This policy opens a major opportunity for Vietnam's maritime industry — but opportunity always comes with questions: who has the capacity to seize it, and at what cost?

As the government accelerates its maritime economic strategy and upgrades the national port system, Vietnam Maritime Corporation (VIMC, ticker MVN) has officially been tasked with developing the Can Gio International Transshipment Port — a project with total investment of VND 113,500 billion (approximately $4.8 billion). This is not only the largest infrastructure project in VIMC's history, but also a litmus test for Vietnam's state-owned enterprise restructuring story.

From the Vinalines "Black Hole" to a Billion-Dollar Market Cap

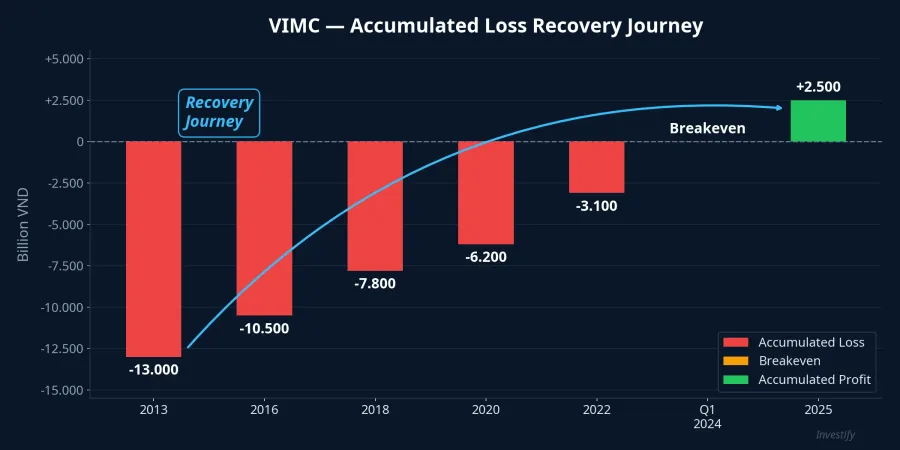

VIMC has come a remarkably long way on its restructuring journey. Looking back to 2013, Vinalines was the poster child of state-owned enterprise failure, with accumulated losses peaking at negative VND 13,000 billion, accompanied by a string of financial and management scandals.

But after more than a decade of persistent restructuring, the picture has completely changed. Accumulated losses were fully cleared by the end of Q1/2024, with retained earnings reaching over VND 1,148 billion by the end of Q3/2025.VietnamFinance Market capitalization once hit a record of over VND 105,000 billion (approximately $4 billion), and currently hovers around $3.3 billion with the share price at VND 49,500.

Strong 2025 Performance and Ambitious 2026 Targets

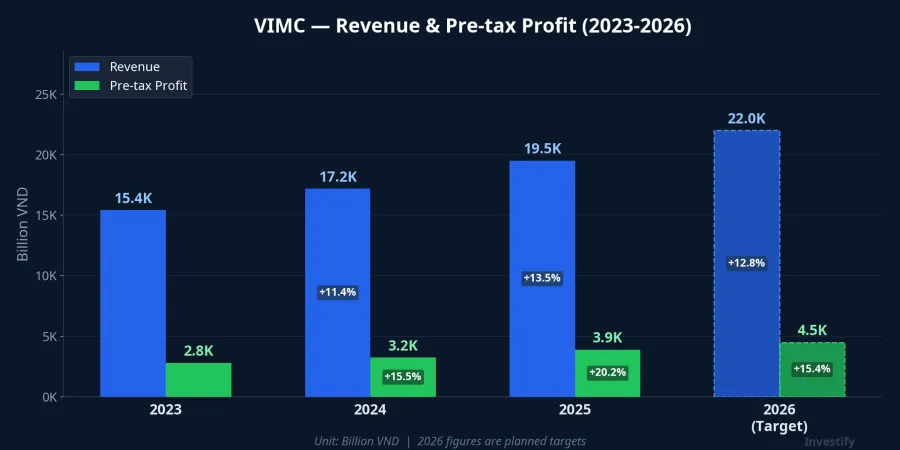

2025 was an impressive year for VIMC. Consolidated revenue reached VND 20,475 billion, with pre-tax profit at VND 3,079 billion. The port segment was the highlight: cargo throughput hit 161.9 million tons (up 12%), while container volume reached 7.5 million TEUs (up 21%). Shipping also exceeded targets at 21.5 million tons.DNSE

The 2026 targets remain ambitious: consolidated revenue of VND 22,186 billion, pre-tax profit of VND 3,236 billion, shipping volume of 23.7 million tons, and port throughput of 180.1 million tons.VietnamNet

