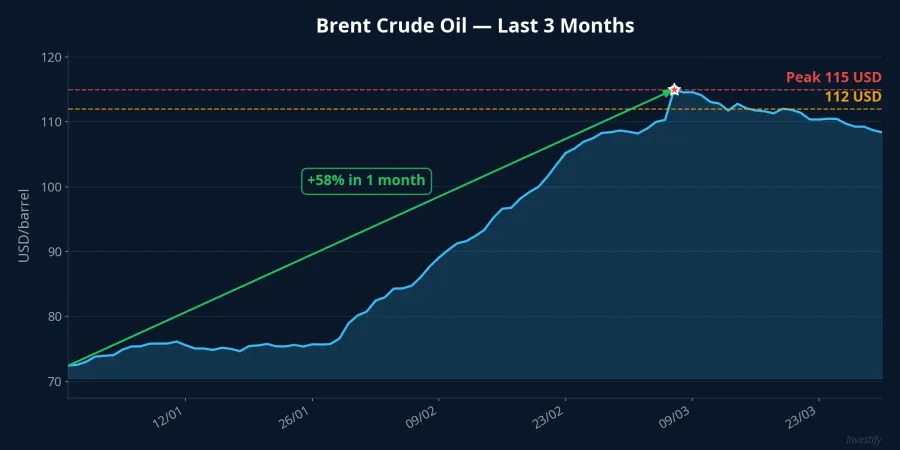

The big picture reveals a fascinating paradox: as Brent crude smashes through the $112/barrel mark and approaches its $115 peak — the highest since mid-2022 — most of the economy is buckling under soaring energy costs. Airlines are cutting flights, logistics costs are climbing, and CPI inflation has hit 3.35%. Yet in another corner of the market, money is flooding into renewable energy and power construction stocks.

On March 25, 2026, a wave of power sector stocks including NT2, REE, PC1, TTA, and GEG simultaneously hit ceiling prices with surging volume — NT2 alone traded over 2.9 million units, triple its previous session.Vietnambiz The VN-Index recovered to the 1,672-point zone after three weeks of decline, with the power sector serving as one of the key pillars. What is driving this?

Oil Price Shock — But Who Benefits?

This oil shock stems from escalating geopolitical tensions in the Middle East, particularly after Houthi attacks on Israel and President Trump's remarks about controlling Iranian oil.CNBC Brent surged nearly 58% in just one month — a pace rarely seen since the early days of the Russia-Ukraine conflict in 2022.

The answer to this paradox lies in input costs. Wind, solar, and hydropower do not depend on fossil fuels. When oil prices rise, production costs for renewable plants remain virtually unchanged, while electricity selling prices tend to increase with energy inflation. In other words, their profit margins widen naturally — the exact opposite of gas-fired power plants whose fuel costs are eroding margins daily.

According to SSI Research, electricity demand in 2026 is projected to grow approximately 8.5% year-over-year (high scenario: 10-15%), with the wholesale electricity market price (FMP) forecast to recover by around 29%.Vietnambiz El Nino conditions may reduce hydropower output, increasing dispatch from other sources — creating additional opportunities for wind and solar power.

