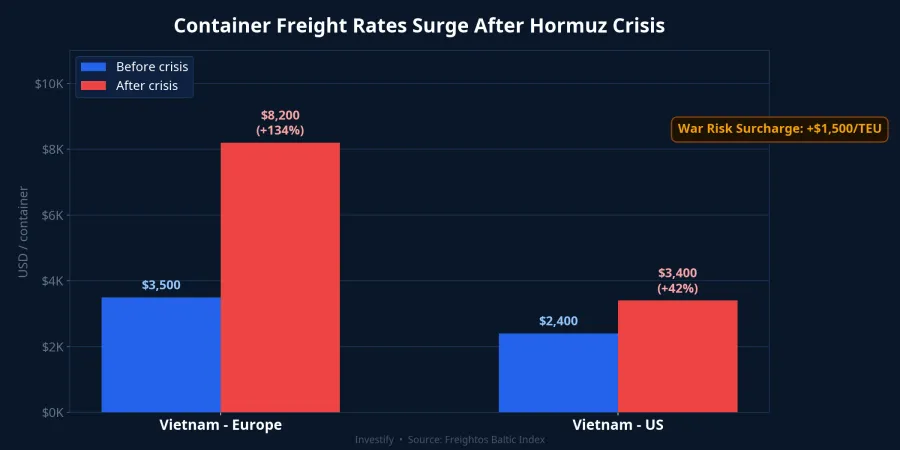

For Vietnamese exporters, the situation is even more severe. Domestic container rates on multiple routes increased by up to 25% in March 2026 alone, with rates from Hai Phong and Ho Chi Minh City ports to Europe fluctuating between $7,500–$8,200 per FEU — double the pre-crisis range of $3,500–$4,000.VietData

Export Stocks: First in the Line of Fire

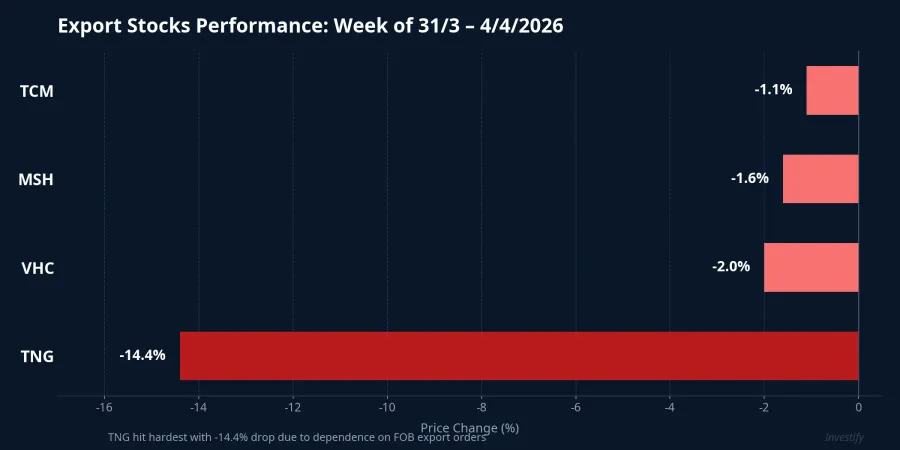

Textiles: TNG Plunges Nearly 15% in One Week

The textile sector showed stark divergence, with TNG taking the heaviest hit. The stock dropped from VND 26,400 (March 31) to just VND 22,600 (April 4), losing nearly 14.4% in a single trading week. The cause lies in TNG's business structure: the company relies heavily on FOB export orders, where the seller bears shipping costs. When container freight doubles, profit margins erode directly.

MSH (Song Hong Garment) declined more modestly, falling to VND 36,900 with a 1.6% loss. TCM (Thanh Cong Textile) shed 1.1% to VND 22,550. Both companies have more diversified client bases with higher CIF order ratios — meaning buyers bear shipping costs, providing better margin protection.

Seafood: The Thinnest Margins on the Market

Seafood is the sector most vulnerable to freight rate increases because the value of goods per container is low — logistics costs represent a large share of total product costs. VHC (Vinh Hoan) fell to VND 57,400, losing over 2% for the week. ANV (Nam Viet) eased to VND 23,600. The market is repricing both stocks on concerns that Q2 margins will be squeezed significantly.

