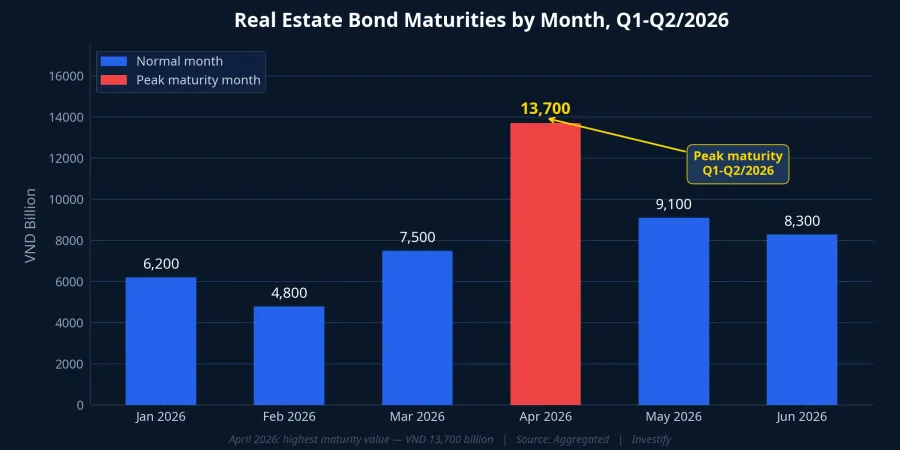

On March 27, over 13 real estate stocks simultaneously hit their ceiling prices — PDR up 6.84%, KBC up 6.97%, DIG up 6.64%. Purple flooded the trading boards as VN-Index surged 28.17 points to 1,672.8.Dan Tri But anyone looking closer would spot what the trading board does not show: in April alone, roughly VND 13,700 billion in real estate corporate bonds will come due — accounting for 80.8% of total market-wide bond maturities, up 37.5% from March and 3.4 times the same period last year.Thoi Bao Ngan Hang

The question the reports do not spell out: can the companies flashing purple on the trading board actually afford to pay their debts?

April 2026 — peak maturity pressure

Total principal and interest obligations in April 2026 are estimated at approximately VND 23,300 billion. The three largest maturities belong to Vingroup (VIC) at roughly VND 4,000 billion, Vinhomes (VHM) at VND 4,000 billion, and TCO Real Estate at VND 3,000 billion. For VIC and VHM — the industry's heavyweights — financial capacity is relatively strong, so default risk remains low. But the real risk lies with smaller developers: weaker cash flows, persistent late-payment histories, and far less room to maneuver.

Looking at the full year, total real estate bond maturities in 2026 reach a record VND 108,267 billion, representing 58.4% of all corporate bonds maturing — a legacy of the aggressive issuance wave during 2021-2022.VnEconomy

The "debt deferral" wave — who is trapped?

Even before April arrives, the situation has been concerning since the start of the year. As of late February 2026, total overdue corporate bonds across the market reached approximately VND 18,700 billion, with 26 bond codes from 12 issuers recording payment defaults.VnBusiness

The most notable case is Novaland (NVL). As of March 16, 2026, the company was behind on approximately VND 1,435 billion in principal and VND 427.6 billion in interest — totaling nearly VND 1,862 billion on bond code NVLH2224006. Subsidiary Nova Final Solution also owed an additional VND 125.9 billion.Vietnam Business Insider More critically, auditors have raised going-concern doubts, and Novaland itself admitted it lacks sufficient funds to repay debts through the end of 2026.VnExpress

Novaland is not alone. R&H Group carries total overdue bonds of VND 5,000 billion, has repeatedly requested interest payment deferrals with unpaid interest nearing VND 276 billion, and has been fined by the State Securities Commission for disclosure violations.Nguoi Dua Tin Additionally, Van Truong Phat (VND 10,000 billion maturing this year), Hai Dang (VND 6,650 billion), and Truong Minh (VND 5,500 billion) are all under severe pressure.Dien Dan Doanh Nghiep

Why are stocks still rising?

The divergence between the equity and bond markets reflects two entirely different logics. Stocks react to expectations — short-term speculative capital flooded into real estate names after VN-Index had dropped 12.3% over the preceding three weeks, creating a "technical rebound" effect. Policy expectations around legal bottleneck resolution and credit easing are also fueling optimism.

But who is really at risk? Notably, foreign investors were net sellers on March 27 — NVL alone saw VND 74.33 billion in net foreign selling. Institutional investors, with their longer-term perspective, are far more cautious than domestic retail investors caught up in the short-term wave.

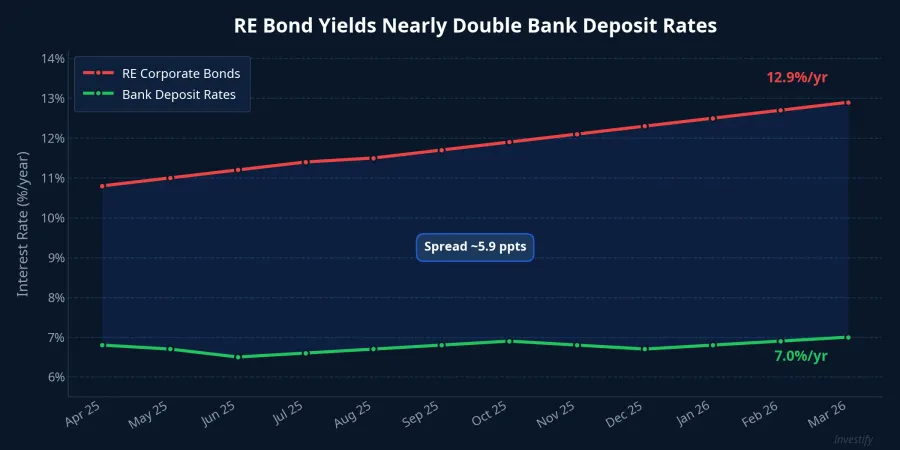

Meanwhile, real estate bond yields have climbed to 12.9% per year — nearly double the banking sector's 7.0%.Vietnam News This spread of nearly 6 percentage points is a clear signal that the market is pricing in significantly elevated default risk for the real estate sector.

Distinguishing risk — not all real estate stocks are equal

Investors must soberly distinguish between two distinct groups. The fundamentally strong names — VIC, VHM, KDH, NLG — have robust cash flows, transparent land banks, and high debt-servicing capacity. Their stock rallies have a more rational foundation. Conversely, the high-risk group — NVL and smaller developers with late-payment histories — faces heavy maturity pressure, weak cash flows, and the danger of "catching a falling knife" for those who fail to do proper due diligence.

The real risk is that many retail investors only see the purple ceiling prices on the board while forgetting to read the balance sheets behind each ticker. The mass ceiling-price rally is a positive sentiment signal, but April 2026 will be the toughest test of the year for the entire real estate sector. Companies that cannot service their bond obligations will be exposed quickly — and when that happens, today's purple could turn into tomorrow's floor red.