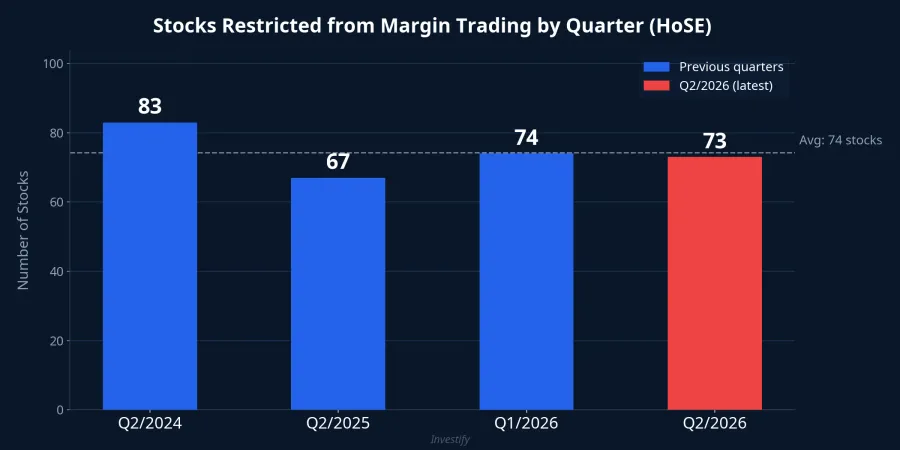

What the reports don't spell out when VN-Index crosses the 1,700-point mark is that the foundation underneath is shaking. On the very first trading session of Q2/2026, the Ho Chi Minh Stock Exchange (HoSE) published a list of 73 stocks ineligible for margin trading.Vietnambiz This number is slightly down from 74 stocks at the start of Q1/2026, but still significantly higher than 67 stocks in the same period last year.Người Quan Sát

The real risk lies here: the market was riding high on expectations of FTSE Russell's announcement on April 7, yet on the April 2 session, VN-Index reversed course and dropped 0.48% to 1,694.82 points with 267 declining stocks versus only 70 advancing. The margin restriction list is the regulator's reminder: don't let the index rally obscure the true quality of listed companies.

73 Stocks Split into 4 Groups

According to HoSE's official announcement, the 73 margin-restricted stocks are clearly classified into 4 groups.Người Quan Sát

Group 1: Under warning, supervision, or trading restriction accounts for the majority, including familiar names like BCG, DLG, LDG, TTF, SMC, TCD, and TLH. Notably, BCG (Bamboo Capital) is currently suspended from trading with zero liquidity across multiple consecutive sessions after repeatedly failing to submit audited financial statements.VnEconomy

Group 2: Negative after-tax profit includes 14 stocks, with NVL (Novaland) being the most notable. Group 3: Newly listed within 6 months includes AFX, MCH, VCK, VPX, and others — this group is restricted by technical regulation, not business quality. Group 4: Late financial reports or adverse audit opinions includes HID, VMD, TIX, VTO, GDT, and STG.

NVL: Out of Losses, But Not Out of Danger

Novaland best illustrates the paradox of "surface-level optimism, underlying risk." The group recorded an after-tax profit of VND 1,818 billion in 2025, officially returning to profitability after two consecutive years of losses.Phụ Nữ Việt Nam However, the balance sheet tells a completely different story: cash on hand is only VND 4,395 billion while short-term debt reaches VND 95,997 billion. In other words, for every dong of cash, NVL carries nearly 22 dong of debt due within 12 months.

Analysis from VNSC shows that from now until end of 2026, Novaland does not have sufficient funds to cover maturing debts.VNSC NVL closed the April 2 session at VND 13,850/share, down 2.12% — despite touching a short-term peak of VND 14,900 just one week prior.

HVN: Escaped Negative Equity, But Debt Still 10x Equity

Vietnam Airlines is another special case. The national carrier officially escaped negative equity in September 2025 after SCIC injected VND 7,770 billion in share purchases.Báo Đầu Tư However, HVN's total debt remains 10.6 times its equity, with short-term liabilities exceeding current assets by approximately VND 34,200 billion. HVN closed the April 2 session at VND 22,150/share, down 1.12%.