Vietnam's seafood exports in the first two months of 2026 still grew 20% year-on-year, reaching approximately $1.7 billion.Vietnam.vn However, rising revenue doesn't necessarily translate to rising profits when logistics costs are escalating continuously.

Shipping and Ports: Winners That Aren't Really Winning

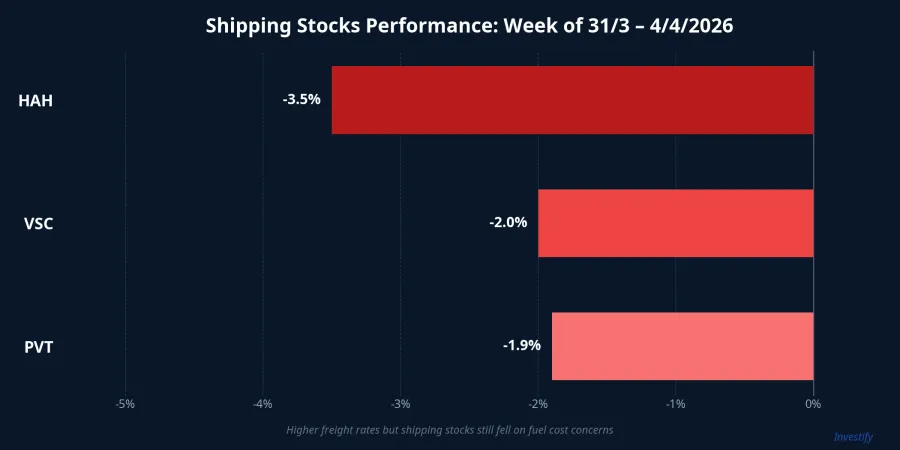

Conventional wisdom suggests shipping companies should benefit when freight rates surge, but reality is far more nuanced. HAH (Hai An Transport) — Vietnam's largest domestic container shipping company — traded flat at VND 54,600 on April 4, but had already lost 3.5% during the week. HAH enjoys short-term advantages from elevated freight levels, but faces longer-term risks: fuel costs rising with oil prices, disrupted Middle East routes, and the threat of declining export volumes if the crisis persists.Elibook

VSC (Vietnam Container Shipping) dropped 2% to VND 23,800. VSC benefits indirectly from increased warehousing and storage demand as cargo backlogs grow, but this isn't enough to offset the cautious market sentiment. PVT (PetroVietnam Transport) fell 1.9% to VND 21,150, reflecting concerns that fuel costs are eating into margins.

Outlook: Iran Rejects Negotiations, Pressure Continues

The US has demanded Iran reopen Hormuz before ceasefire negotiations can begin, but Iran has rejected this precondition.CNBC Data shows vessel traffic through Hormuz has collapsed by up to 96% compared to pre-crisis levels — from 138 ships per day to just a handful.Wikipedia

If the blockade persists, Q2/2026 will see three key trends. First, logistics costs will continue climbing as carriers impose additional emergency fuel surcharges and slow-steam to conserve fuel, further extending delivery times. Second, export margins will keep narrowing as seafood and textile companies struggle to pass costs to buyers amid competition from India and Bangladesh. Third, deeper divergence on the exchange: shipping companies with term contracts will benefit more steadily than those dependent on spot rates.

What Should Investors Watch?

The Hormuz crisis is creating a "two-sided" picture on Vietnam's stock market, but in truth both sides are under pressure. Export stocks — especially seafood and textiles — face dual headwinds from surging freight and extended delivery times. Shipping and port stocks enjoy revenue tailwinds but also face rising fuel cost risks.

With the VN-Index hovering around the 1,684-point level and no signs of de-escalation from the Middle East, investors should focus on two factors: the trajectory of US-Iran negotiations and the upcoming Q1/2026 earnings reports. Companies with CIF contract structures, high domestic revenue exposure, or margins thick enough to absorb shipping cost surges will be the most compelling names to watch during this period.