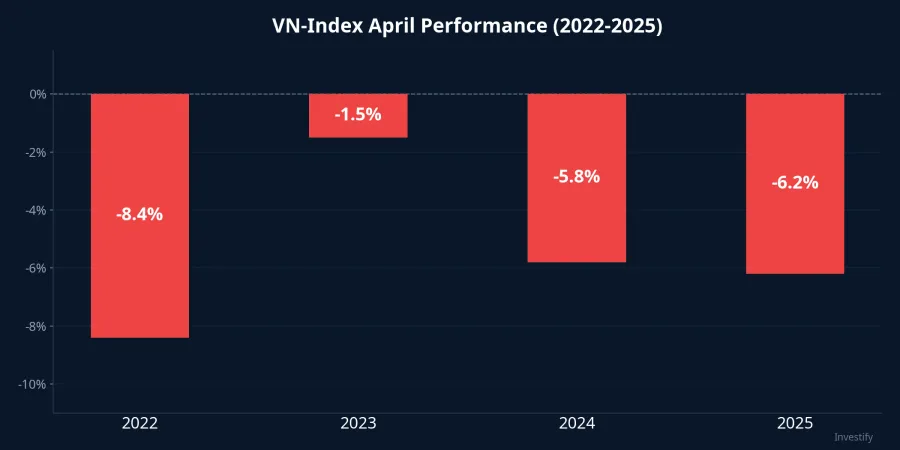

The big picture shows that April has been the cruelest month for Vietnamese stock investors over the past four years. From 2022 to 2025, the VN-Index posted four consecutive April declines, averaging roughly 5.5% losses. But in 2026, capital flows are shifting in an entirely new direction.

Four Consecutive "Red" Aprils

Looking at the data, this seasonal pattern is no coincidence. Each April decline had clear macroeconomic causes, and the losses were consistently significant:

- April 2022: -8.4% (from 1,492 to 1,367 points). The Fed's aggressive rate hikes and the Tan Hoang Minh scandal shook the bond market.

- April 2023: -1.5% (from 1,065 to 1,049 points). The market remained in a weak recovery phase following the 2022 bottom.

- April 2024: -5.8% (from 1,284 to 1,210 points). Exchange rate pressure and heavy foreign net selling.

- April 2025: -6.2% (from 1,307 to 1,226 points). U.S. tariff concerns and foreign capital withdrawals from emerging markets.

The average decline across the last four Aprils was approximately 5.5%.HOSE This is a concerning seasonal pattern that every investor should consider when entering April 2026. However, three factors that never appeared in the previous four years are creating a fundamental difference.

FTSE Russell Review on April 7: A Historic Turning Point

On April 7, 2026, FTSE Russell will announce the results of its interim review, the final checkpoint before Vietnam officially gets upgraded to Secondary Emerging Market status on September 21, 2026.LSEG This is an event the market has been waiting for over a decade.

FTSE Russell has identified 28 Vietnamese stocks eligible for the FTSE Global All Cap index, including major names such as HPG, VCB, VIC, VHM, MSN, SAB, VNM, VJC, and SSI.VnEconomy Vietnam is expected to account for approximately 0.22% of the FTSE Emerging Index.

In terms of capital flows, FTSE Russell estimates approximately $6 billion from passive ETF funds will flow into Vietnam's market, while the World Bank forecasts short-term inflows of around $5 billion and long-term flows potentially reaching $25 billion by 2030.Vietnam Briefing The last time a catalyst of this magnitude appeared in April was never in the past four years. Capital from passive funds is not "buy-and-sell" money but mandatory index-tracking flows, creating a long-term demand foundation for the 28 selected stocks.

Brent Oil Reversal: Good News for Vietnam's Economy

After surging a record 64% in March 2026 due to Middle East conflicts, Brent crude reversed course and dropped to around $102 per barrel on April 1, losing nearly 10% from its $112 peak in just a few trading sessions.Doanh nghiep Hoi nhap The main catalyst was positive negotiation signals between the U.S. and Iran, with Iran's president declaring readiness to cease military action if security guarantees are achieved.

