Looking at the numbers from Gelex's Annual General Meeting on April 1, 2026, the financial picture is quite clear: revenue continues to break records while profit sharply reverses. This is a familiar paradox for multi-sector conglomerates during expansion phases, but for Gelex, the story also comes with a notable leadership transition.

Leadership Transition: CEO Becomes Chairman, New CEO Born in 1994

At the AGM held at Fairmont Hotel Hanoi, Mr. Nguyen Van Tuan — who served as CEO since 2017 — was officially elected Chairman of the Board for the 2026-2031 term.MekongAsean Taking over as CEO is Mr. Le Tuan Anh, born in 1994, making him one of the youngest CEOs on Vietnam's stock exchange.MekongAsean

This model is common in corporate governance: the founder or veteran CEO moves to a strategic role, handing operational authority to the next generation. More noteworthy was Mr. Tuan's statement at the meeting, confirming he would not join Eximbank's Board — putting to rest years of speculation.VnExpress However, Gelex left open the possibility of increasing its Eximbank stake from 10% to 15% when conditions allow.CafeF

In other words, Gelex wants to maintain its financial interests in the bank without getting entangled in Eximbank's power struggles. This is a pragmatic choice that allows management to focus resources on core business operations.

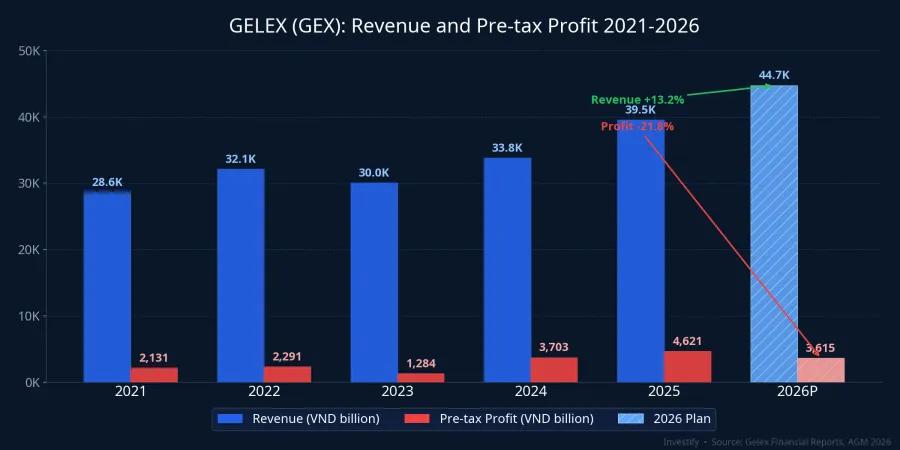

The Financial Paradox: Record Revenue, Declining Profit

The figures approved at the AGM paint a striking contrast. Consolidated revenue target is VND 44,712 billion, up 13.2% from the record VND 39,513 billion in 2025. Meanwhile, planned pre-tax profit is only VND 3,615 billion, down 21.8% from VND 4,621 billion achieved last year.MekongAsean

Looking at the 5-year chart, the continuous upward revenue trend is a positive signal showing the company's expanding scale. But net profit margin hovering around 7.5% — the "thin margin" characteristic of multi-sector conglomerates — tells a different story. According to management, the main drivers are pressure from borrowing costs and operating expenses from new projects that have not yet reached full capacity.

Simply put, Gelex is accepting "short-term pain" to build the foundation for the next growth cycle. The question is how long this pain period will last, given that the current interest rate environment is hardly favorable for leveraged investment strategies.

Four Strategic Pillars for 2026-2031

Gelex has structured its new-phase strategy around four core business segments.Vietnam Financial Times

Electrical equipment remains the backbone. The brand ecosystem of CADIVI, THIBIDI, HEM, and VIHEM has established a strong foothold in Vietnam's power sector. This segment directly benefits from the national power grid investment cycle and surging demand for transformers, providing stable and predictable revenue.

Water infrastructure is the noteworthy new highlight. Gelex is coordinating the development of 3 wastewater treatment projects in Ho Chi Minh City while expanding clean water supply capacity. This segment offers stable cash flow characteristics, suitable for balancing risk across the portfolio.

Real estate in industrial parks and residential segments is being reinforced through GELEX Infrastructure. This segment offers high profit margins but depends heavily on handover schedules and market conditions. With industrial real estate currently benefiting from FDI inflows, this could be a significant growth driver if project timelines are met.

Finance is represented by the strategic investment in Eximbank — approximately 10% ownership, equivalent to 187 million EIB shares — with a long-term holding approach. The decision not to join the board while maintaining a large ownership stake suggests Gelex views this as a pure financial investment, not a control instrument.

Generous Dividends, But Significant Dilution

The shareholder distribution plan looks impressive on the surface: total dividend and bonus share ratio reaches 53%, comprising 25% stock dividends, 8% cash, and 20% issuance from equity.Vietstock

However, issuing an additional 45% in shares means significant dilution. If 2026 profit hits the planned VND 3,615 billion, diluted EPS will drop sharply compared to 2025. Investors need to clearly distinguish between "receiving more shares" and "creating more real value" — two very different concepts. Stock dividends essentially just slice the pie thinner, not make it bigger.

GEX Valuation: The Conglomerate Discount

On April 2, 2026, GEX traded around VND 36,300, down 2% from the previous session and approximately 11.3% lower year-to-date. Market capitalization stands at roughly VND 32,800 billion. The only positive signal is a 3.7% recovery over the past month.

On valuation, the 2025 P/E ratio at 13.3x is significantly lower than the electrical equipment industry average (approximately 22-23x). This gap reflects the conglomerate discount and concerns about capital efficiency. P/B at 1.3x is acceptable for an asset-heavy business, but it also shows the market is not fully buying into the growth narrative.

Three Risks to Monitor

First, copper and steel price volatility directly impacts profit margins in the electrical equipment segment. This factor is beyond management's control, and in the current cycle of highly volatile raw material prices, this risk is far from trivial.

Second, the progress of real estate and water infrastructure projects depends on regulatory approvals and market conditions. Any delays mean additional capital costs while revenue recognition is postponed.

Third, the interbank lending rate at 12% creates significant pressure on borrowing costs. For a company in a major investment cycle like Gelex, this factor can "erode" profits faster than expected if rates remain elevated for an extended period.

Conclusion: Building Foundations or Spreading Too Thin?

Gelex stands at a critical crossroads. The combination of Chairman Nguyen Van Tuan's strategic experience and 32-year-old CEO Le Tuan Anh's fresh energy is a positive governance signal. The record VND 45,000 billion revenue target is achievable with all segments expanding.

But the 21.8% profit decline is the price of that ambition. At a P/E of 13.3x, the market is pricing GEX at a discount to the sector, meaning investors could be getting a "bargain" if they believe in the long-term story. Conversely, if new projects are slow to generate returns over the next 2-3 years, the 45% dilution will continue to compress EPS. Financial discipline during this phase will determine whether Gelex becomes an efficient multi-sector conglomerate or falls into the "jack of all trades, master of none" trap.