On April 2, 2026, General Secretary Tô Lâm signed Resolution No. 18-KL/TW at the Second Plenum of the 14th Party Central Committee. The document sets the direction for economic development during 2026–2030, targeting average GDP growth of 10% or higher per year. This policy simultaneously opens four channels of impact on the capital market, issued just five days before FTSE Russell announces its interim review results on April 7.Bloomberg

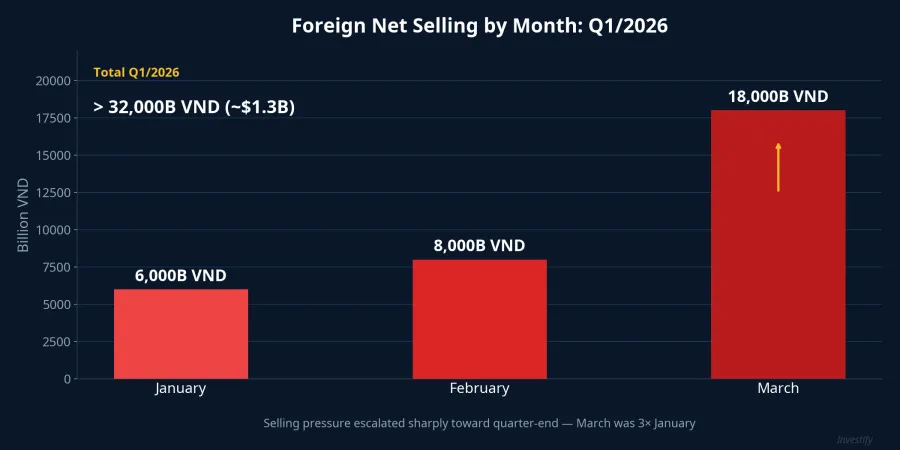

This marks a rare moment of "policy convergence": the Party's highest-level directive and international standards point in the same direction. The VN-Index closed at 1,684 points on April 3, down 0.64% amid weak liquidity and foreign net selling exceeding VND 32,000 billion in Q1/2026.Người Quan Sát However, the policy landscape is opening opportunities for investors who position themselves in the right sectors.

Stock Market Upgrade: Securities Firms and Blue Chips

Resolution 18 explicitly requires: "Implementing solutions to upgrade the stock market; issuing special and superior mechanisms and policies to enhance the effectiveness of the International Financial Center."Government Portal

This is not the first time a market upgrade has been mentioned, but it is the first time a Central Committee document — not a government resolution or a ministry circular — has confirmed this target. This means the entire political system will mobilize behind it, not just the Ministry of Finance or the State Securities Commission.

On April 7, FTSE Russell will announce its interim review, the final checkpoint before officially classifying Vietnam as a Secondary Emerging Market from September 2026. According to FTSE Russell documents, 28 Vietnamese stocks have been preliminarily identified for the FTSE Global All Cap Index, including 4 large-caps (VIC, VHM, HPG, VCB), 3 mid-caps (MSN, SAB, VNM), and 21 other tickers such as SSI, VND, STB, and VJC.Vietnam News

Direct beneficiaries: SSI, VND, HCM — securities firms that benefit doubly from rising liquidity and foreign capital inflows. SSI has proposed increasing its charter capital to VND 30,000 billion to prepare for the upgrade. When the market gets upgraded, securities firms serve as the "gateway" for new capital flows, with brokerage and margin lending revenues rising accordingly.

