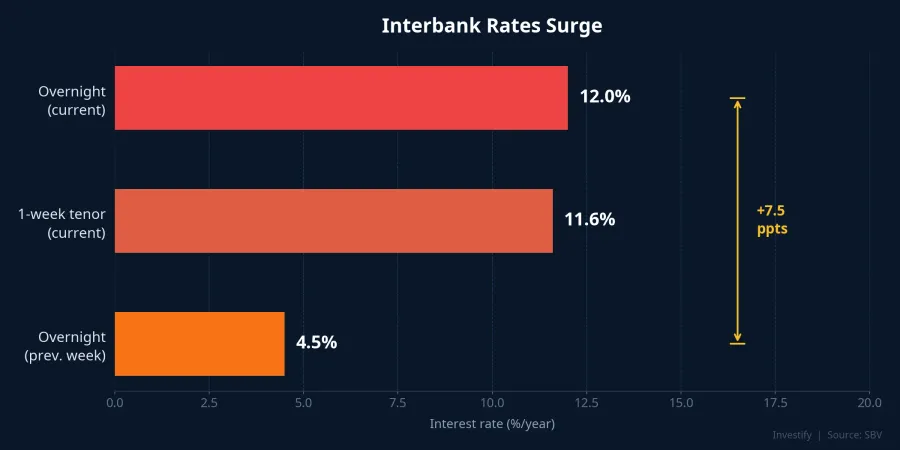

On April 1, 2026, the VN-Index surged to 1,702.93 points (+1.70%), crossing the psychological 1,700 level for the first time in months. Forums lit up green with 217 advancing stocks and turnover exceeding 943 million shares. But here's what the reports don't tell you: at the very same time, the overnight interbank lending rate spiked to 12% per annum, nearly triple its ~4.5% level just one week earlier.

The real risk lies here: when banks are willing to pay 12% just to borrow overnight, the system is desperately short of cash. And a stock market rallying on top of strained liquidity is like a beautiful house built on sand.

Interbank rates: the thermometer most investors ignore

The interbank market is where commercial banks lend to each other short-term to meet daily liquidity needs. It's the most sensitive barometer of cash flow health in the financial system, yet most retail investors completely overlook it.

When the overnight rate spikes from 4.5% to 12%, it means banks are so cash-strapped they'll pay a steep premium just to balance their books overnight. The 1-week tenor also climbed to 11.6%, confirming this is no one-off event.

The primary cause: the State Bank of Vietnam (SBV) aggressively drained liquidity through open market operations (OMO) for nearly four consecutive weeks in March 2026. Total net withdrawal reached approximately VND 187,600 billion, pushing outstanding OMO volume to its lowest since mid-September 2025. Liquidity buffers at many small and medium banks were significantly eroded, forcing them to rely increasingly on expensive interbank funding.Dân trí

More alarmingly, this isn't the first shock of the year. In early February 2026, the overnight rate surged to 17% during the post-Tet period when cash demand spiked dramatically.CafeF The increasing frequency of these liquidity stress episodes is what should truly concern investors.

SBV's emergency injection: VND 90,000 billion

Facing mounting pressure, the SBV swiftly deployed a VND 90,000 billion support package through OMO channels: VND 35,000 billion for 7-day tenor, VND 40,000 billion for 14-day tenor, and VND 15,000 billion for 56-day tenor, all at a uniform 4.5% interest rate. This was the largest net injection since early March, underscoring the severity of the situation.CafeF

But the bigger question remains: if system liquidity were truly abundant — as many reports claim — why would the SBV need such a massive emergency injection? This "firefighting" response reveals that the real picture differs significantly from what surface-level credit growth figures suggest.