Falling oil is good news for Vietnam's economy for three reasons: it reduces inflationary pressure, lowers transportation and production costs, and opens room for the State Bank of Vietnam to maintain an accommodative monetary policy. Direct beneficiaries include airlines (VJC, HVN), shipping companies, and consumer goods manufacturers. With interbank overnight rates running high, falling oil prices give the central bank additional policy flexibility without worrying about inflation exceeding targets.

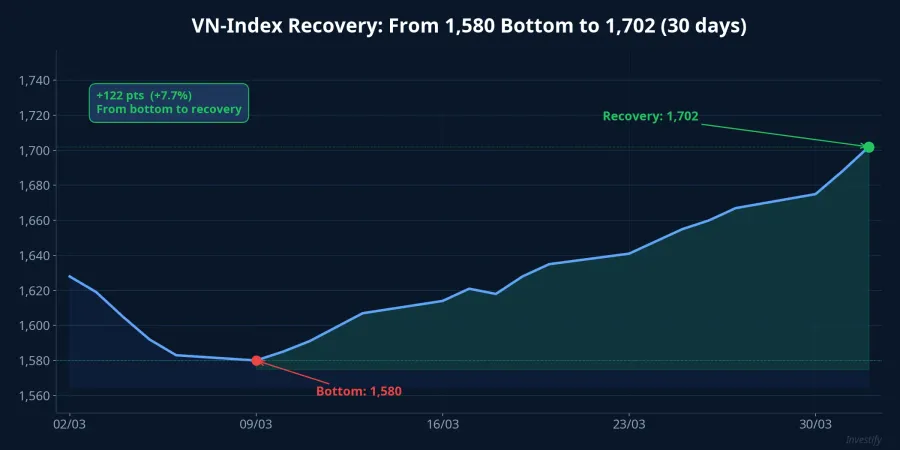

Clear Recovery Momentum from the 1,580 Bottom

The VN-Index staged a strong recovery from the approximately 1,580-point bottom in early March, reaching 1,702.93 points in the April 1, 2026 session, gaining over 7.5% in less than a month. On the first trading day of April, the index surged 1.70% driven by Vingroup stocks and airline shares, with trading volume exceeding 943 million shares.

Major securities firms are all issuing positive forecasts: BVSC targets 1,800 points in April, Yuanta Vietnam aims for 1,736-1,750 points, and BSC considers the 1,700-1,725 range as a new equilibrium base.VnEconomy Notably, this recovery is accompanied by gradually increasing liquidity, indicating that real money is returning to the market rather than a mere technical bounce.

Risks Still Lurking

Despite many positive factors, investors should remain vigilant about four key risks:

System liquidity under stress: The overnight interbank rate stands at 12%, signaling significant pressure on banking system liquidity. This could directly impact margin funding and retail investor purchasing power.

Oil decline remains unstable: U.S.-Iran negotiations could collapse at any moment, pushing oil prices back to the $110-115 per barrel range. Such a scenario would completely reverse the positive effects of falling oil prices.

FTSE Russell could delay: If the April 7 review shows Vietnam has not met sufficient conditions regarding Global Broker access mechanisms, the September upgrade timeline could be postponed. This is a binary event: a positive result triggers a strong rally wave, while a negative one creates significant selling pressure.

Seasonal effects have statistical backing: Four consecutive years is not random. April typically coincides with Q1 financial reporting season and profit-taking pressure following Q1 rallies, creating a negative psychological loop that is hard to break.

Strategy for Investors

Rather than making a one-directional bet, investors can consider four approaches:

Prioritize the 28 FTSE stocks: HPG, VCB, VHM, VIC, and MSN are the direct beneficiaries of passive ETF flows if the upgrade succeeds. This group has the clearest structural demand thesis in the short term.

Monitor the April 7 results closely: This event is binary. Investors should have plans for both scenarios: add exposure to FTSE stocks on a positive outcome, shift to defensive positioning on a negative one.

Maintain 20-30% cash allocation: Defend part of the portfolio to prepare for a seasonal repeat scenario. Cash is not a weak position; it is a call option to buy at better prices.

Capitalize on falling oil: Airlines (VJC, HVN), transportation, and consumer stocks have fundamental reasons to outperform in the short term as input costs decline.

April 2026 presents a rare confrontation between a negative seasonal pattern and positive macroeconomic drivers. For the first time in five years, the market has legitimate reasons to expect a break in the losing streak; but risk management discipline remains the deciding factor between success and failure.