Looking at the numbers from the March 31, 2026 session, many investors found themselves puzzled: DPM dropped 3.4% to VND 29,800 and DCM fell 3.57% to VND 47,250 — among the session's steepest declines — while the VN-Index actually ticked up 0.38%. What makes this particularly striking is that global urea prices are at their highest since October 2022, with FOB Middle East hitting USD 674/ton — a 70%+ surge since the start of the year.Thoi bao TCVN

So is this a market paradox, or a puzzle that financial data can explain more clearly?

Hormuz — The Supply Shock Behind a 3-Year Urea High

The direct catalyst for the urea price spike is the shipping disruption at the Strait of Hormuz. Escalating Middle East conflict has stranded approximately 570,000 tons of urea in the Persian Gulf, slashing global urea exports in March from a normal 3.5-5 million tons down to just 1.5 million tons.Thoi bao TCVN This is a sustained supply shock, not short-term speculative volatility.

However, the more important question for Vietnamese investors is not "what is global urea worth" but rather "how much of that price flows through to DPM and DCM." The answer lies in each company's specific business structure.

2026 Targets "Go Backward" — Strategy or Genuine Pessimism?

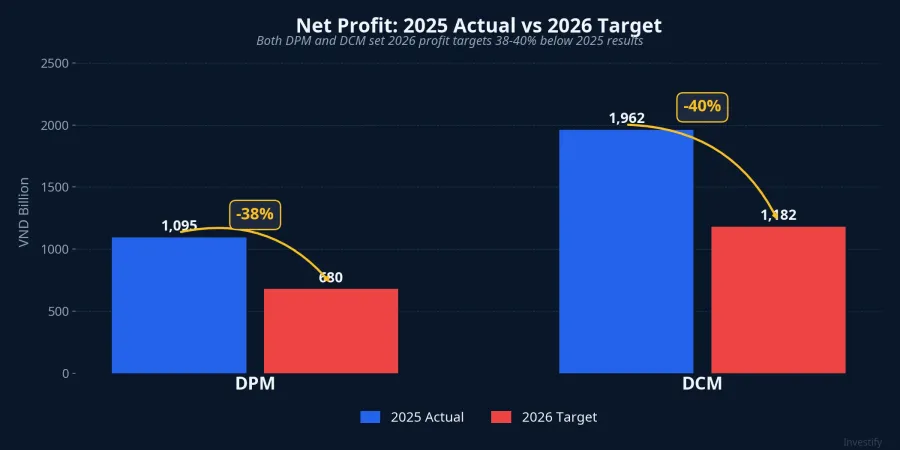

In 2025, both companies delivered impressive results. DPM posted revenue of VND 16,564 billion (+23%), with after-tax profit of VND 1,095 billion — exceeding its target by 60%.Vietstock DCM performed even better with revenue of nearly VND 17,033 billion (+21%) and after-tax profit of VND 1,962 billion, up 37% year-on-year.Tin nhanh CK

Yet their 2026 plans sent chills through the market. DPM set a net profit target of just VND 680 billion — down 38% from 2025 actuals, with a projected 12% dividend.Thoi bao TCVN DCM was even more conservative at roughly VND 1,182 billion, a 40% cut, with dividends halved to 10%.Vietstock

Management cited "geopolitical instability and extreme weather" as reasons. But historically, this is a common practice among state-owned enterprises — setting low targets to easily report "exceeded plan" by year-end. DPM beating its 2025 plan by 60% is a case in point. Investors should not treat the 2026 target as a real forecast but instead cross-reference it with urea price trends and the upcoming Q1 results.

Three Barriers Preventing Global Urea Prices from Flowing to Shareholders

Many investors make the mistake of equating "urea prices up" with "DPM/DCM profits soar." In reality, three structural barriers stand in the way.

First, a domestic-oriented market. DPM supplies approximately 40% of domestic urea demand, while DCM primarily serves the Mekong Delta region. Export volumes remain modest, so international FOB prices do not translate directly into revenue.

