Looking at the figures MB Bank (MBB) just presented in its 2026 Annual General Meeting documents, there are two common reactions: admiration for the consistent growth trajectory, and skepticism about the feasibility of certain targets. Both reactions are well-founded — and this article breaks down each number so investors can judge for themselves.

The Profit Picture: Is VND 39,500 Billion Realistic?

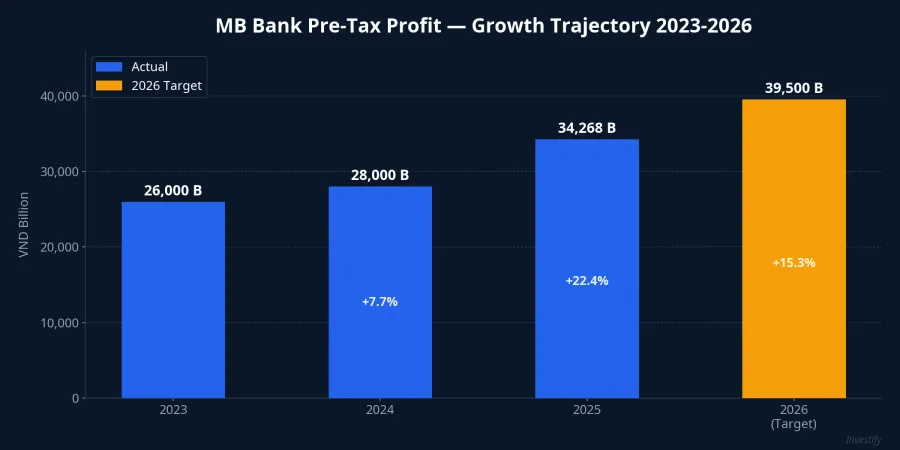

MB targets consolidated pre-tax profit of approximately VND 39,500 billion for 2026, representing a roughly 15% increase over the VND 34,268 billion achieved in 2025.CafeF In the context of the past three years, MB's profit growth has been remarkably steady: from VND 26,000 billion (2023) to VND 28,000 billion (2024, +7.7%) then VND 34,268 billion (2025, +22.4%). The 15% target for 2026 is actually more conservative than last year's achievement.

What stands out in the financials is MB's operational efficiency, which ranks among the best in the industry: ROE around 21-22%, ROA approximately 2%, and a cost-to-income ratio (CIR) of just 29-30%. With this foundation, the VND 39,500 billion profit target is highly achievable if credit growth reaches 20-25% and net interest margin (NIM) remains stable. However, that "if" is precisely where the challenge lies.

Total Assets of VND 2 Quadrillion — Unprecedented Pace

The most striking figure is not profit but the target to surpass VND 2 quadrillion in total assets — a 28% increase from VND 1.616 quadrillion at end-2025. This comes alongside 30% credit growth and 30% deposit mobilization growth targets.Nhip Song Kinh Doanh

If achieved, MB would become the fastest private bank in history to go from VND 1 quadrillion to VND 2 quadrillion in total assets. To support this, MB plans to increase charter capital from VND 80,550 billion to a maximum of VND 102,687 billion through stock dividends (15%), rights issues (10%), and private placements — officially joining the "VND 100,000 billion charter capital club" alongside VPBank.

However, 30% credit growth requires MB to disburse hundreds of trillions of dong more at a time when deposit rates are climbing, system-wide funding costs are rising, and businesses face pressure from surging fuel prices and shipping costs. The critical question: who will borrow at higher rates and still be able to service their debt?

NIM Compression — An Early Warning Signal

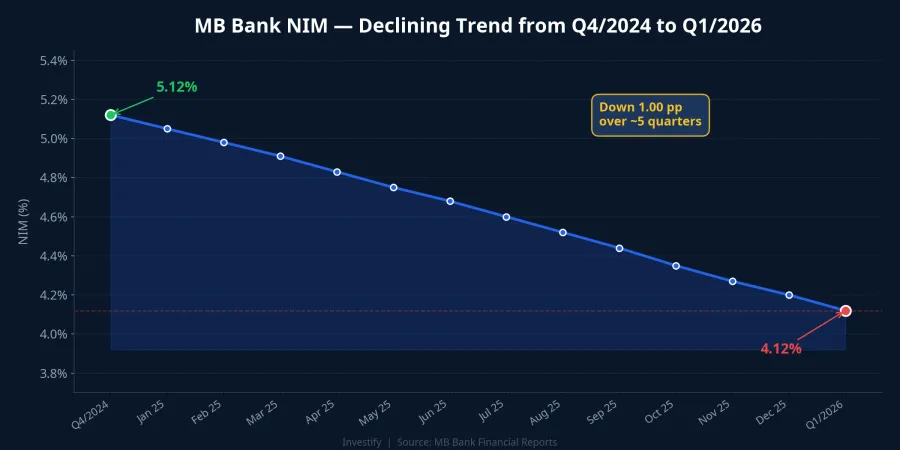

MB's net interest margin has been declining steadily: from above 5.12% in Q4/2024 to approximately 4.12% in early Q1/2026 — a full 1 percentage point drop over just 5 quarters. This is a direct consequence of rising deposit rates as CPI hit 3.35% and Brent crude surpassed $107 per barrel.

