This policy opens the biggest opportunity in a decade for Vietnam's stock market. On April 7, 2026, FTSE Russell will announce the results of its interim assessment — the final checkpoint before officially including Vietnam in the FTSE Emerging Index starting September 21, 2026. If Vietnam passes, billions of dollars from international investment funds will begin flowing into the market. But this roadmap is not without risks, and investors need to understand each link in the chain before taking action.

From Frontier to Emerging — a long journey

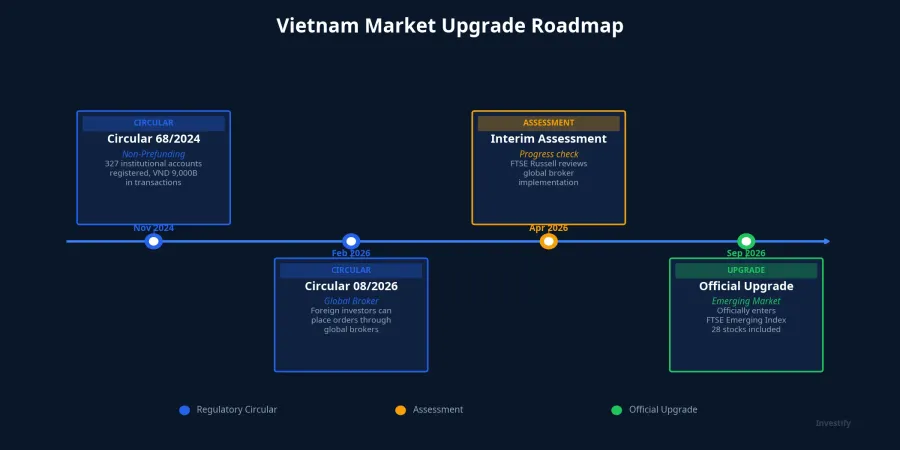

In October 2025, FTSE Russell officially announced Vietnam's reclassification from Frontier Market to Secondary Emerging Market, conditional on passing the interim assessment scheduled for March 2026.LSEG This is not an automatic decision — FTSE needs to confirm that market infrastructure reforms have been implemented in practice, not just on paper.

According to the roadmap, the assessment focuses on one critical criterion: international investor accessibility through global brokers — meaning foreign institutional investors can place orders through international brokerage firms without opening accounts at Vietnamese securities companies.FTSE Russell FAQ This is the final technical barrier Vietnam needs to clear.

Three reform milestones already completed

Over the next 3-5 years, the outcome of the upgrade roadmap will depend on the reform foundation already built. And in reality, Vietnam has met most of FTSE Russell's technical requirements through three critical reforms.

First, the Non-Prefunding (NPF) mechanism. Circular 68/2024/TT-BTC took effect on November 2, 2024, allowing foreign investors to place buy orders without having sufficient funds in their accounts at the time of order placement. In the first month of implementation, 327 foreign institutional accounts registered, executing over 19,000 transactions worth approximately VND 9,000 billion.Bao Dau Tu

Second, the failed trade resolution process now has an official mechanism. This is a technical requirement that many frontier markets overlook but is a necessary condition for international funds to trade with confidence.

Third and most importantly — Circular 08/2026, the final piece of the puzzle, took effect on February 3, 2026. This circular allows foreign investors to place orders through global brokers without opening accounts at domestic securities companies.VnEconomy This reform is the decisive factor in whether FTSE Russell will give the green light in the April 7 assessment.

Expected capital flows — billions of dollars at stake

According to the roadmap, if the upgrade succeeds, capital will flow in three phases of increasing scale. Passive capital — from ETFs tracking the FTSE Emerging Index that must buy Vietnamese stocks to match weightings — is estimated at $0.8 to $1.5 billion according to HSBC Global Research.Vietnam Briefing This is virtually guaranteed money, as passive funds have no choice — they must buy when the index changes.

Active capital typically runs 3-5 times passive flows, coming from institutional funds making their own allocation decisions. The World Bank estimates total short-term inflows at approximately $5 billion, with long-term flows potentially reaching $25 billion by 2030. In terms of timing, active funds have already begun portfolio restructuring, while passive ETFs will concentrate their buying around the effective date of September 21, 2026.

28 stocks in the crosshairs

FTSE Russell has preliminarily identified 28 stocks eligible for inclusion in the FTSE Emerging basket: VIC, VHM, HPG, MSN, VCB, VNM, SSI, STB, VJC, VRE, SHB, VND, GEX, KBC, KDH, FRT, DGC, EIB, PLX, SAB, DIG, DXG, VIX, VCI, HUT, DPM, PDR, KDC.Vietnam News These stocks were filtered by minimum market capitalization of $150-165 million, free-float of 5-10%, adequate liquidity, and remaining foreign ownership room. The official list will be announced during FTSE's semi-annual review in September 2026.

Notably, not all stocks will benefit equally. Those with significant remaining foreign room — such as securities firms (SSI, VND, VCI) and real estate (KDH, PDR) — will have greater upside potential compared to blue chips where foreign ownership is nearly maxed out.

Lessons from Saudi Arabia and Kuwait — upgrades don't guarantee short-term gains

Looking globally, the experience of previously upgraded markets paints a two-sided picture. Saudi Arabia was upgraded by FTSE in March 2019 — the market rose 10% in the announcement year. More impressively, Saudi's weight in the FTSE Emerging Index grew from 0.3% to 4.2%, with foreign capital increasing more than fourfold from $23.1 billion to $97.5 billion by Q3 2023.MSCI

In contrast, Kuwait was upgraded in September 2018 but gained only 3.5% before the upgrade, then weakened due to US interest rate volatility and oil price swings. The lesson is clear: upgrades improve market structure and attract long-term foreign capital, but do not guarantee short-term price increases. External macro factors can still overshadow the upgrade effect.

Risks to consider before April 7

Despite the optimism, investors should remain clear-headed about three key risks. First, the global broker mechanism only took effect in February 2026 — less than two months before the assessment. If FTSE Russell deems the operating period insufficient for evaluation, they could well postpone the upgrade timeline. Second, foreign ownership room at many blue chips is nearly full — limiting foreign funds' buying capacity even if the upgrade succeeds. Third, the macro environment is not entirely favorable, with CPI at 3.35%, rising interest rates, and exchange rate pressure.

The VN-Index sits at 1,672.8 points following a weekly recovery of +2.85%. The "buy before the event" strategy always carries significant risk — especially when the market has already partially priced in upgrade expectations. Investors should prioritize stocks with ample remaining foreign room, high liquidity, and solid business fundamentals — rather than chasing rumors. April 7 will be the defining day for the upgrade roadmap, but the investment journey always requires looking beyond a single event.