Looking at the Q1 estimates just released by major brokerages, Vietnam's 2026 steel story is opening with more cracks than expected. The shareholder meeting season is in full swing and profit targets have been set at record levels, but the first three months of the year tell a different story. This article walks through each key data point, compares plans against reality, and assesses what these early signals mean for investors.

Record Plans, Modest Reality

Hoa Phat (HPG) has presented its 2026 plan targeting VND 210 trillion in revenue and VND 22 trillion in net profit after tax — a 42% increase over 2025.Fili This is the most ambitious target ever set by Vietnam's largest steelmaker. Yet right in the opening quarter, brokerage estimates already reveal a worrying gap between targets and reality.

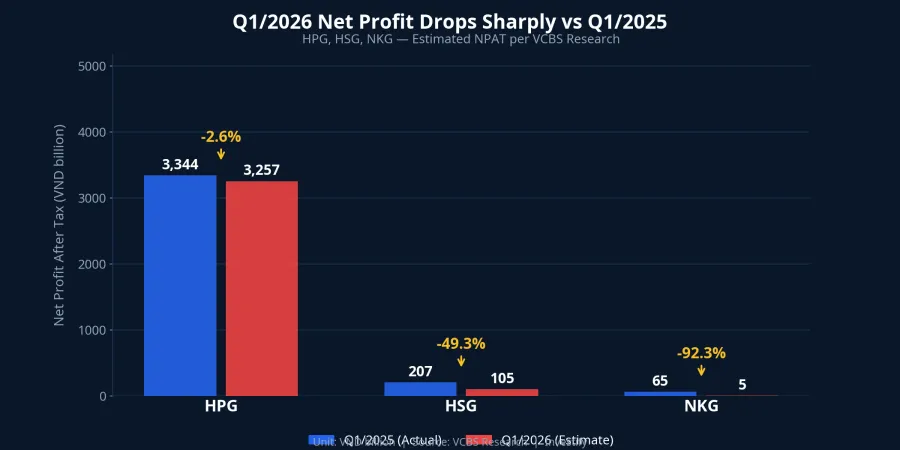

According to VCBS Research, all three major steel companies posted year-on-year profit declines in Q1/2026: HPG fell 2.6% to approximately VND 3,257 billion, Hoa Sen (HSG) dropped 49.4%, and Nam Kim Steel (NKG) plummeted a staggering 92.4%.Nguoi Quan Sat SSI Research paints a more optimistic picture for HPG at VND 5,500 billion (up 64%), but this figure includes extraordinary income from asset transfers — not a reflection of core business health. Even SSI confirmed that the coated steel group HSG and NKG declined 17% and 38% respectively.CafeF

The key takeaway from these numbers: regardless of the scenario — bearish or optimistic — the message is consistent. The steel sector is sharply diverging, and coated steel producers are suffering the most.

HPG: Still Standing, but 22 Trillion Is a Long Road

HPG is trading around VND 27,100/share with a market cap of approximately VND 208 trillion. Based on VCBS's core estimate of roughly VND 3,257 billion for Q1, HPG has only completed about 15% of its full-year target. The remaining three quarters need to average VND 6,250 billion each — significantly above the VND 3,800 to 4,200 billion per quarter that HPG consistently achieved in 2025.

The bright spot lies in volume: Q1 sales volume is estimated at 3.16 million tons, up 18.8% year-on-year, with construction steel growing 26%. Gross margin per SSI may reach 15.4%, up 1.2 percentage points year-on-year thanks to lower raw material costs. But the disconnect between rising volume and flat profit points to severe selling price pressure — the company is moving more steel while earning less per ton.

NKG and HSG: Coated Steel Is Bleeding

Nam Kim Steel (NKG) stands at VND 14,000/share with a market cap of VND 6,300 billion. With Q1 net profit estimated to decline between 38% and 92% depending on the source, NKG faces the greatest risk among the three. Its Q4/2025 gross margin had already fallen to just 2.3% — virtually no cushion to absorb raw material price swings.

Hoa Sen (HSG) trades at VND 15,050/share, market cap VND 9,300 billion. Its fiscal Q1 (October-December 2025) already recorded an 18% revenue decline and 62.3% drop in net profit, with gross margin compressing to 11.2% as lower sales volume pushed up fixed costs per unit.Thuong Hieu Cong Luan Both coated steel producers are trapped in a vicious cycle: thin margins, export dependency, and mounting competitive pressure.

Four Structural Pressures Squeezing Margins

Looking at the profit declines, the natural question is: why? It is not a single cause but rather four structural pressures converging simultaneously on the steel sector.

Domestic oversupply is the first pressure. Coated steel capacity expanded by 1.4 million tons per year (from NKG and GDA), while the sector's capacity utilization sits at only about 68%. Companies are forced to compete on price, eroding margins quarter after quarter.

The EU's CBAM took effect on January 1, 2026, adding USD 70 to 80 per ton in costs for steel exported to the EU.VnEconomy Vietnam's steel exports to the EU had already dropped approximately 38% even before CBAM charges were fully applied.VietnamBiz

US tariffs of approximately 50% have effectively closed the American market. But the indirect effect is more concerning: Chinese steel blocked from the US will redirect to Southeast Asia, intensifying price competition on home turf.

Cheap Chinese steel is the underlying driver. China exported a record roughly 108 million tons in the first 11 months of 2025, while shifting to low-priced billet sales to circumvent tariffs, dragging down finished steel prices across ASEAN.

H2 2026 Outlook: Conditional Hope

Q2/2026 is expected to improve thanks to peak construction season and HRC prices stabilizing around USD 1,063 per ton. The second half of 2026 could be more positive if three conditions converge: accelerated public investment disbursement (North-South expressway, Long Thanh airport), anti-dumping trade defense measures on HRC, and China implementing steel export controls.

However, the risks are equally clear: if China continues dumping, the EU tightens quotas mid-year, or real estate recovery stalls, HPG's VND 22 trillion target will be very difficult to achieve — and coated steel producers could face yet another tough year.

What Are Steel Stocks Telling Us?

The 3-month stock price chart reveals clear divergence. HPG has traded roughly flat, holding near its period-start level — reflecting market confidence in its leading position and integrated production chain. Meanwhile, HSG and NKG have both lost significant value, with NKG under the heaviest pressure.

Q1 is not the final verdict for the full year, but it is an important warning signal. HPG remains the safest pick in the steel group thanks to its large domestic market and low production costs — investors should wait for official financial statements (expected late April) to confirm core margins. For HSG and NKG, thin margins combined with export dependency and domestic oversupply create a risk trifecta that is difficult to resolve in the short term.

Stock prices as of the morning session on March 31, 2026. Q1/2026 data are estimates from VCBS and SSI Research, not official financial statements.