Here is what the reports do not make explicit: when a bank has just posted a quarterly loss with bad debts double the regulatory threshold, yet prioritizes a name change and headquarters relocation — retail investors should ask: whose interests are being served here?

Sacombank (STB) is preparing for its Annual General Meeting on April 22, 2026, with three headline proposals: rebranding as "Sai Gon Tai Loc Commercial Joint Stock Bank," relocating from its iconic headquarters on Nam Ky Khoi Nghia Street, and extending its post-merger restructuring plan through 2030 — four years beyond the original deadline. Each proposal deserves scrutiny, but taken together, they raise more questions than answers.

A Decade of Restructuring, and the Wound Still Has Not Healed

The story began in 2015, when Sacombank merged with SouthernBank and inherited a massive portfolio of bad debts. The State Bank of Vietnam (SBV) approved a 10-year restructuring plan. After more than a decade of effort, Sacombank has resolved most of the legacy debts, but the bank itself acknowledges that debt recovery remains challenging due to complex legal proceedings.Vietstock

But who bears the cost of this prolonged process? Retail shareholders — those who have patiently held STB for years, expecting the restructuring to conclude on schedule.

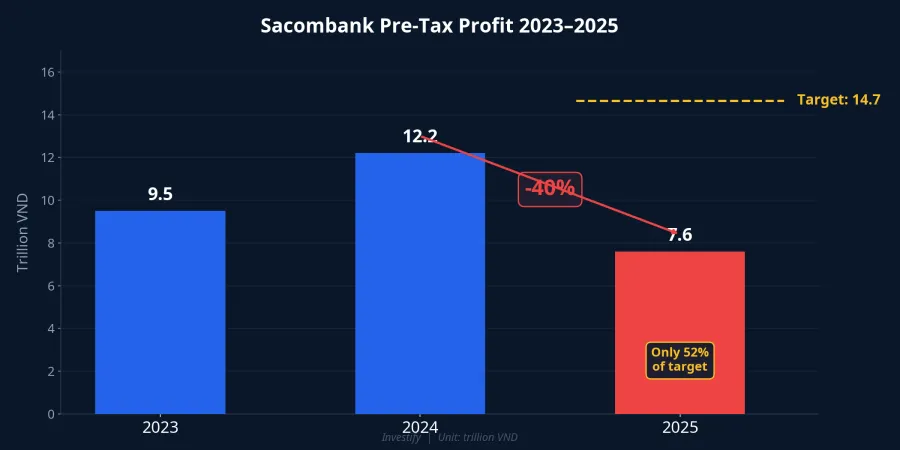

Profit Evaporates 40%, First Quarterly Loss in Nearly a Decade

The 2025 financial results provide the clearest evidence that the wound has not healed. Consolidated pre-tax profit reached only VND 7,628 billion — down approximately 40% year-on-year and achieving just 52% of the VND 14,650 billion target approved by shareholders.CafeF

Most alarming, Q4/2025 marked Sacombank's first quarterly loss in nearly a decade at approximately VND 3,360 billion. The direct cause: the bank aggressively increased credit risk provisioning to VND 9,232 billion in Q4 alone — roughly 8 times the previous quarter.Tuoi Tre While heavy provisioning can be interpreted as "cleaning up" the balance sheet, it also reveals that bad debts had been accumulating and were masked by low provisioning in earlier quarters.

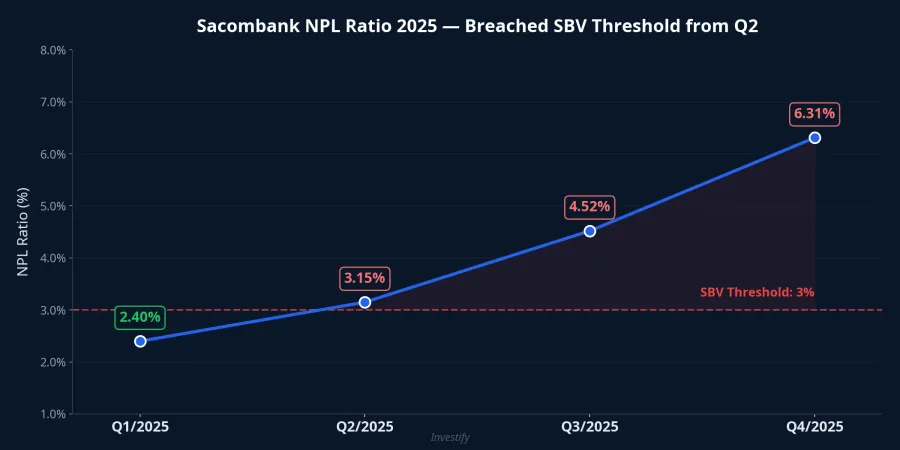

NPL Ratio Surges to 6.3% — Far Beyond the Safety Threshold

The direct consequence of this provisioning wave is that the non-performing loan (NPL) ratio on customer loans surged to 6.31% at end-2025, up from just 2.4% at the start of the year — far exceeding the SBV's 3% control threshold. Loss-category debts (Group 5) increased by VND 18,400 billion to reach VND 29,906 billion.Dan Tri