PC1 — Record Backlog of VND 8,250 Billion Opens a New Growth Cycle

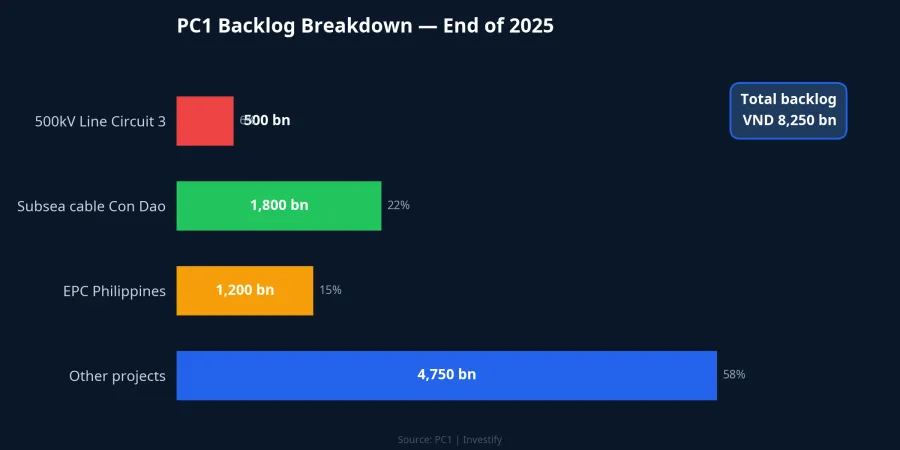

Capital flows are shifting most visibly toward PC1 — the power construction company in its strongest position in years. According to VCBS, PC1's power construction backlog reached a record VND 8,250 billion at the end of 2025, with three standout projects.MarketTimes

The 500kV Line Circuit 3 is an urgent national power transmission contract, the Con Dao subsea cable is valued at approximately VND 1,800 billion, and the wind power EPC contract in the Philippines is worth around VND 1,200 billion. Construction revenue is expected to grow 11% in 2026, with estimated new contract value of VND 7,000 billion — of which 57% comes from private clients, demonstrating impressive revenue diversification.

Even more notably, the Bao Lac A wind power project is expected to commence operations by late Q2 or Q3 2026, adding a new revenue stream from power generation. This means PC1 benefits not only from construction but is also beginning to harvest returns from its own renewable energy assets.

REE, GEG, and the New Electricity Pricing Mechanism

Beyond PC1, REE is aggressively expanding its renewable energy portfolio with expectations for a profit breakthrough in 2026-2027. After-tax profit projections for 2026 range from VND 2,600 to 2,948 billion depending on the source — Vietcap, BVSC, VNDirect, and HSC.Elibook GEG is also positioned to benefit from the new investment cycle under Power Planning VIII, as the government targets renewable energy (excluding hydropower) to reach 28-36% by 2030.Fili

A key policy catalyst is providing further support: the two-component electricity pricing mechanism (capacity price + energy price) has been piloted since January 1, 2026, creating a more attractive pricing framework for renewable plants compared to the previous transition period.VnExpress This is a significant step toward market-based electricity pricing, and the renewable energy group is a direct beneficiary.

The Dark Side — Gas-Fired Power Under Heavy Pressure

While renewables are booming, gas-fired power companies are caught between rising fuel costs and selling prices that have not yet adjusted. POW faces the initial operating phase of the Nhon Trach 3 and 4 plants with high borrowing costs. With Brent sustaining elevated levels, gas input costs rise with a certain lag, weighing heavily on gross profit margins. POW's trading volume in its most recent session was significantly below its 20-day average — a sign that capital is actively avoiding the stock.

NT2 is somewhat more stable thanks to long-term gas contracts and nearly fully depreciated assets, allowing net profit in 2026 to grow an estimated 9% to VND 357 billion despite slightly declining revenue.Vietnambiz However, NT2 still faces risk if imported gas prices continue to climb. According to SSI Research, a fluctuation of roughly $10/barrel in Brent can significantly impact POW's gross margin when pricing mechanisms have not kept pace with costs.

The Big Picture — Selective Opportunities Between Two Extremes

The divergence within the power sector creates a clear investment map. Renewable energy companies (REE, GEG) enjoy a dual advantage: unchanged input costs while selling prices rise, combined with support from the new pricing mechanism and Power Planning VIII. Power construction (PC1) is fueled by surging infrastructure investment demand with a record backlog. Conversely, gas-fired power (POW, NT2) depends entirely on oil price developments and pricing adjustment mechanisms — an equation that currently has no favorable solution.

However, it is worth noting that with Brent having surged nearly 58% in just one month, any signal of geopolitical cooling from the Middle East could trigger a sharp oil price correction — and a reversal in power sector capital flows. Investors need to clearly distinguish between the short-term story (the oil price shock) and the long-term outlook (electricity demand growing 8.5%/year, Power Planning VIII) to determine appropriate positioning. The last time oil spiked this dramatically — early 2022 — renewables also surged in the short term before correcting with the broader market. History may not repeat, but it often rhymes.