Looking at the numbers alone, Vietcap Securities' (VCI) 2026 business plan is hard to fault: revenue target of VND 6,525 billion, pre-tax profit of VND 2,300 billion — an all-time high, up 41% versus 2025 actuals. Yet on the very day of the Annual General Meeting (March 30, 2026), VCI shares dropped over 2%, extending a roughly 15% decline through March. What is the market seeing that the headline numbers do not show?

The 2025 Foundation — Solid, Not Spectacular

VCI's 2025 results were genuinely strong. Revenue reached approximately VND 5,021 billion and pre-tax profit hit VND 1,629 billion — exceeding the shareholder-approved plan by 16% and 15%, respectively.Doanh nghiep & Hoi nhap Proprietary trading (FVTPL) remained the key profit driver with over VND 942 billion, while brokerage revenue came in around VND 1,000 billion on improved market liquidity.

These numbers gave management the confidence to target 41% profit growth for 2026. However, reaching VND 2,300 billion requires strong growth across every business segment — a tall order when the VN-Index is in correction mode, sliding to 1,662 points as of March 30.

The Dilution Problem — Why the Market Is Selling the News

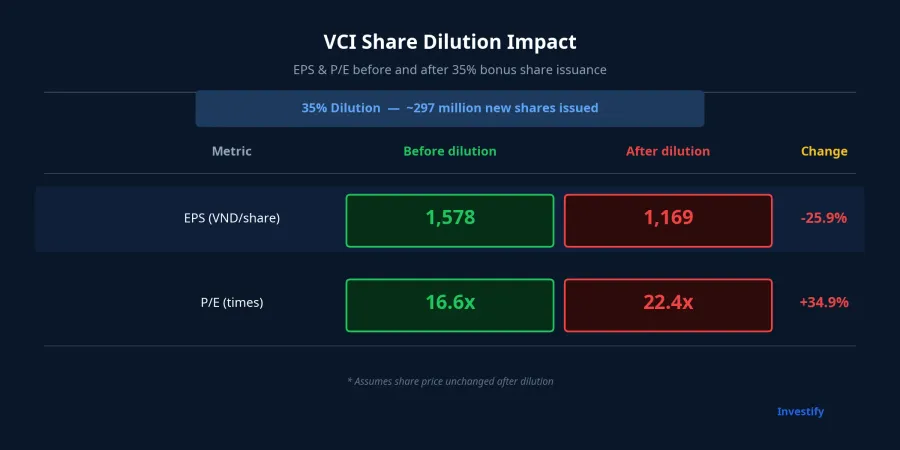

The most significant agenda item at the AGM was not the profit target but the proposed 20:7 bonus share issuance (equivalent to 35%). With 850.1 million shares outstanding, VCI would issue approximately 297.5 million new shares, bringing the total to nearly 1,148 million shares.Vietstock

The arithmetic is straightforward: EPS drops roughly 26% — from VND 1,578 to VND 1,169 per share — even if profit grows 41%. Post-dilution P/E rises from 16.6x to 22.4x, a level no longer attractive relative to sector peers. On top of this, a plan to issue up to 4.6 million ESOP shares at a preferential price of VND 11,000 adds further dilution pressure.Bao Moi

This is a familiar story in Vietnam's equity market: a company delivers solid growth, but the mechanism for sharing that growth leaves minority shareholders feeling "silently diluted." You receive more shares, but the intrinsic value per share shrinks — like a pie sliced into more pieces, with each piece getting smaller.

FTSE Russell — A Strategic Card Not Yet Fully Priced In?

Just eight days remain before FTSE Russell announces its interim review results on April 7, 2026 — the final checkpoint before officially adding Vietnam to the FTSE Emerging Index from September 2026.FTSE Russell VCI is among the 28 stocks in the projected FTSE Global All Cap Index inclusion list, alongside SSI, HCM, and VND.VnEconomy

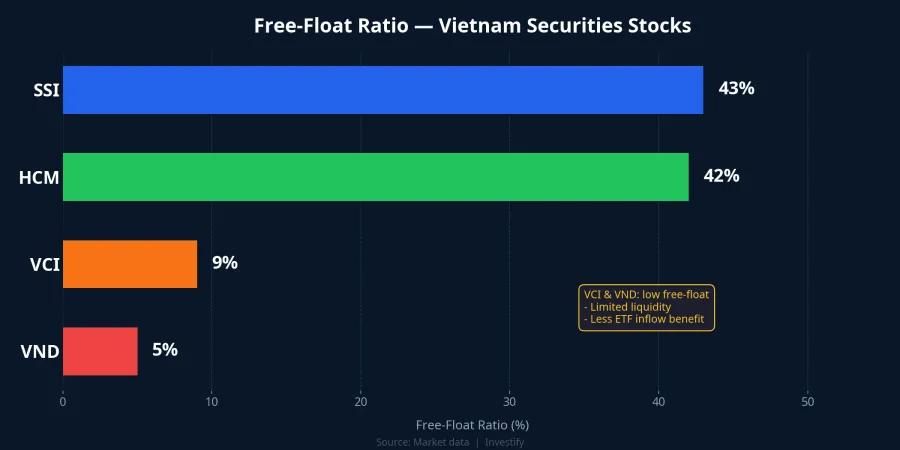

Multiple research houses estimate that passive ETF inflows into Vietnam could reach USD 500 million to USD 1.5 billion in the initial phase following the upgrade, led by the Vanguard FTSE Emerging Markets ETF (AUM exceeding USD 100 billion). However, VCI stands to benefit significantly less than SSI or HCM from these flows. The reason is free-float: VCI's free-float ratio sits at approximately 9%, compared to 43% for SSI and 42% for HCM. With a lower free-float weighting, passive capital allocated to VCI is estimated at just USD 40-80 million — a modest figure relative to expectations.

Where Does VCI Stand Among Listed Peers?

To put these numbers in context, a quick comparison between VCI and its two largest peers paints a clear picture:

| Metric | VCI | SSI | HCM |

|---|---|---|---|

| Price (Mar 30) | 26,150 | 26,550 | 22,300 |

| Market cap | VND 22,200 bn | VND 66,100 bn | VND 24,100 bn |

| P/E | ~16.6 | ~18-20 | ~14-16 |

| Free-float | ~9% | ~43% | ~42% |

| 1-month change | -15% | -12% | -8% |

VCI appears more attractively valued than SSI on current P/E, but after the 35% dilution this advantage virtually disappears. The low free-float also means limited liquidity and smaller passive ETF inflows — two factors the market is pricing in quite clearly through share price action.

A Balanced View for Investors

VCI's story reflects a common paradox in Vietnam's stock market: ambitious growth plans paired with heavy dilution. Investors should consider three time-horizon scenarios.

In the short term, the 35% dilution overhang and sell-the-news sentiment could continue weighing on the stock for several weeks, especially while the VN-Index has not confirmed a recovery trend. On a medium-term view, should FTSE Russell confirm the upgrade on April 7, the entire securities sector — VCI included — would benefit from foreign capital expectations, with the strongest rally phase typically occurring 3-6 months before the effective date (September 2026).

Regarding risk, the VND 2,300 billion profit target relies heavily on proprietary trading — a segment inherently volatile and market-dependent. If the VN-Index continues to correct, the ability to meet this plan could come under serious threat. Retail investors need to distinguish clearly between "real growth" — where earnings per share actually increase — and "paper growth" — where total profit rises but gets diluted by new share issuance.