What the March 2026 PMI report doesn't say outright, the numbers are screaming: Vietnam's manufacturing sector is entering a danger zone. Not because of recession, but because costs are eroding profit margins faster than at any time in nearly 15 years.

March PMI: The 51.2 Figure Masks the Real Risk

Vietnam's manufacturing PMI for March 2026, published by S&P Global, came in at 51.2, dropping sharply from February's 54.3. Many investors look at this number and sigh with relief: still above 50, meaning still expanding. But the real risk lies in three sub-indices underneath.

First, output prices rose at the fastest pace since April 2011 — nearly 15 years. Companies were forced to pass cost burdens onto customers, but not everyone can. Second, input costs surged at the steepest rate since April 2022, with nearly half of surveyed companies reporting sharp raw material price increases. Third, delivery times were stretched to their worst levels in 4 years, reflecting severe supply chain disruptions.S&P Global

Export orders reversed from strong growth in late 2025 to a steep decline, employment contracted, and business confidence fell to a 6-month low. This picture isn't a recession, but it's clearly a stress test for Q1/2026 profit margins.

Middle East Conflict: The Trigger for the Cost Shock

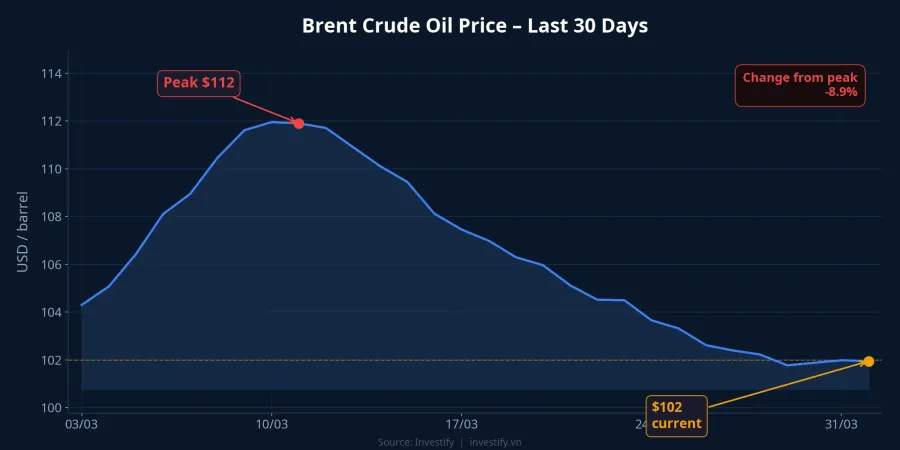

The root cause lies in the US-Iran conflict in the Middle East. Brent crude surged over 60% in less than a month, dragging the entire petroleum-based raw materials cost chain sharply higher. This was the primary driver behind the abnormal spike in input costs and selling prices during March.CafeF

The positive signal is that Brent has retreated from its peak of $112.57/barrel (March 27) to approximately $101.96/barrel (April 2) on hopes of negotiations. President Trump declared that attacks on Iran could cease within 2-3 weeks.Euronews However, Tehran rejected the US proposal. In other words, oil may have passed its short-term peak, but geopolitical risk still hangs in the balance.

Four Manufacturing Sectors: Who Takes the Hardest Hit?

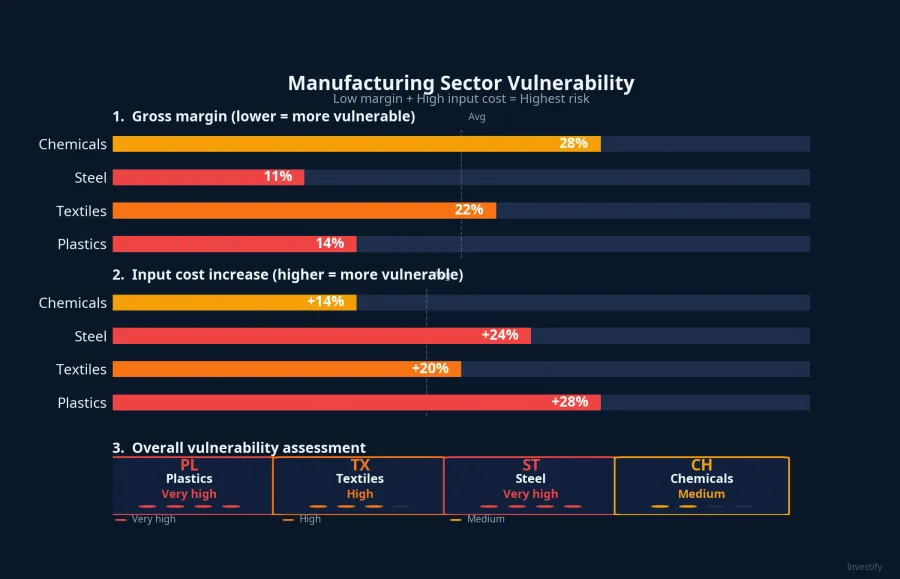

Not every sector is equally affected. Vulnerability depends on two factors: gross profit margin (capacity to absorb costs) and the specific magnitude of input cost increases.

