The big picture reveals a significant shift in the final week of March 2026. After three weeks of decline that wiped out 232.5 points (equivalent to 12.3%), the VN-Index found its footing at 1,672.8 points — up 25 points (+1.52%). What makes this recovery more interesting than the headline number is the story behind it: who is buying, who is selling, and where global capital flows are heading.

The March 27 Session — A Breadth Signal Worth Watching

On Thursday March 27, the VN-Index surged 28.2 points (+1.7%) with 253 advancing stocks versus only 90 declining — an overwhelmingly positive breadth ratio rarely seen during a market that just endured a deep correction.VnDirect Leading sectors included Chemicals (+3.4%), Retail & Services (+2.8%), Oil & Gas (+2.4%), Technology (+2.2%), and Real Estate (+2.2%).

The broad-based market breadth indicates this was not a recovery driven by a handful of blue-chips, but rather a widespread capital diffusion — a sign of a more fundamentally grounded rebound compared to a mere technical bounce.

Foreign Investors Still Net Selling — But Pressure Is Cooling Significantly

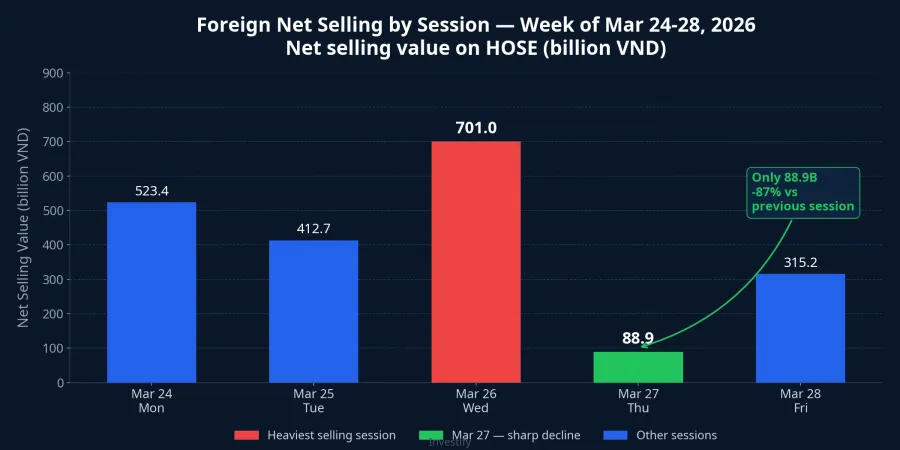

Capital flows are shifting, though not yet from foreign investors. During the week, foreign investors net sold approximately 2,982 billion VND on HOSE.VietnamBiz However, the deceleration in net selling is the most noteworthy development.

On March 27, foreign net selling dropped to just 88.9 billion VND — an 87% decline from the 701 billion VND the previous session and the lowest level in seven consecutive sessions. Notably, the bulk of the week's net selling was concentrated in FUEVFVND (Diamond ETF certificate) at -3,594 billion VND, followed by STB (-810B), HDB (-611B), VCB (-592B), and VIC (-560B). On the buy side, MCH (Masan Consumer) stood out with +1,031 billion VND in net purchases.

The fact that FUEVFVND accounted for most of the net selling reveals that the pressure is primarily driven by ETF redemptions — a technical phenomenon that does not reflect a negative assessment of Vietnam's market fundamentals. Excluding the ETF factor, the actual foreign capital picture is far less gloomy than the aggregate net selling figure suggests.

DXY Breaks Below 100 — The Catalyst for Capital Flow Reversal?