MB benefits from a CASA (current account savings account) ratio around 36-37% — among the highest in the industry — which helps keep average funding costs down. But as the Big 4 state-owned banks have already begun raising deposit rates to retain deposits, the competition will push funding costs higher across all banks, MB included. The pace of CASA improvement in coming quarters will be the deciding factor in whether NIM stabilizes or continues to slide.

Three New Pillars: FDI, Gold, and Digital Assets

Beyond scale expansion, MB is branching into three entirely new business lines: serving FDI enterprises, gold trading, and digital assets.Tap Chi Cong Thuong With global gold prices exceeding $4,547/oz, the gold trading segment has significant fee income potential. However, gold's extreme price volatility demands specialized risk management capabilities that MB has not previously tested at this scale.

The digital assets segment poses even greater challenges given Vietnam's lack of a clear regulatory framework. Investors should closely monitor implementation progress and actual fee income contributions rather than building in premature expectations.

Industry Comparison: Where Does MB Stand in the Race?

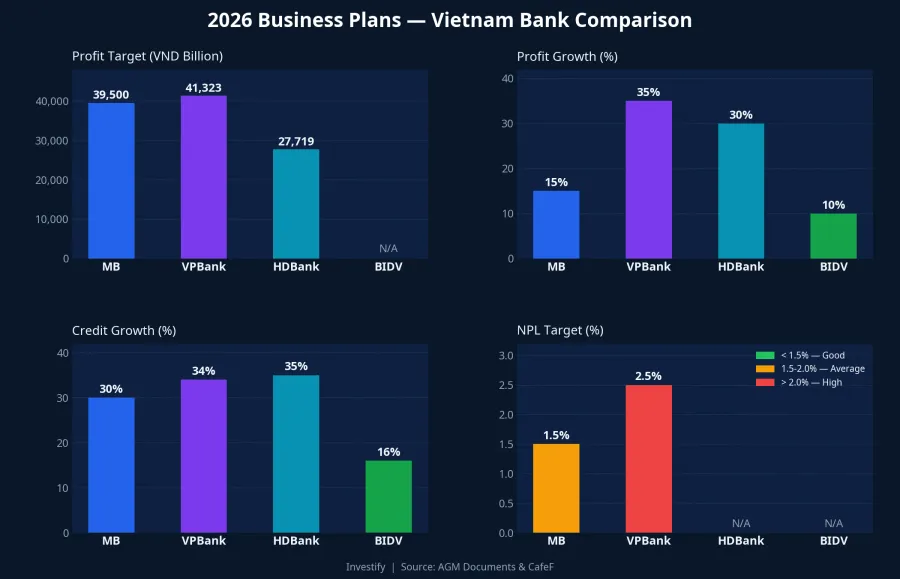

The 2026 AGM season features an intense growth race among major private banks. VPBank targets VND 41,323 billion profit (+35%) with 34% credit growth but accepts NPL targets widening to below 2.5%. HDBank aims for over VND 27,719 billion (+30%) with 35% credit growth. Meanwhile, the Big 4 state-owned banks are more conservative with 15-16% credit growth and around 10% profit growth.CafeF

MB occupies the middle ground: more ambitious than the Big 4 but more conservative than VPBank on profit growth. MB's clearest competitive advantages are its high CASA ratio and low CIR — two metrics showing the bank sources cheaper funding and operates more efficiently than most peers. Combined with aggressive capital-raising plans, MB has a better safety margin than many banks with similar credit growth ambitions.

Key Risks to Watch Before the April 18 AGM

MBB shares are trading around VND 25,750 per share (March 30 session) with a market cap of approximately VND 207,400 billion. Ahead of the April 18 AGM, investors should pay close attention to four critical factors. First, the SBV credit quota allocated to MB — the 30% growth target requires a corresponding room allocation, a variable entirely outside the bank's control. Second, NPL and Group 2 loan trends, particularly in the real estate segment and among businesses under cost pressure — data shows MB's NPL already edged up slightly during 2024 to early 2025, though it remains controlled at 1.29-1.3%. Third, the pace of CASA improvement will determine NIM stability. And finally, the rollout progress of gold trading and digital assets will reveal whether MB is diversifying revenue in the right direction or simply adding operational risk.

In summary, the VND 39,500 billion profit target is well within reach given MB's industry-leading operational foundation. But total assets of VND 2 quadrillion and 30% credit growth are significant challenges, heavily dependent on macroeconomic conditions beyond MB's control. The numbers tell a compelling story — but those same numbers demand that investors remain clear-eyed.