Reading the Numbers: Where Does Coteccons Stand?

While most investors remain focused on banking and real estate, Vietnam's infrastructure construction sector is experiencing its most impressive growth phase in nearly a decade. Coteccons (CTD) — Vietnam's largest general construction contractor — is the most compelling case study right now.

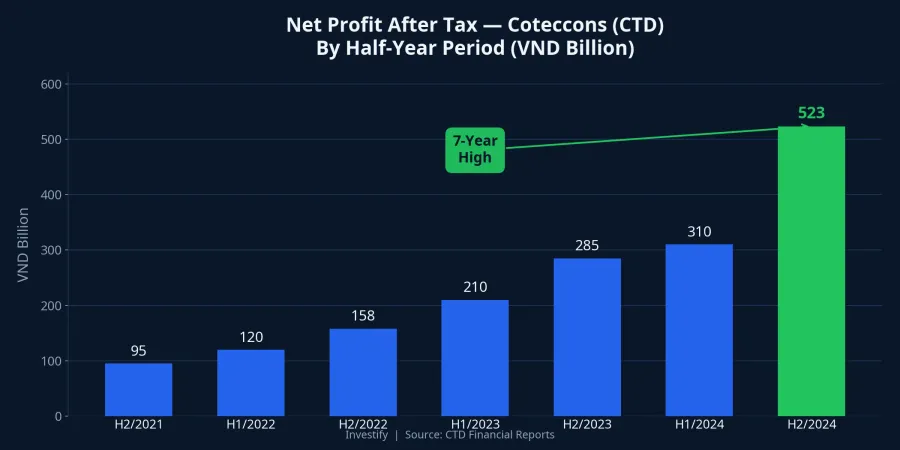

In the first half of fiscal year 2025-2026 (July to December 2025), Coteccons reported consolidated revenue of VND 17,459 billion, up 50% year-over-year.Vietstock Net profit after tax reached VND 523 billion, surging 165% — the highest level in nearly 7 years.VnExpress In Q2 alone, quarterly revenue surpassed VND 10,000 billion for the first time ever, signaling that execution capacity has reached unprecedented levels.

What stands out in the financial statements is the pace of target completion: after just 6 months, Coteccons has already achieved 58% of its full-year revenue plan and 75% of its profit target. The full fiscal year targets are VND 30,000 billion in revenue and VND 700 billion in net profit — if this momentum holds, exceeding targets is entirely feasible.

Record Backlog of VND 62.5 Trillion — Secured Revenue for 2 Years

The most important highlight is not past profits, but the backlog value. At the end of Q2 FY 2025-2026, the backlog reached VND 62,500 billion — an all-time record, equivalent to over 2 years of current revenue.VietnamBiz In Q2 alone, newly signed contracts totaled VND 18,000 billion — a figure showing that the project pipeline continues flowing in at a rapid pace.

The backlog sources are well diversified: Long Thanh airport infrastructure (the CTD-CC1-FECON consortium won a package worth over VND 3,143 billion), major civil projects like Eaton Park (Gamuda Land), Ecopark Central Park Vinh, and Sun Group's industrial complex in Phu Quoc. This diversification reduces concentration risk in any single segment.

Vietnam's Largest Public Investment Cycle Provides Tailwinds

Coteccons is not an isolated case — the entire sector is benefiting from a record public investment cycle. The 2026 public investment capital plan exceeds VND 1 quadrillion, up approximately VND 93,000 billion from 2025.Government Portal Two mega-projects are reshaping the construction sector landscape.

Long Thanh Airport, with a total investment of VND 336,630 billion, is approximately 67% complete and targets commercial operations in the first half of 2026 with nearly 15,000 engineers and workers mobilized.Nhan Dan Additionally, on March 28, 2026, the Lien Chieu super-port project (Da Nang) officially launched its container terminal worth over USD 2 billion, planned across 3 phases through 2036, with the Hateco-APM Terminals (Netherlands) consortium as the investor.Government Portal

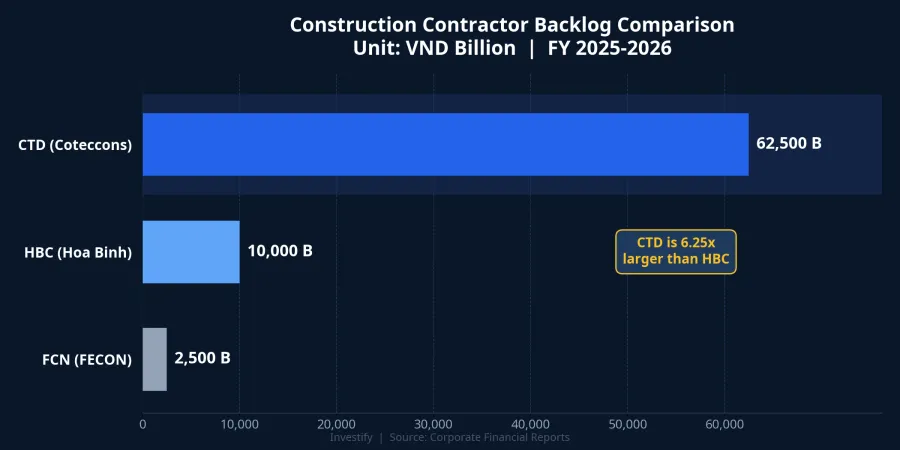

Contractor Comparison: CTD Leads by a Wide Margin

Comparing the three major listed contractors, Coteccons' lead is decisive. CTD's backlog is 6.25 times that of Hoa Binh (HBC) and 25 times that of FECON (FCN). For 2026 revenue targets, CTD aims for VND 30,000 billion versus HBC's VND 10,000 billion. CTD's gross margin is improving to 4.3%, while HBC continues to face significant volatility due to heavy interest expense burdens.CafeBiz

FCN (FECON), while much smaller in scale, has a distinct advantage in the technical foundation segment — with above-average gross margins on airport and industrial projects. It is a stock worth watching for investors seeking high-beta exposure in the infrastructure space.

Risks to Monitor Closely

Coteccons' gross margin has improved from around 3% (2021-2022) to 4.32% in the most recent quarter, thanks to stable steel prices from the 2022 peak and new material pricing mechanisms in contracts. However, investors should not let optimism overshadow real risks.

First, public investment disbursement remains the biggest bottleneck. Despite the plan exceeding VND 1 quadrillion, the disbursement rate in the first 2 months of 2026 was only 5.6% of the plan.TBTCVN If disbursement lags, even a massive backlog will struggle to convert into revenue on schedule. Second, Brent crude above USD 95 per barrel is pushing up transportation and material costs, directly squeezing already thin margins. Third, multiple large projects running simultaneously require substantial working capital, while payments from government projects tend to be delayed. Finally, Vietnam's construction sector margins hover at just 3-5%, with competitive bidding limiting room for meaningful improvement.

Investment Perspective

CTD shares are trading around VND 81,400, with target prices from securities firms ranging between VND 83,000 and VND 110,000. The key question for investors: can the conversion of VND 62,500 billion in backlog into actual revenue and profits keep pace with market expectations?

With Long Thanh Airport nearing commercial launch and Lien Chieu port just breaking ground, infrastructure construction stocks deserve a place on watchlists — especially for investors seeking growth stories beyond real estate and banking. The numbers do not lie, but the market always prices based on future expectations.