Looking at the VND 30 trillion charter capital target that SSI has set, many would ask: why does the industry leader need even more capital? The answer lies in a bigger picture: in just 5 days, on April 7, 2026, FTSE Russell will announce its interim assessment results — the final checkpoint before officially adding Vietnam to the FTSE Emerging Index from September 2026. And SSI is far from the only firm racing to prepare.

SSI: VND 30 Trillion Target, Cementing the Top Position

According to SSI's 2026 annual general meeting documents, the company plans to issue approximately 500 million bonus shares to existing shareholders at a 5:1 ratio — for every 5 shares held, shareholders receive 1 new share at a par value of VND 10,000. If completed, SSI's charter capital will rise from roughly VND 25 trillion to VND 30 trillion, reinforcing its position as the industry's undisputed leader.Thời báo TCVN

The 2026 business plan is equally ambitious: SSI targets revenue of VND 15.66 trillion (up 19%) and pre-tax profit of VND 5.838 trillion (up 15%) compared to 2025. Shareholders will also vote on a 10% cash dividend, equivalent to VND 1,000 per share, totaling over VND 2.5 trillion in payouts. The AGM is scheduled for April 23 at Thong Nhat Hall, Ho Chi Minh City.

The estimated dilution ratio is approximately 16.7% — not insignificant. However, since shares are issued from existing equity (bonus shares), current shareholders don't need to contribute additional capital and maintain their ownership ratio. The new capital will fund core operations: brokerage, margin lending, proprietary trading, and technology infrastructure investment.

The Industry's VND 77.8 Trillion Capital Race

SSI isn't alone in this game. Total planned capital increases across the securities industry amount to VND 77.8 trillion, of which less than 50% has been completed so far.VnEconomy

The industry landscape reveals an ever-widening gap between SSI and the rest. VND (VNDIRECT) currently has charter capital of approximately VND 15.223 trillion — less than half of SSI's target. HCM (HOSE Securities) follows with VND 10.808 trillion. Notably, both MBS and SHS are planning to push their charter capital past VND 10 trillion, with SHS targeting profits of VND 1.7 trillion.Vietstock

VCI (VietCap), while smaller in scale, has set an ambitious pre-tax profit target of VND 2.3 trillion, a 41% year-over-year increase — signaling that mid-tier firms are also making big bets on the upcoming period.VietnamBiz

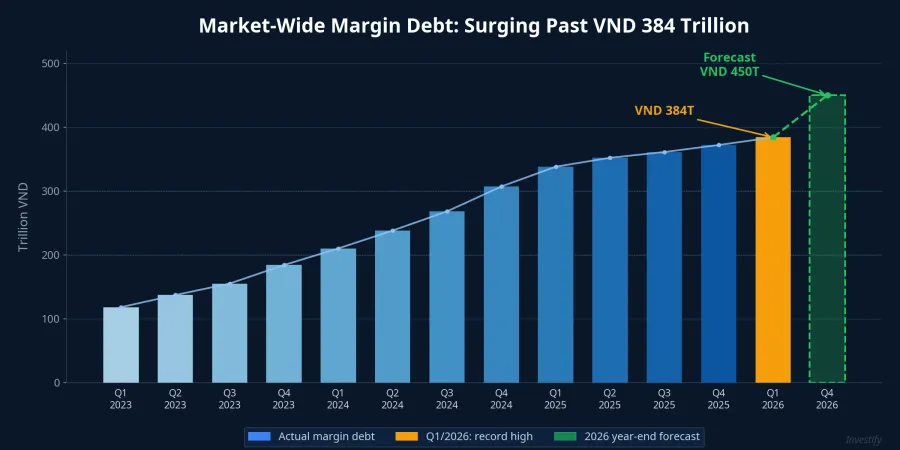

The Margin Equation Before the FTSE Gate

Why are securities firms simultaneously raising capital right now? The answer lies in the industry's core operating mechanism. By regulation, margin lending debt cannot exceed twice a firm's equity. Larger equity means higher margin limits, which enables serving more investors and capturing greater market share.

The numbers make the urgency clear. As of Q1/2026, market-wide margin debt surpassed VND 384 trillion, up 62.5% year-over-year.VnEconomy Forecasts for 2026 suggest this figure could exceed VND 450 trillion as foreign capital begins flowing in post-upgrade.

When FTSE Russell officially upgrades Vietnam from September 2026, capital inflows from ETFs tracking the FTSE index are estimated at USD 600–1,500 million.Duane Morris Higher liquidity drives margin demand and brokerage revenue upward. Firms with larger capital bases will hold a clear competitive advantage. In essence, raising capital today means laying the foundation to harvest revenue from foreign capital inflows tomorrow.

Lessons from Previously Upgraded Markets

International experience shows that financial stocks typically rally strongly in the 1–2 years before an upgrade, as expectations of new capital flows begin to be priced in. After the official upgrade, price appreciation tends to slow as the market has already "bought the rumor." However, the crucial point is that brokerage and margin revenues sustain their growth trajectory thanks to structurally improved liquidity, not just temporary spikes.

This is precisely why Vietnamese securities firms aren't just racing to raise capital but are also investing heavily in technology infrastructure, preparing for T+0 settlement when the KRX system is fully operational. Stronger infrastructure means handling larger transaction volumes when foreign capital truly begins to flow.

Long-Term Opportunity vs. Short-Term Dilution Risk

In the morning session of April 2, VN-Index traded around 1,696.85 points, down 0.36%. Securities stocks showed mild movements: SSI fell 0.54% to VND 27,750, VCI dropped 0.73% to VND 27,150, VND declined 0.62% to VND 16,150, while HCM bucked the trend with a 0.64% gain to VND 23,650.

For investors, it's essential to distinguish two dimensions when evaluating this capital-raising wave. On the long-term opportunity side, increased capital expands margin capacity, maximizes the capture of post-FTSE foreign capital flows, and supports new business lines such as securities lending and T+0 trading. On the short-term risk side, historical data shows SSI dropped approximately 15% within 30 days of its supplementary issuance announcement in early 2026. A sharp increase in share supply invariably creates downward price pressure.

By the numbers, buying securities stocks now is a bet that the FTSE upgrade will generate enough new revenue to offset the dilution effect. If foreign capital flows meet expectations, leading firms like SSI, HCM, and VCI will be direct beneficiaries. But if FTSE delays the upgrade or capital inflows fall short of forecasts, dilution risk becomes a real burden for shareholders.