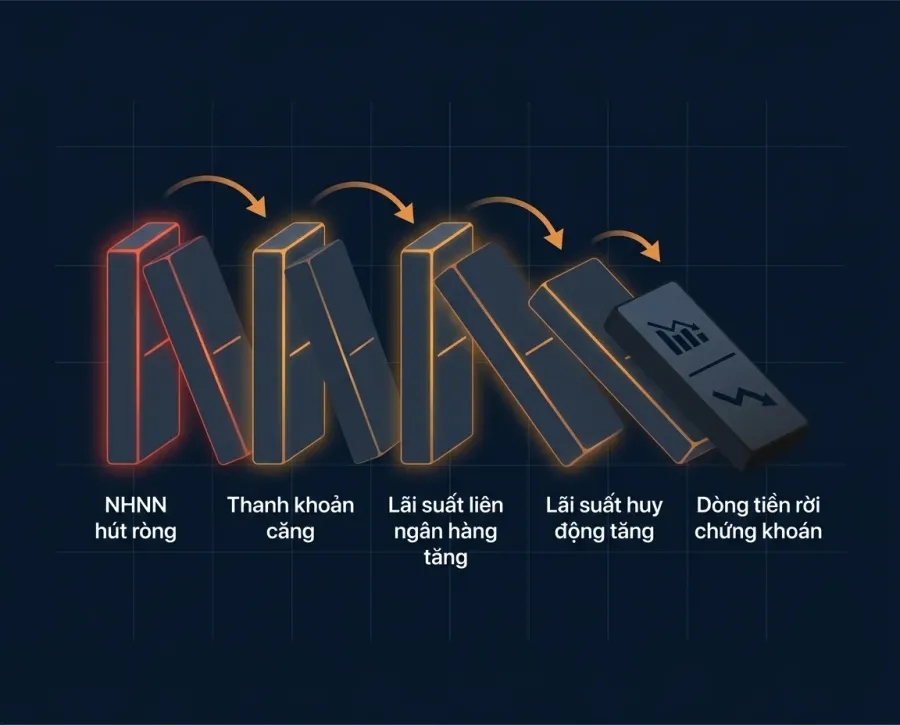

The domino effect: from money markets to your portfolio

When banks borrow from each other at steep rates, the consequences cascade clearly — and the ultimate losers are retail investors.

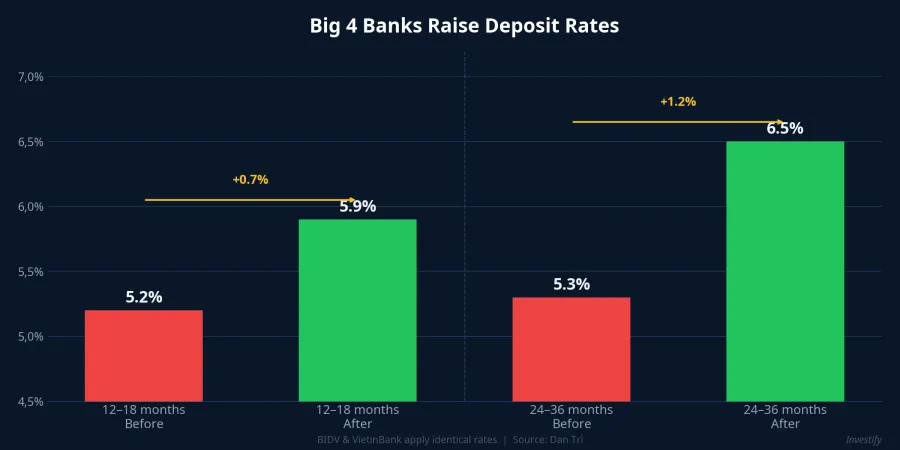

Deposit rates climbing fast. The Big 4 banks simultaneously raised rates. BIDV and VietinBank increased their 12–18 month deposit rate from 5.2% to 5.9%; the 24–36 month tenor jumped from 5.3% to 6.5%.Dân trí Special savings rates at some private banks have already hit 10%.VietnamNet

Rising funding costs squeezing margins. Banks with low CASA ratios (current account savings account) face the most pressure as they must raise deposit rates to retain funds. Net interest margins (NIM) risk compression, directly impacting Q2 banking profits.

Securities margin getting more expensive. Brokerage firms borrow from banks to fund margin lending. When interbank rates rise, their cost of capital increases accordingly, potentially pushing margin interest rates higher or tightening margin room. Leveraged investors should be especially cautious.

Real estate under dual pressure. Mortgage rates currently stand at 12–14% per annum. Combined with February CPI at 3.35% (YoY) and rising input costs economy-wide, homebuyer purchasing power continues to weaken. Capital is shifting from real estate toward savings deposits as deposit rates become more attractive.

What investors should monitor

Instead of watching only price charts and volume, investors should add money market indicators to their dashboard:

- Overnight interbank rate: When it exceeds 8–10%, that's a warning signal that system liquidity is strained. The current 12% sits firmly in the danger zone.

- SBV's OMO activity: Net injection or net drain? What's the scale? This is the system's most important "pressure relief valve." If the SBV continues large injections, liquidity may stabilize temporarily; if it stops too soon, pressure returns.

- Big 4 deposit rates: When all four of the largest banks raise rates simultaneously, it signals an intensifying deposit-gathering race. Money may flow from equities to savings when the rate environment becomes attractive enough.

- USD/VND exchange rate: Currency pressure constrains the SBV's ability to inject liquidity, creating a bind between supporting domestic liquidity and maintaining exchange rate stability.

Green surface, turbulent undercurrents

VN-Index crossing 1,700 is encouraging news, but smart investors look beneath the surface. When overnight rates spike to 12% — nearly triple the normal level — it's a reminder that cash flows within the system are under real stress.

The SBV's timely VND 90,000 billion injection has helped cool things down, but if liquidity pressure continues to build in the coming weeks, the market's rally may lack a solid foundation. OMO developments and deposit rate trends will be the two key variables determining whether VN-Index can sustain above 1,700, or whether this rally is merely the tip of the iceberg.

Risk doesn't always come dressed in red. Sometimes it hides behind the brightest shades of green.