The big picture reveals a rare paradox: inflation hits its strongest level in 5 years while banks race to push deposit rates into the 8-10% per annum range. These two forces simultaneously squeeze retail investors' portfolios from both sides — real yields erode from rising prices, while capital gets pulled back toward risk-free savings channels.

March CPI Hits 5-Year High

March 2026 CPI rose 4.65% year-over-year, the highest March reading in 5 years. Month-over-month, CPI increased 1.23%, and the Q1/2026 average stood at 3.51% while core inflation exceeded the 3.63% threshold.VnEconomy

The primary driver was the transportation sector, surging 12.85% and contributing 1.28 percentage points to the headline CPI. Specifically, gasoline prices jumped 29.72% and diesel soared 57.03%, driven by global energy price increases amid geopolitical tensions in the Persian Gulf.VnEconomy

This isn't just a statistical footnote. For investors, CPI at 4.65% means real yields on every investment are being eroded far faster than six months ago. A 7% savings deposit now delivers only about 2.35% in real terms — significantly below expectations.

The Deposit Rate Arms Race

As CPI escalates, banks have intensified their deposit mobilization race with rates unseen in years. According to an early April 2026 survey, PVcomBank is offering up to 10% per annum for large deposits, while ABBank applies 9.65%. In the standard 12-month segment, MBV leads at 7.5%, followed by LPBank (7.4%) and Techcombank (7.25%). Online channels are equally competitive with HLBank offering 8% per annum.CafeBiz

Notably, the Big 4 banks — Vietcombank and VietinBank — while maintaining rates around 5.9%, have already adjusted upward 4-5 times within March alone.VietnamNet When even the most conservative giants are forced to repeatedly raise rates, capital flows are shifting dramatically. This mobilization race is pulling idle money from equities back into savings channels.

SBV: Pumping Liquidity With One Hand, Braking Rates With the Other

The State Bank of Vietnam faces its most challenging balancing act in years. In just the week of March 30 to April 3, the SBV injected 110,000 billion VND through the open market operations (OMO) channel, with the April 2 session alone seeing 32,800 billion VND in successful bids concentrated in 7-day maturities.Thời báo Tài chính

Simultaneously, the SBV issued Official Letter 2342/NHNN-CSTT requiring credit institutions to stabilize the interest rate environment, avoid market disruption, and enhance transparency in publishing deposit and lending rates.Thời báo Tài chính

This is a rare policy contradiction: one hand pumps interbank liquidity to cool short-term rates, while the other asks banks to "self-restrain" in the deposit race. The last time the SBV faced a similar dilemma was late 2022, when deposit rates also spiked to 9-10% before being cooled through administrative measures. The current signals suggest the SBV is trying to maintain system stability without triggering a sudden interest rate shock.

Winners and Losers in Dual Inflation

When inflation and interest rates rise simultaneously, sector performance diverges sharply. The hardest-hit group includes transportation and logistics, where fuel costs account for 30-40% of cost of goods sold. A 57% diesel surge nearly wipes out the thin margins of these businesses. Energy-intensive manufacturing sectors like steel, cement, and chemicals also face pressure as electricity, gas, and oil prices all rise simultaneously. Highly leveraged real estate firms face mounting interest costs, while airlines see jet fuel — 25-35% of operating expenses — spike considerably.

On the flip side, beneficiaries include banks, where net interest margins (NIM) may improve as lending rates rise faster than deposit rates. Upstream oil and gas directly benefits from Brent crude exceeding $115 per barrel. The power sector is protected by cost pass-through mechanisms, while insurance companies benefit from rising bond yields improving financial investment income.

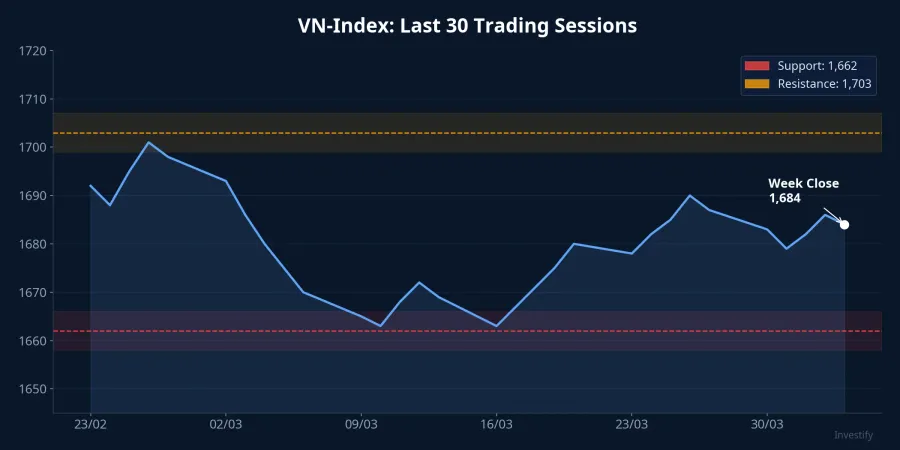

VN-Index: Fragile Recovery Amid Capital Retreat

The VN-Index closed the week of April 4 at 1,684 points, slipping 0.64% in the final session after recovering from the 1,662-point zone earlier in the week. Average daily liquidity reached only about 26,050 billion VND per session — down 10% from the prior week — signaling clear capital contraction.

Foreign investors net bought over 2,565 billion VND on HOSE, but concentrated in select stocks. Retail money flow remained active in high-liquidity names like SHB, HPG, SSI, and VIX, but leaned toward short-term trading. Defensive sentiment prevails as investors weigh equity returns against near risk-free savings rates.

Next Week: FTSE Russell and the Capital Allocation Dilemma

On Monday April 7, FTSE Russell announces its market classification review results. Even in the most optimistic scenario — Vietnam upgraded to Secondary Emerging Market — new ETF flows would face the gravitational pull of 8-9% risk-free savings rates.

Retail investors now face a very real choice: savings deposits at 7-8% with virtually no risk, versus equity returns that may not adequately compensate for the risk premium amid surging inflation. In this environment, several strategies deserve consideration:

- Reduce margin leverage, increase cash or short-term deposit allocations to capitalize on elevated rate levels.

- Prioritize stable cash-flow stocks with low energy cost sensitivity: large banks, insurance, utilities.

- Avoid bottom-fishing in transportation and highly leveraged real estate while the interest rate trend remains upward.

Capital is flowing decisively from risk toward safety. Inflation from both sides — prices and interest rates — is stress-testing every investment portfolio. Capital preservation, in this phase, may be more important than chasing returns.