Second, regulated domestic pricing. In March 2026, domestic urea prices fluctuated sharply between VND 10.8 million and VND 19 million per ton. Mid-month peaks of VND 18-19 million gave way to end-of-month cooling at VND 10.8-13 million — showing that the ability to pass through international prices is significantly constrained.SFarm

Third, natural gas costs — the decisive variable. Natural gas accounts for an estimated 60%+ of urea production costs. DPM's gross margin in 2025 was only 17-20%, while DCM achieved 19-24%. With Brent crude already above USD 115/barrel, rising gas input costs from PVN could erode margins even as selling prices improve. This is precisely why the market remains skeptical — revenues may grow, but costs could grow faster.

Low-Cost Inventory — A Short-Term Trump Card, Not a Long-Term Story

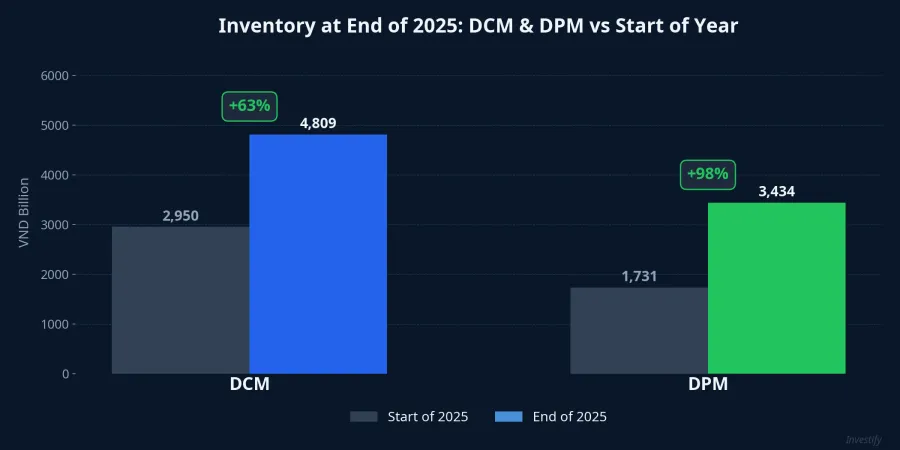

The clearest bright spot in the financial picture is inventory built up before prices surged. At end of 2025, DCM's inventory reached VND 4,809 billion, up 63% from the start of the year. DPM nearly doubled to VND 3,434 billion.Nha dau tu

The spread between low acquisition costs (purchased before the Hormuz crisis) and current high selling prices should significantly boost Q1/2026 margins. Some estimates suggest profits could double in the first quarter thanks to this inventory effect alone.24hMoney

However, investors must recognize this is a one-time windfall. Once low-cost inventory is sold through, margins revert to normal. Moreover, if the Hormuz situation de-escalates and urea prices correct, the risk of inventory write-downs becomes very real — a cost that hits profits directly.

Pre-AGM Checklist for April

DCM holds its AGM on April 22, with DPM expected to follow later in the month. Given the current unique circumstances, five variables will determine the valuation story next quarter:

- Hormuz developments — de-escalation could trigger rapid urea price corrections and inventory risk.

- Gas input pricing from PVN — determines actual margins, not just revenue.

- Q1/2026 results — if they far exceed the full-year plan in just one quarter, the market will be forced to reprice.

- China's urea export policy — any relaxation would add supply and dilute current price levels.

- AGM content — whether management will raise targets given more favorable-than-expected conditions.

Follow the Numbers — Patience Before Action

DPM and DCM find themselves in a rare situation: pessimistic targets but reality trending better than expectations, commodity prices supportive but the cost structure not yet allowing full benefit. This is not a simple "buy the dip" story — it is a problem requiring patience for two critical data points: Q1/2026 earnings and the specific content of April's AGMs. Investors should clearly distinguish between "one-time inventory profits" and "sustainable growth" before committing capital.