The big picture reveals a striking paradox: Vietnam's exports have weathered the historic tariff shock, yet capital flows in the stock market have diverged more violently than ever. One year after Trump's "Liberation Day," the question is no longer "who survived" but "who is actually emerging stronger from the crisis."

The 04/02/2025 Shock: The Darkest Trading Session in History

On April 2, 2025, US President Donald Trump announced reciprocal tariff policies, imposing a 46% duty on Vietnamese goods — the highest among affected nations. The stock market reaction was immediate: the VN-Index plunged over 82 points on April 3, 2025, its steepest single-day decline ever, with hundreds of stocks hitting the floor on HOSE.Tuổi Trẻ

Foreign capital fled, retail investors panic-sold across the board. At that point, the worst-case scenario many envisioned was Vietnam losing its export competitive edge for years. However, the following 12 months proved otherwise.

After intense rounds of negotiations, Vietnam and the US reached an agreement reducing tariffs from 46% to 20%, effective August 2025.Tuổi Trẻ The effective average tariff rate for Vietnamese goods entering the US is now approximately 18%, significantly lower than many regional competitors.Ministry of Industry and Trade The VN-Index staged a remarkable recovery, closing 2025 at an all-time high of 1,784.49 points.VietnamBiz

Q1/2026 Exports: Clear Recovery but Uneven Across Sectors

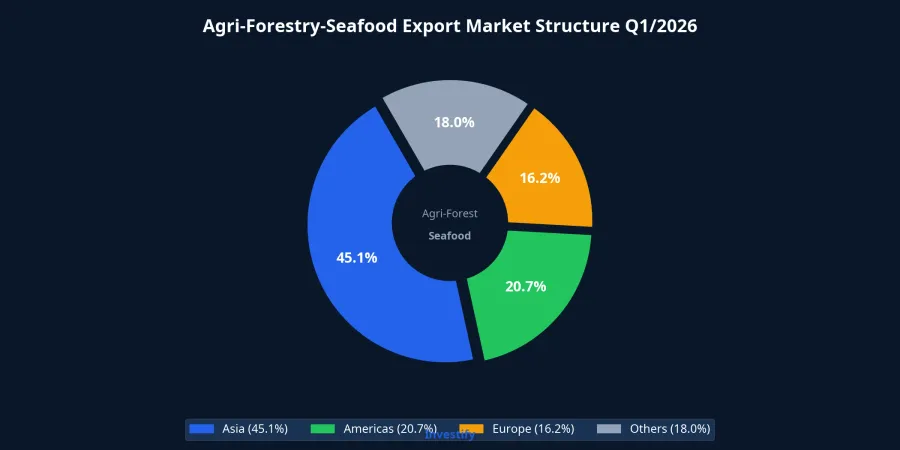

Capital flows are shifting, and Q1/2026 data provides the clearest evidence. According to the Ministry of Agriculture, agri-forestry-seafood exports reached $16.69 billion, up 5.9% year-over-year, with a trade surplus of $4.78 billion (+12%).Thương Gia Online Overall, the export sector has moved past the tariff shock. But a closer look at individual sectors reveals a less uniform picture.

Seafood led the pack at $2.62 billion (+13.3%). Pangasius, Vietnam's flagship export to the US, benefited directly from tariff advantages over Chinese tilapia, which faces higher duties. However, the signal isn't entirely optimistic: pangasius exports to the US in the first two months reached only $38 million, down 5%, as importers remain cautious about new Marine Mammal Protection Act (MMPA) regulations.VASEP

Agriculture reached $8.93 billion (+4.1%), driven by effective market diversification toward Asia. Asia now accounts for 45.1% of agri-forestry-seafood export share, with China maintaining its position as the largest partner (22.1%) while the US declined to 18.3%.

