The big picture reveals a global financial market entering a phase of sharp divergence. On one side, Wall Street is drowning in a selloff wave driven by geopolitical crisis. On the other, VN-Index has just snapped a 3-week losing streak. Capital flows are following contradictory signals — and the week of March 30 will be a critical test for Vietnamese investors.

Wall Street Officially Enters Correction Territory

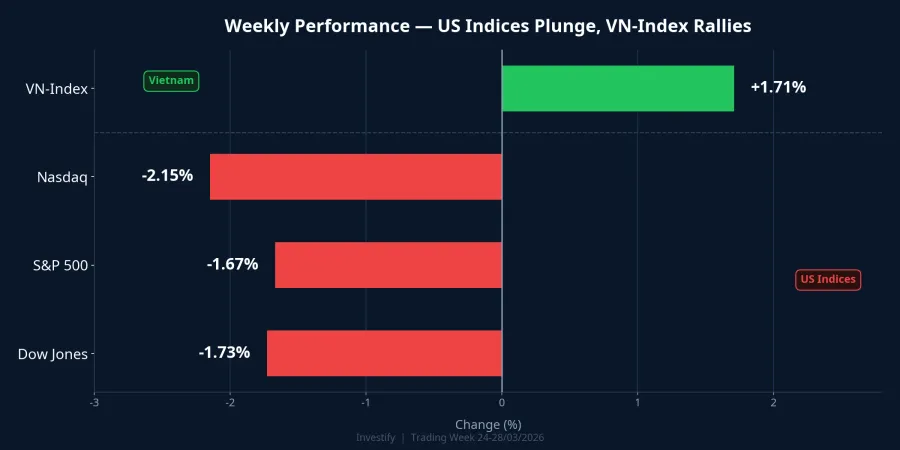

In the final session on March 27, the Dow Jones plummeted 793 points (1.73%) to 45,167, officially entering correction territory after losing more than 10% from its peak. The S&P 500 fell 1.67% to 6,369 — its lowest level in 7 months. Most alarming was the Nasdaq, which lost 2.15% and marked its fifth consecutive weekly decline.CNBC

The primary catalyst is the Strait of Hormuz crisis — a maritime chokepoint that handles approximately 20 million barrels of oil per day. Iran has imposed sweeping restrictions, allowing only "non-hostile" vessels to pass, reducing cargo flow through the strait by roughly 95% since early March.Wikipedia Alternative routes can only accommodate about 9 million barrels per day — meaning more than half the supply is completely stranded.

The direct consequence: Brent crude closed at $112.57 per barrel on March 27, surging 4.22% in a single session to reach its highest level since mid-2022.Fortune US 10-year Treasury yields climbed to the 4.42-4.48% range, reflecting expectations that the Fed will maintain higher rates for longer than anticipated. This is a classic adverse combination for capital flows into emerging markets — including Vietnam.

VN-Index Rallies But Foreign Investors Tell a Different Story

While Wall Street was bathed in red, VN-Index delivered a notable recovery week. The index closed on March 27 at 1,672.8 points, gaining 1.71% in the session and ending a 3-week losing streak that had wiped out 232 points (12.3%). This is a positive signal, but the capital flow picture is far more nuanced.

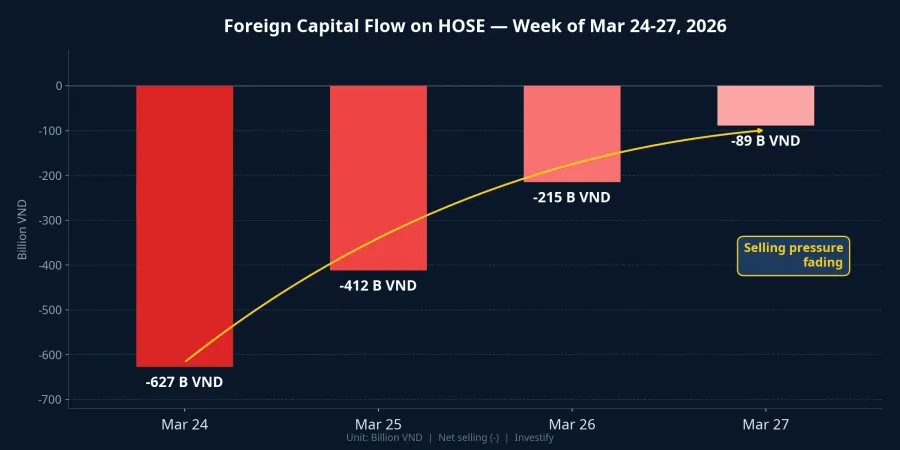

Foreign investors sold a net VND 2,500 billion on HOSE during the week of March 24-27. VIC was the most heavily offloaded at VND 3,594 billion, followed by HPG (VND 810 billion), FPT (VND 611 billion), and STB (VND 560 billion). On the buying side, MCH attracted the strongest inflows (VND 1,031 billion), along with SHB and VRE.VietnamBiz

However, the encouraging detail lies in the rapidly declining selling pressure. From VND 627 billion on March 24, net selling shrank quickly to just VND 89 billion by March 27.CafeF Selling momentum is fading — and while the overall trend has not yet reversed to net buying, this signals that the worst of the "dumping" phase may be behind us.