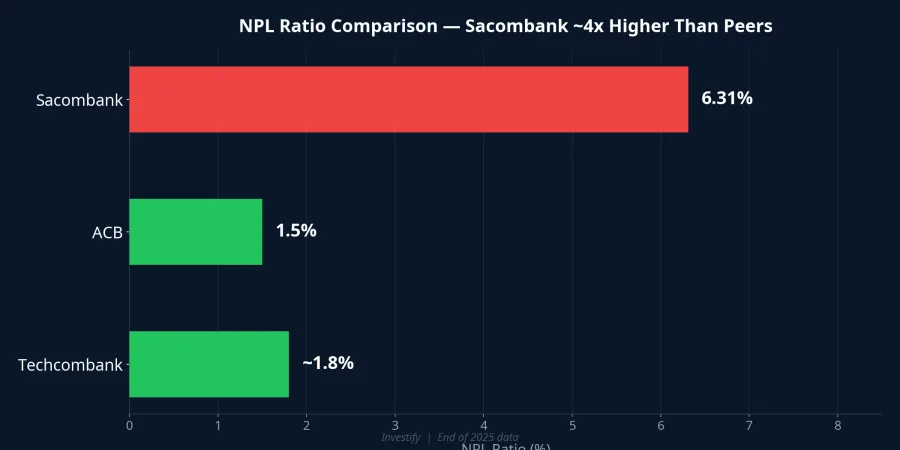

The VND 29,906 billion in Group 5 debts deserves careful consideration: it equals nearly 4 times the bank's entire 2025 profit. In other words, even maintaining current profit levels without additional provisioning, Sacombank would need at least 4 years just to offset these potentially irrecoverable debts. Compared to ACB (NPL around 1.5%) or Techcombank (below 2%), the gap is enormous.

Rebranding and Relocation — What Problem Does It Solve?

Shortly after Nguyen Duc Thuy (known as "Bau Thuy") was appointed CEO in late 2025, Sacombank launched a series of brand identity changes. The bank registered the trademark "Sai Gon Tai Loc Vietnam Bank" on December 29, 2025.Nguoi Lao Dong

The relocation rationale is that the current headquarters is "not within the core zone of Ho Chi Minh City's International Financial Center."Tuoi Tre However, the new location has not been specified in the proposal. Industry observers have noted that Sacombank signage has appeared at Thaigroup's headquarters — ThaiSquare The Merit on Nguyen Thi Minh Khai Street.CafeLand

The real risk is this: brand repositioning can support image, but cannot substitute for resolving nearly VND 30,000 billion in potentially irrecoverable debts sitting on the balance sheet. Additionally, this year's AGM will be held for the first time outside Ho Chi Minh City — in Phu Tho province, the hometown of Nguyen Duc Thuy. This detail has raised questions about accessibility for hundreds of thousands of retail shareholders based in HCMC.

2026 Targets: Cautious to the Point of Concern

Sacombank has set a 2026 pre-tax profit target of just VND 8,100 billion — a 6.2% increase over 2025 results but 45% below the previous year's plan.Vietstock The target of bringing NPLs below 5% confirms that the bank recognizes its current bad debt ratio remains critically high and cannot be quickly resolved.

Given that 2025 achieved only 52% of plan, investors have every right to question whether the VND 8,100 billion target is genuinely achievable or merely another optimistic figure on paper. STB shares currently trade around VND 66,400 per share with P/B and P/E ratios among the highest in the banking sector — reflecting market expectations for a completed restructuring. But with the plan now seeking a 4-year extension, this premium is under serious challenge.

Three Questions STB Shareholders Must Ask Before the AGM

Before the April 22 AGM, every STB shareholder should consider three critical questions. First, does extending restructuring to 2030 mean four more years of elevated bad debts and restricted dividends? The aggressive provisioning in 2025 may be a positive long-term signal, but it also shows the post-SouthernBank merger problem remains unresolved.

Second, is rebranding and relocating the right priority at this moment? When NPLs are double the threshold and profits have dropped sharply, should management resources focus on debt resolution or brand identity?

Third, is the VND 8,100 billion profit target realistic? The new leadership under Nguyen Duc Thuy needs to prove operational capability through concrete results, not just a new name.

A fresh coat of paint has never been enough to cure an old disease. And for STB, that disease remains clearly visible on the balance sheet.