Forestry was the sole weak spot at $4.11 billion, down 2.4%. Although the US postponed Section 232 timber tariff increases from early 2026 to 2027, current rates of 10-25% depending on product type continue to weigh heavily.Tuổi Trẻ The timber industry targets $18-19 billion for full-year 2026, but prospects depend heavily on upcoming negotiations.NLĐ

Textiles target $49-49.5 billion (+8%), with a strategic pivot toward smaller, higher-value FOB orders and reduced dependence on simple contract manufacturing.Dân Việt

Export Stocks: Winners and Losers After 12 Months

The last time the market saw this level of divergence within a single sector was during 2018-2019, when the first US-China trade war created clear winners and losers among exporters. This time, the gap is even wider.

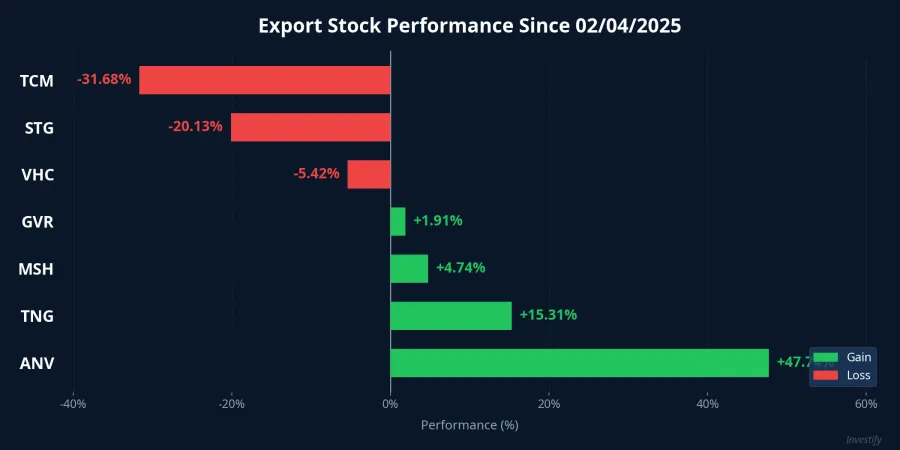

The recovery leaders share common traits: strong profit margins, stable order books, and low dependence on imported raw materials. ANV (Nam Viet) led with a +47.74% gain, benefiting from direct competitive advantages as Chinese tilapia faces higher tariffs. TNG (TNG Investment) rose +15.31% thanks to high FOB ratios and retained core orders, though a 5.83% drop on 04/03/2026 signals near-term pressure remains. MSH (May Song Hong) held steady at +4.74%, supported by long-term commitments from major customers.

The pressure group exhibited opposite characteristics: heavy reliance on imported materials and high logistics costs. TCM (Thanh Cong Textile) fell the steepest at -31.68%, currently trading at VND 22,550, sitting below all moving averages. Margin compression from rising input costs is eroding its competitive edge. VHC (Vinh Hoan) declined -5.42% despite the seafood sector's tariff advantage, suggesting US demand recovery is slower than expected. STG (Sotrans) dropped -20.13% as logistics prospects narrowed alongside declining US-bound orders.

Risks Ahead: Four Variables to Watch

While the current 20% tariff is significantly lower than the initial 46%, it would be a mistake to treat this as a stable "new normal." Four variables could shift the landscape at any moment.

First, the tariff agreement has an expiration date. Upcoming negotiation rounds will determine long-term rates, and any policy change from Washington could impact exporters immediately.

Second, input costs continue climbing. Container freight rates remain elevated due to the Red Sea situation, combined with rising imported material prices, squeezing already-thin margins for many businesses.

Third, market diversification takes time. Companies are actively expanding into China, EU, and ASEAN markets, but building new distribution channels cannot be accomplished overnight.

Fourth, the FTSE Russell review session on April 7 could trigger volatility for export stocks, especially if foreign capital flows shift.

Implications for Investors

After 12 months, the picture is clear enough to draw a lesson: in an uncertain tariff environment, picking the right company matters more than picking the right sector. ANV, TNG, and MSH demonstrate that strong margins and low dependence on imported inputs are the most effective "armor" against policy volatility.

With the VN-Index currently at 1,684 points — roughly 100 points below its 2025 peak — investors should prioritize selecting stocks with solid fundamentals rather than expecting the entire export group to recover uniformly. Capital is shifting from "buy the basket" to "selective bets," and this trend is likely to continue through the coming quarters.