Plastics (AAA, TPC): Most Vulnerable

The plastics sector tops the risk list. Vietnam imports approximately 70% of its virgin plastic resin needs, and polypropylene (PP) prices rose about 19% while polyethylene (PE) surged nearly 25% in March.Kanetora With gross margins of only 7-14%, companies like AAA and TPC have virtually no room to absorb the cost shock. When input costs rise 25% against a 14% gross margin, the profit equation becomes brutally harsh.

Textiles (TCM, HTG): Double Blow from Costs and Orders

Textiles face a twin hit: international shipping costs surging due to supply chain disruptions, while export orders weaken (consistent with PMI data). Gross margins of 11-16% sound better than plastics, but pricing power is severely limited because most processing contracts were signed at fixed prices beforehand. Companies are trapped between rising costs and locked-in selling prices.

Steel (VCA, TNS): Thin Margins, but Domestic Demand Helps

HRC steel prices rose approximately 4% in the month and 13% over three months — not as dramatic as polymer increases. Stable domestic construction demand provides some relief. However, the steel sector's gross margins are extremely thin at just 1-3%. With margins this razor-thin, even small cost fluctuations can push companies from profit to loss.

Chemicals (CSV): Least Vulnerable

Basic chemicals is the safest sector in the group, with the highest gross margin (~25%) and strong pricing power thanks to essential products with limited direct competition. Input costs are affected by oil prices but the increase is not dramatic. This could be the group that attracts defensive capital flows as the market diverges.

VN-Index Breaks 1,700, but Divergence Is Forming

On April 1, VN-Index surged 28.44 points (+1.70%) to 1,702.93 with 217 gainers and over 943 million shares traded. The rally was supported by positive global markets: the S&P 500 rose sharply, Hang Seng gained +2.04%, and oil declined on Iran negotiation hopes.Yahoo Finance

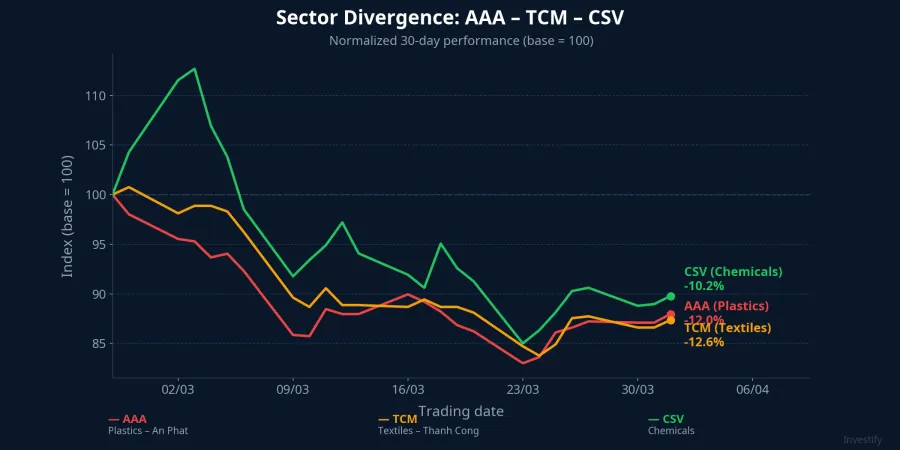

But here's what the report doesn't tell you: VN-Index broke through 1,700 primarily thanks to Vinhomes, financials, and airlines. Meanwhile, the manufacturing group — textiles, plastics, steel — is absorbing the cost blow. The 30-day stock performance chart shows that AAA, TCM, and CSV all declined 10-13%, regardless of their vulnerability levels.

With Q1/2026 earnings season about to enter its peak period, manufacturing sector profit margins could disappoint. That is the real risk for investors currently holding positions in this group.

Strategy Ahead of the April 2 Session

Positive signals remain: oil has dropped to the $101-102 range, international markets are green, and VN-Index has crossed above its 20-day moving average. However, the hidden risk is that PMI deceleration combined with persistently elevated input costs means Q1 manufacturing margins could come in weaker than expected.

Investors should exercise caution with the plastics and textiles groups in the short term. Monitor the chemicals sector, especially CSV, as this group has the capacity to attract defensive capital when the market diverges. Maintain a neutral weighting on steel as long as PMI holds above 50. The decisive factors in the coming week: the progress of US-Iran negotiations, oil prices, and the first Q1 earnings reports from listed manufacturers.