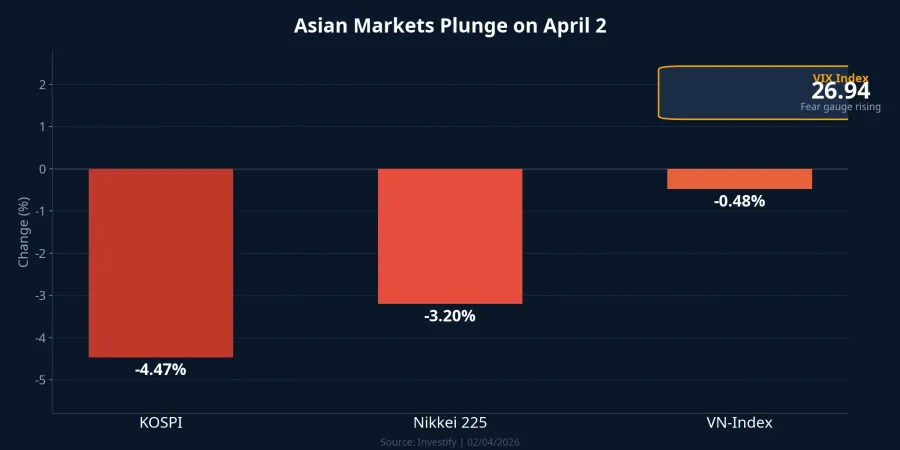

The big picture reveals a striking paradox from the April 2, 2026 trading session: Asian equities were drowning in red, yet the VN-Index retreated just 8.11 points to 1,694.82 — a modest 0.48% decline. At the same time, South Korea's KOSPI lost over 4%, Japan's Nikkei 225 dropped more than 3%, and the VIX volatility index surged nearly 10% to 26.94 — deep into the risk warning zone.Simplize

Capital flows are being pulled in opposing directions. The question isn't whether the VN-Index will fall, but rather: what's keeping it from plunging alongside the rest of the region?

FTSE Russell Expectations Anchoring Market Sentiment

The first and perhaps strongest support comes from upgrade expectations. On April 7, FTSE Russell will announce its interim review results — the final checkpoint before officially upgrading Vietnam from Frontier to Secondary Emerging Market status in September 2026.Bloomberg

According to estimates from local brokerages, the upgrade could attract hundreds of millions of dollars in passive capital flows through ETFs — a figure large enough to reshape supply-demand dynamics. This expectation is functioning as a powerful "psychological anchor," preventing domestic investors from panic-selling in sympathy with the region. In fact, the April 2 session saw foreign investors net-buy over VND 1,700 billion across the market, primarily through large block trades — a signal that institutional capital continues to bet on the upgrade narrative.

However, according to analysis from Duane Morris, the question is no longer "whether Vietnam meets the criteria" but "whether the trading system can operate at international institutional scale" — an operational risk the market has largely overlooked.Duane Morris

VHM Explodes Higher, Pulling the Index From Danger

The second support came from an unexpected name: Vinhomes (VHM). While 267 stocks declined against just 70 gainers, VHM surged nearly 7% to VND 117,900 per share — its second consecutive ceiling-hitting session.VietnamBiz

The catalyst was Vinhomes' proposal to distribute a 60% cash dividend — VND 6,000 per share — totaling up to VND 25,000 billion. This represents the largest cash dividend in VHM's trading history, immediately attracting massive capital inflows. Trading volume hit over 16.3 million shares in the session — nearly 5 times the previous day's level.

With a market capitalization exceeding VND 484,000 billion and significant weight in the VN-Index basket, VHM alone contributed meaningfully to keeping the index from falling further. Viewed from another angle, this also reveals that the index's resilience depends on a handful of large pillars rather than broad market strength.

Domestic Investor Structure: A Natural Buffer

The third support is rarely discussed but equally important. Unlike South Korea or Japan — where foreign capital makes up a large proportion and reacts quickly to global volatility — Vietnam's market is dominated by domestic retail investors. The last time a similar pattern occurred was during the August 2024 volatility episode, when the Nikkei dropped 12% in a week but the VN-Index retreated only about 2%.

Domestic capital is less sensitive to international headlines and tends to react more slowly, creating a natural buffer for the index. However, this is a double-edged sword: if domestic sentiment shifts — for example, after a disappointing FTSE result — selling pressure could persist longer because retail investors are typically slower to cut losses than institutions.

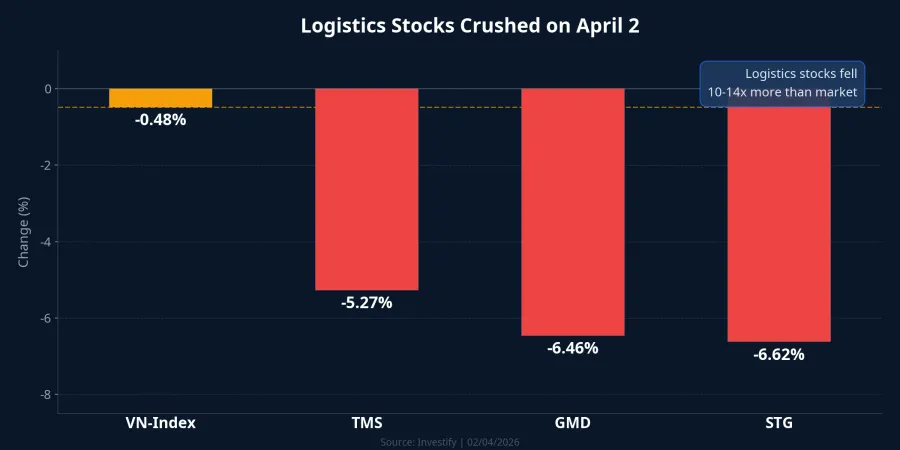

Logistics Stocks Flash Trade Risk Warnings

While three forces kept the index stable, transportation and logistics stocks sent a clear warning signal. The April 2 session recorded:

- GMD (Gemadept) fell 6.46% to VND 72,400, with trading volume 10 times the previous session

- STG (Sotrans) dropped 6.62%

- TMS (Transimex) declined 5.27%

Logistics stocks are considered a "barometer" for international trade activity. When logistics plunges while the broader index barely dips, it signals that the market is repricing supply chain disruption risk. The current context is particularly complex: Middle East geopolitical tensions are pushing oil prices higher, while concerns about returning trade barriers have intensified following new statements from the US.VietnamPlus

If trade risks escalate, export-oriented and logistics sectors will bear the first impact, with knock-on effects spreading to industrial park operators and port companies.

Strategy Ahead of FTSE Week on April 7

The FTSE Russell event on April 7 is the market's focal point. If the outcome is positive — confirming the upgrade timeline remains on track — passive ETF capital could begin portfolio rebalancing early, supporting large-cap stocks. However, investors should remain alert to a "buy the rumor, sell the news" scenario, as expectations may already be priced in.

In the near term, the big picture points to three allocation approaches:

- FTSE beneficiaries: securities firms (SSI, VCI), major banks (VCB, MBB) — continue to benefit from new capital flow expectations

- Defensive plays: industrial park real estate, consumer staples — less exposed to global trade volatility

- Caution zone: logistics, direct exporters — highly sensitive to global supply chain disruptions

Market breadth remains weak (only 70 advancers versus 337 total stocks), showing that current resilience comes from a few large pillars rather than broad-based strength. If the "FTSE wall" fails to deliver as expected, external pressures could quickly breach this fragile line of defense. Capital flows are shifting, and next week will be the most important test for Vietnam's market since the start of 2026.