Two Opposing Forces for the Week of March 30

The outlook for the coming week is shaped by two clearly opposing forces, which could trigger significant volatility before the market settles on a direction.

Bearish forces stem from three key factors. First, VN-Index has not yet priced in the Dow's sharp decline on March 27 (since the US market closes after Vietnamese trading hours), so the opening session on March 31 could face substantial gap-down pressure. Second, Brent crude above $112 directly impacts transportation costs, CPI inflation, and exchange rate pressure — airlines (HVN, VJC) have already slashed thousands of flights, while fertilizer and chemical companies face surging input costs. Third, rising US Treasury yields create headwinds for capital flows into emerging markets.

Bullish forces are equally compelling. FTSE Russell will announce its interim assessment results on April 7 — a crucial step before Vietnam's official upgrade to Secondary Emerging status on September 21, 2026.FTSE Russell Vietcap assesses the probability of not achieving the upgrade at 0%, meaning the market is virtually certain to receive positive news. Additionally, Q1/2026 earnings season kicks off in early April with expectations of improvement in banking and construction materials sectors. End-of-quarter portfolio rebalancing may also create opportunities for active traders.

Technical Analysis: The 1,700 Zone Is the Decisive Test

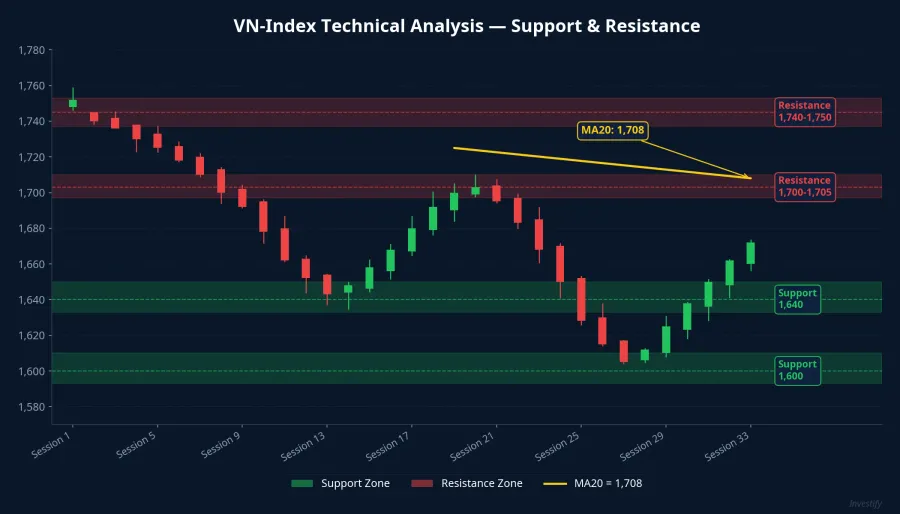

According to weekly strategy reports from ASEAN Securities and Vietstock, the technical picture shows VN-Index at a critical juncture.ASEAN SecuritiesVietstock

The nearest resistance sits at 1,700-1,705, coinciding with the MA20 at 1,708 — the "wall" that VN-Index must break through to confirm the recovery trend. Stronger resistance lies at 1,740-1,750 (near the MA100 at 1,744). On the downside, near support is at 1,640 and strong support at 1,600-1,612. The RSI at 43.33 shows remaining upside potential but lacks strong momentum, while the MACD remains negative. Liquidity around VND 20,000 billion per session is below the previous month's average.

Three Scenarios for Investors

Scenario 1 — Continued Recovery, Testing 1,700 (medium probability): VN-Index breaks above 1,700 if Wall Street pressure is absorbed quickly in the opening session and liquidity improves. The prerequisite is foreign investors reducing selling or shifting to net buying.

Scenario 2 — Sideways Consolidation at 1,640-1,700 (highest probability): The market oscillates within a narrow range as cautious money waits for FTSE Russell on April 7. This scenario favors short-term trading strategies — buying near support, taking profits near resistance.

Scenario 3 — Correction to 1,600 (low probability but warrants vigilance): This occurs if oil continues rising past $120 and Wall Street declines further. In this case, the 1,580-1,600 zone becomes the "last line of defense" — and an attractive accumulation zone for medium-term investors.

Key Events for the Week of March 30 - April 3

- March 31: Vietnam PMI for March (S&P Global) — manufacturing health indicator

- April 1: US ISM Manufacturing PMI, JOLTS — labor market signals

- April 2: US ADP Employment — early preview of Non-Farm Payrolls

- April 3: US Weekly Jobless Claims, Retail Sales

- April 7: FTSE Russell announces Vietnam interim assessment results — the focal event

Capital is shifting between two opposing poles: geopolitical risk pulling money out of risky assets, while the FTSE upgrade narrative anchors long-term capital. In this context, investors should maintain a cautious equity allocation, prioritizing fundamentally strong stocks that have already been discounted heavily. Increase exposure only if VN-Index decisively clears 1,705 with clearly improving liquidity. This is a week for observation — not for going all-in.