But who bears the cost? It's the retail investors using leverage on these stocks, believing that "returning to profit" equals "safe to invest." Returning to profitability on the income statement and having enough cash to service debt are two entirely different stories.

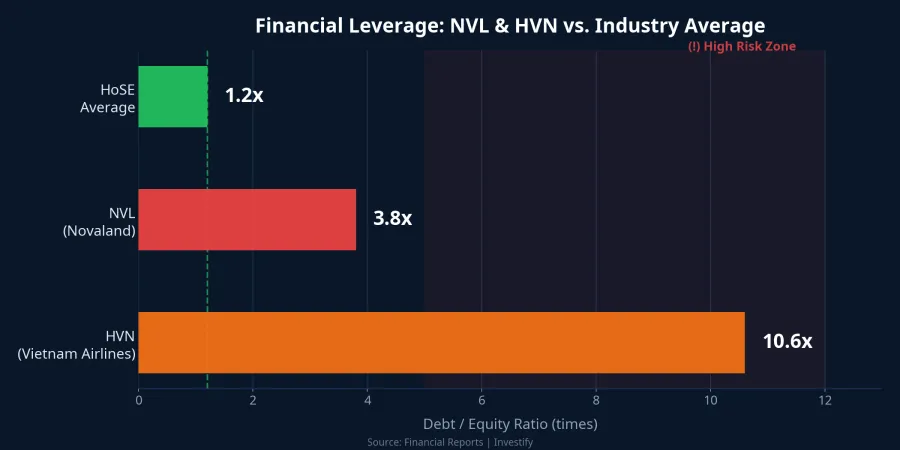

Financial Leverage: The Gap Between NVL, HVN, and the Rest

The chart below illustrates the financial leverage of NVL and HVN compared to the HoSE industry average. When the debt-to-equity ratio exceeds 5 times, a company enters a high-risk zone — any shock to cash flow or interest rates can trigger a negative chain reaction.

Record Margin Debt, Rising Rates: A Recipe for Forced Selling

The current environment makes margin risk more serious than ever. Total market margin debt hit a record of approximately VND 360,000–406,000 billion by end of 2025.Vietnambiz Since early March 2026, numerous securities firms have raised margin interest rates by 0.5–1 percentage points, bringing the general level to 13–14% per year.VnEconomy

When a stock is placed on the margin restriction list, investors cannot use borrowed funds to buy more. For those holding margin positions on these stocks, brokerages may require additional collateral or gradual position reduction. If investors fail to comply, forced selling is triggered, creating domino selling pressure that pushes prices down further. With margin rates at 13–14% per year, the cost of holding positions is also increasingly expensive.

The Paradox: Index Rising, Corporate Fundamentals Still Weak

The persistently high number of margin-restricted stocks over the past three quarters (67 → 74 → 73) reflects a concerning reality. VN-Index has recovered to the 1,700-point range, but the financial health of many listed companies has not improved proportionally. Accumulated losses, bad debts, and late financial reporting — these are structural problems that cannot be resolved by index momentum alone.

With the FTSE Russell expectation on April 7 and the Q1/2026 earnings season approaching, investors need to clearly distinguish between "cheap stocks" and "high-risk stocks." The margin restriction list is the last shield that regulators put in place — treat it as a warning signal, not a bottom-fishing opportunity.

What Should Investors Do?

- Holding margin positions on restricted stocks: consider proactively reducing positions before forced selling kicks in. Waiting and hoping is the worst strategy when brokerages have already tightened collateral requirements.

- Interested in NVL, HVN: closely monitor debt restructuring progress and Q1/2026 results. Only consider when there are signals of genuine cash flow improvement, not just accounting profits.

- Newly listed stocks (MCH, VCK, NTC): wait at least 6 months of trading and 1–2 financial reporting periods before using leverage.

- General principle: only use margin on stocks with stable earnings, high liquidity, and no regulatory warnings. Margin is an amplifier — it amplifies both gains and losses.