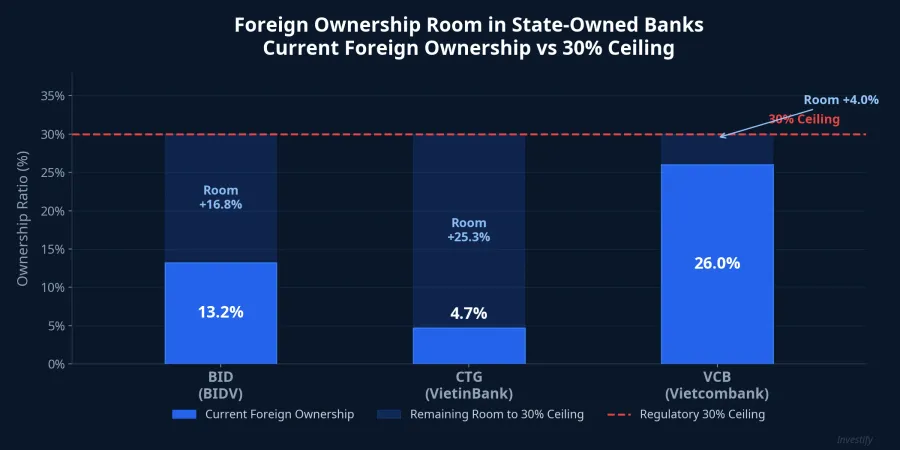

Expanding Foreign Ownership Limits: State Banks and Real Estate

The document emphasizes "expanding cooperation and deep integration with the international economy" and "unlocking capital channels." This provides the highest legal foundation for expanding foreign ownership limits — a key condition that FTSE Russell requires for completing the upgrade.

Currently, foreign ownership at BID stands at only about 13.2%, CTG at about 4.7%, while VCB is near the ceiling at 26%. Compared to the 30% ceiling for the banking sector, BID and CTG still have room of 16.8% and 25.3%, respectively. If foreign ownership limits are expanded or foreign investor mechanisms improved, an estimated $5–5.5 billion in passive ETF flows would pour into capped blue chips.VinaCapital

The $5–5.5 billion figure is not an optimistic prediction. It is based on Vietnam's expected weight in the FTSE Emerging Index, multiplied by the total assets under management of ETFs tracking the index. This capital flow is passive — meaning it will automatically flow in regardless of fundamental analysis, as long as Vietnam is in the index.

Beneficiaries: BID, CTG, VCB (state-owned banks with low foreign ownership); VIC, VHM (large real estate companies with high foreign ownership, benefiting from new capital flows).

State Bank Recapitalization: BID, CTG, VCB

The Resolution requires "strengthening financial capacity, ensuring economic-financial security, and increasing systemic resilience." With double-digit GDP growth targets, the banking system needs significantly more capital to supply credit to the economy.

BIDV took the lead by completing a private placement of 258 million shares at VND 38,900 per share on March 24, raising nearly VND 10,000 billion and increasing its charter capital to over VND 72,800 billion.VietnamBiz VCB is also preparing to issue over 1 billion bonus shares at its AGM on April 24.

However, investors should note that additional share issuance dilutes EPS in the short term. For BID, the 258 million new shares are locked for one year, reducing immediate supply pressure but creating potential overhang from March 2027. Over the next 3–5 years, if credit growth reaches 15–16% annually as planned, this additional capital will become a clear competitive advantage for the Big 3 state-owned banks.

Digital Assets: A New Signal from the Central Committee

Resolution 18 emphasizes "developing science, technology, innovation, and digital transformation" as key growth drivers. The 2025 Digital Technology Industry Law has been in effect since January 1, 2026, establishing legal status for digital assets in Vietnam for the first time.Thư viện Pháp luật The Central Committee resolution further reinforces this direction at the highest level.

Related stocks: FPT (digital infrastructure, digital transformation), CMC (AI-X strategy). While this is a long-term story, confirmation at the Central Committee level creates a stronger legal foundation than any previous government resolution. The regulatory framework for digital asset exchanges could take shape from 2027, opening new business opportunities for the technology sector.

Risks to Consider

A positive policy landscape does not mean the market will rally immediately. Foreign investors net sold nearly VND 18,000 billion in March alone, pushing total Q1 net selling to over VND 32,000 billion — a record level.Người Quan Sát

Liquidity on April 3 reached only 772 million shares, among the lowest in the month. Domestic capital is cautiously waiting for clearer signals. Moreover, there is always a significant lag between policy documents and actual implementation. Resolution 18 is a directive, not a decree with immediate effect. Investors should clearly distinguish between policy expectations and implementation results, avoiding FOMO into stocks solely because of "policy support" without concrete financial data.

April 6–10: The Action Window

The first trading session after Resolution 18 is Monday, April 6. One day later, FTSE Russell announces its review results. If both signals are positive, this could be a rare moment of policy convergence: the Party's direction and international standards pointing the same way, elevating Vietnam's capital market.

Investors should monitor three factors next week: (1) foreign investor reaction on April 6, (2) the FTSE review result on April 7, and (3) overall market liquidity trends. If all three factors align positively, securities firms (SSI, VND, HCM) and state-owned banks (BID, CTG) will be the tickers most worth positioning in early.