Can Gio Super Port — The Biggest Strategic Bet in History

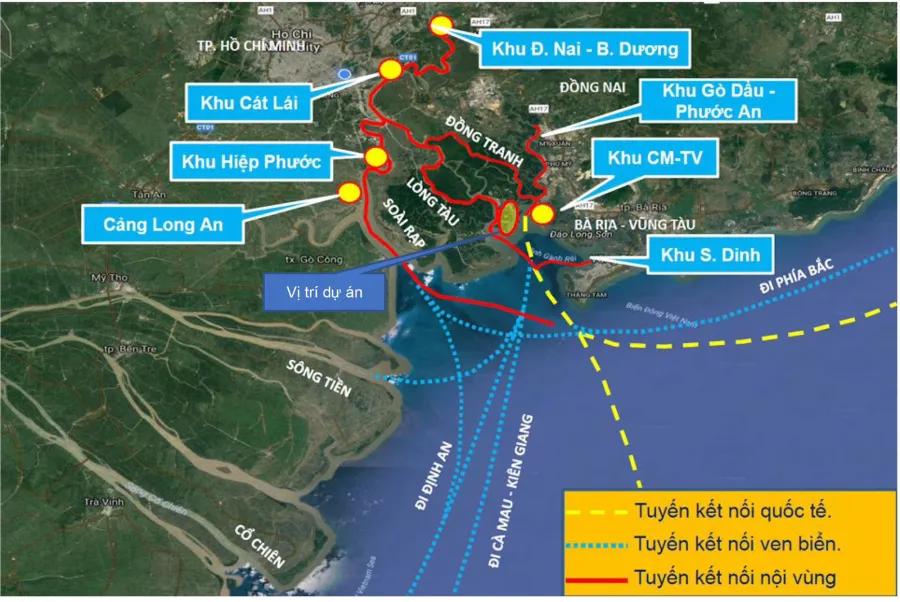

The Can Gio International Transshipment Port is a watershed strategic move. With total investment of VND 113,500 billion and a design capacity of 16.9 million TEUs per year, it rivals the region's top transshipment hubs.CafeF

The joint venture structure is the key factor determining feasibility:

- Terminal Investment Limited (TiL) — a subsidiary of MSC (the world's largest shipping line): 49%

- VIMC: 36%

- Saigon Port Corporation: 15%

VIMC plans to contribute VND 13,839 billion in two phases: over VND 4,100 billion during 2026-2030 and nearly VND 9,700 billion during 2031-2045.Vietstock

The involvement of MSC — the world's number one container shipping line — ensures a stable source of transshipment cargo, solving a challenge that many ports in the region have failed to overcome.

Capital Expansion to VND 30,000 Billion — Opportunity and Dilution Risk

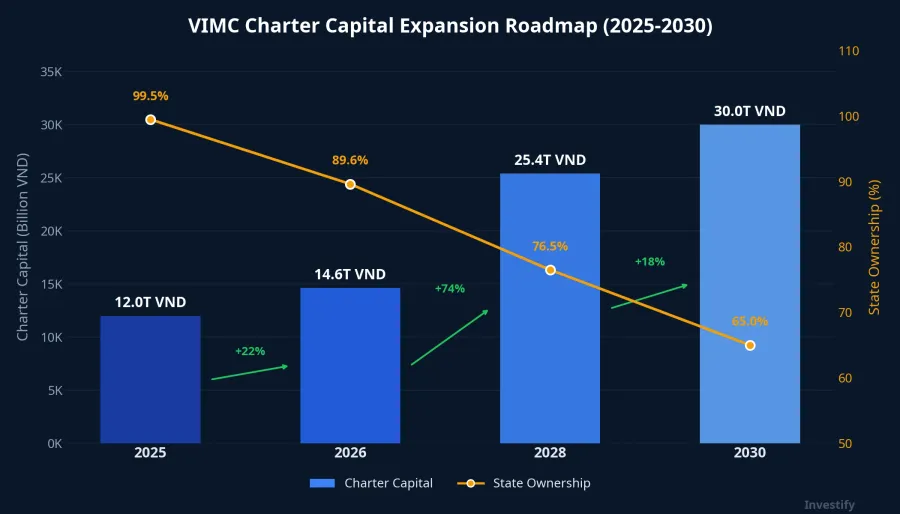

Alongside the super port, VIMC is implementing a charter capital expansion from over VND 12,000 billion to VND 30,000 billion, while reducing state ownership from 99.47% to 65% under Resolution 79.CafeBiz

The three-phase roadmap:

- 2026: Issue 145 million shares, raising capital to VND 14,638 billion, state ownership down to 89.6%.

- 2027-2028: Issue 250 million shares to strategic investors, capital above VND 25,400 billion, state ownership at 76.5%.

- 2028-2030: Reach VND 30,000 billion in charter capital, state ownership at 65%.

Over the next 3-5 years, this opens an opportunity to invest in a nationally strategic infrastructure enterprise. However, issuing nearly 400 million new shares over 4-5 years creates significant dilution risk — investors need to closely monitor the issuance price and criteria for selecting strategic partners.

Risks to Consider

Intense regional competition: Can Gio port will compete directly with Singapore and Tanjung Pelepas (Malaysia) — transshipment hubs that have operated reliably for decades. Building a new shipping route network requires years of persistence.

Timeline and capital requirements: The project runs through 2045 with massive capital needs. Any delays in land clearance or connecting infrastructure (roads, railways) would directly impact investment returns.

Low liquidity: Currently trading on UPCOM with an average of only 15,000 shares per day. The plan to transfer to HoSE has no specific timeline yet — a major barrier for institutional investors looking to participate.

What Should Investors Ask at the 2026 AGM?

The 2026 annual general meeting season is approaching. Given VIMC's development roadmap, investors should ask three critical questions:

- Capital sources: What is the specific funding plan for the VND 4,100 billion contribution during 2026-2030 — debt or equity issuance?

- Strategic partners: What are the criteria for selecting strategic investors, and what is the expected issuance price?

- HoSE transfer: What is the concrete listing plan — timeline and conditions?

From Vinalines as a symbol of failure, VIMC has proven its remarkable capacity for recovery. But the biggest question is not about the past — it is about the future: is the $5 billion super port a sound strategic move aligned with the national development roadmap, or an outsized gamble for a company that has only recently escaped losses?