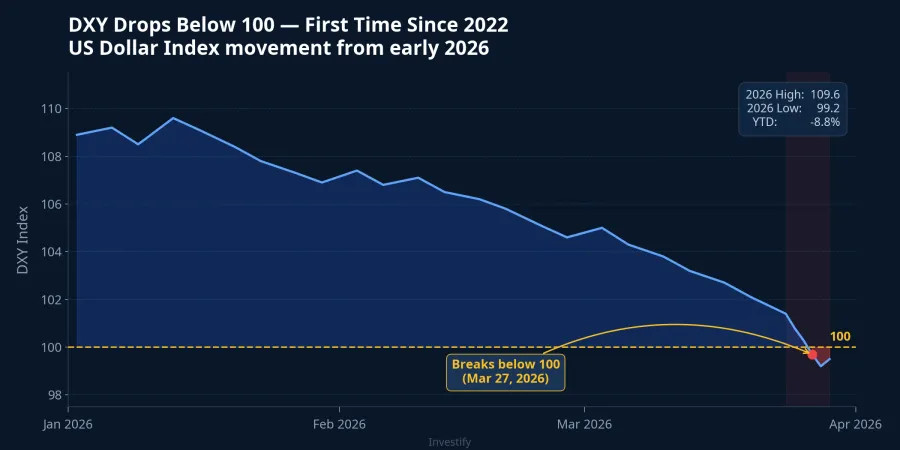

The most significant macro development of the week was the DXY (US Dollar Index) falling to the 99.58-99.96 range, breaking below the psychological threshold of 100 for the first time since 2022.Vietnam.vn The USD/VND exchange rate consequently dropped to 26,337 VND on March 27.

History shows that when the DXY weakens, international capital tends to shift from USD-denominated assets toward emerging markets. The MSCI Emerging Markets Index has gained 15% since the start of 2026, with funds increasing long positions across Asia. Vietnam — with its P/E ratio sitting at attractive levels following the 12.3% correction — could well become a prime destination for foreign capital if the weak-USD trend persists.

However, it should be noted that the DXY recovered to 100.15 on March 29. The trend is not yet fully established, and investors should closely monitor developments in the coming week before making outsized bets on a foreign capital return scenario.

Domestic Capital Takes the Lead — Corporate Insiders "Buy the Dip"

While foreign investors remain cautious, domestic capital has stepped up decisively. Executives and family members at 13 major corporations — including Hoa Phat, Masan, Nam Long, Phat Dat, and Vietjet — registered to purchase over 3,000 billion VND in shares during the market downturn. This is a powerful signal: the "insiders" — those who understand their companies' actual business conditions best — have concluded that current prices are attractive enough to deploy capital.

In the same direction, proprietary trading desks at securities firms recorded nearly 700 billion VND in net purchases during Friday's session, reflecting consensus from domestic "smart money."VietnamBiz When both insiders and proprietary desks buy simultaneously, it typically signals that a short-term bottom has formed.

Outlook for March 30 - April 3: Narrow Range, Mild Recovery

Compiled forecasts from securities firms point to a base-case scenario of narrow-range consolidation with a mild upward bias next week. ASEAN Securities notes the VN-Index has recovered after three consecutive weeks of decline, with capital concentrating in Insurance, Retail, and Chemicals sectors.ASEAN Securities Mirae Asset views current valuations as sufficiently attractive with support at 1,600 points, while BSC expects the index to oscillate around the MA200 (1,656 points). Vietcap believes foreign net selling will likely decelerate if exchange rates stabilize.

From a technical perspective, the VN-Index is holding above its MA200, with RSI14 at 43 — out of oversold territory but not yet strong. Key support lies at 1,600-1,650 points, with the nearest resistance at 1,700-1,720 points.

Balancing Opportunity Against Risk

The big picture this week is distinctly two-sided. On the positive front, foreign net selling pressure is declining sharply (especially excluding ETFs), the DXY below 100 creates a favorable environment for emerging markets, and insider buying signals confidence from within. On the risk side, Brent crude remains elevated above $95 per barrel putting pressure on inflation, Vietnam's Big 4 banks have just raised interest rates increasing corporate borrowing costs, and the DXY could still recover above 100.

The prudent strategy for this phase: short-term investors can capitalize on the consolidation period to increase exposure in sectors showing positive technical signals (Chemicals, Retail, Insurance), while medium-to-long-term investors should maintain positions and closely monitor foreign capital flows — because when foreign investors genuinely reverse to net buying, that will be the strongest catalyst for the next leg up.