This policy opens a new chapter in how share transactions are taxed — and not everyone is ready for the change.

The Ministry of Finance has just released a draft decree guiding the Personal Income Tax Law with a notable proposal: a 20% tax on profits from transferring shares of unlisted companies.Nhà Đầu Tư If approved, this would be the most significant change to securities transfer taxation in over a decade.

Current Tax Regime vs. the New Proposal

Currently, all share transfers — including unlisted companies — are taxed at 0.1% of the transfer price, regardless of whether the investor made a profit or loss. The new draft separates transactions into two distinct groups:

- Listed/registered securities: the 0.1% rate on transfer price remains unchanged.

- Unlisted shares: switches to 20% on actual profit (sale price minus purchase price and reasonable expenses). If cost basis cannot be determined — a 2% flat rate on transfer price applies instead.

According to the drafting agency, unlisted share transactions are private bilateral agreements, essentially similar to capital contribution transfers — hence requiring a separate tax mechanism.Báo Chính phủ

Notably, the Ministry previously proposed applying 20% to listed securities as well, but withdrew that proposal due to concerns about market liquidity impact.VnEconomy The proposal for unlisted shares, however, remains intact.

How Large Is the Tax Difference?

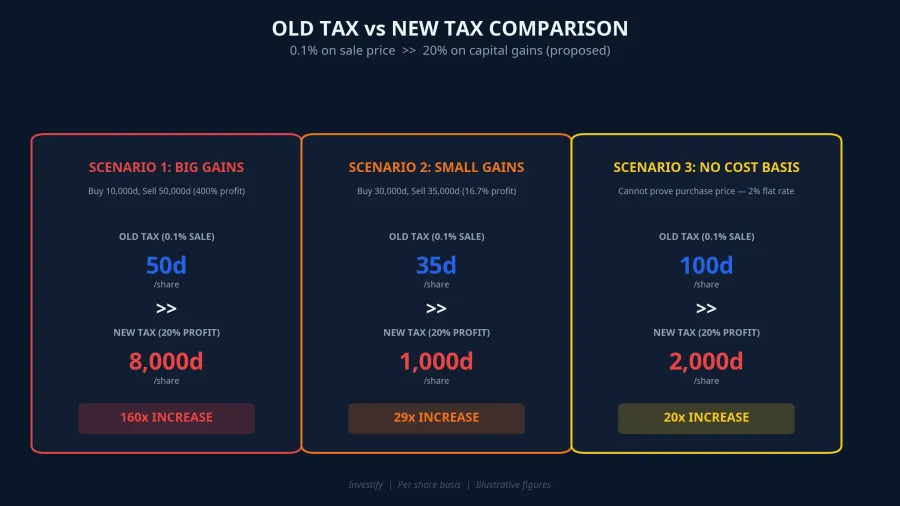

Over the next 3-5 years, if this policy takes effect, the profit equation for OTC investors will fundamentally change. The three scenarios below show that the tax difference can reach up to 160 times in high-profit cases.

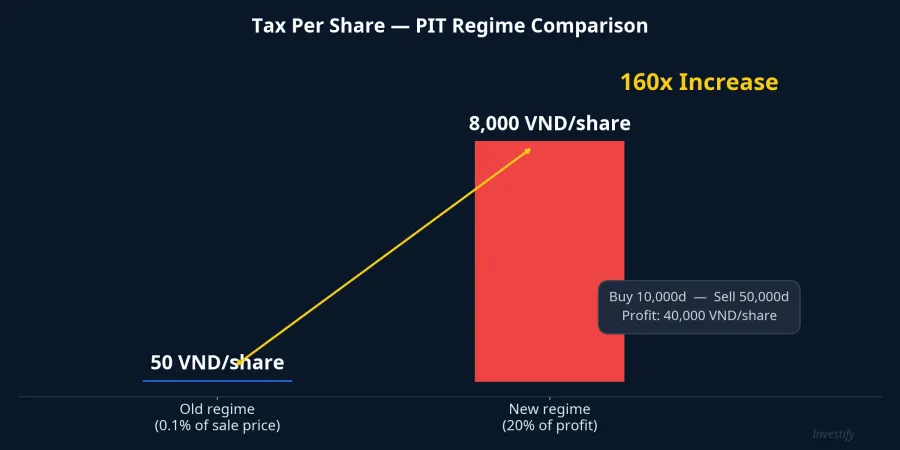

Scenario 1 — Large Gains (Pre-IPO Purchase, Sold After Strong Appreciation)

An investor buys shares at 10,000 VND and sells at 50,000 VND. Under the current system, tax is just 50 VND per share. Under the new proposal, tax jumps to 8,000 VND per share — a 160x increase.

Scenario 2 — Small Gains

Buy at 30,000 VND, sell at 35,000 VND: tax rises from 35 VND to 1,000 VND — a 29x increase.

Scenario 3 — No Provable Cost Basis

If the investor cannot provide documentation proving the purchase price, a 2% flat rate on the total sale price applies. Selling at 100,000 VND means 2,000 VND in tax instead of 100 VND — a 20x increase.

Who Is Most Affected?

With over 900,000 active enterprises in Vietnam but only about 1,600 tickers listed on HOSE, HNX, and UPCoM, the vast majority of share transactions occur off-exchange. Three groups face the most direct impact:

- OTC investors: those trading shares through private agreements — from unlisted bank shares to small and medium enterprises.

- Pre-IPO investors: those who bought in early at low prices, earning returns of hundreds of percent — the new profit-based tax scales exponentially with gains.

- Internal shareholders: ESOP recipients or capital contributors from years past who struggle to document their cost basis — likely facing the 2% flat rate instead.

The Upside — Incentivizing Transparency and Listing

The tax gap between listed (0.1%) and unlisted (20%) shares creates a clear financial incentive for companies to pursue listing. The requirement to prove cost basis also forces parties to maintain transparent transaction records, reducing under-the-table dealings.

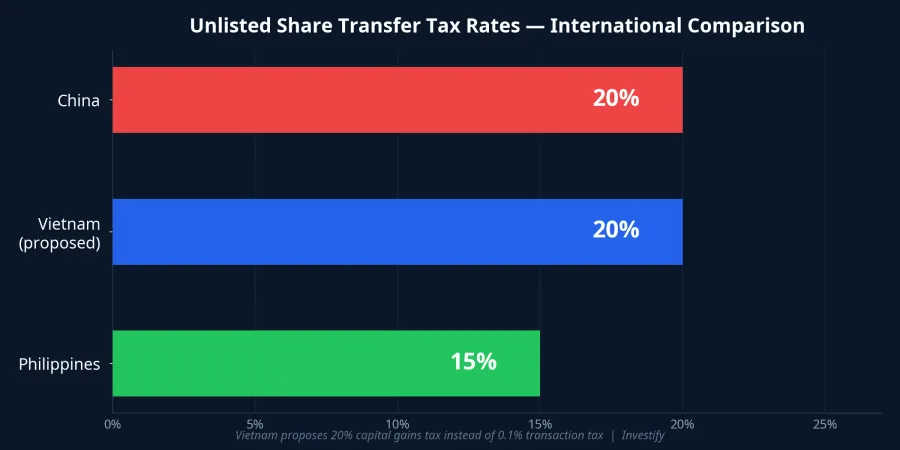

This proposal also aligns with international practice — China and the Philippines have long applied similar taxes on unlisted share transfers.

However, experts note that taxation is only a supplementary factor — governance costs, company scale, and capital-raising needs remain the primary barriers to listing decisions.VnEconomy

Hidden Risks and What Investors Should Prepare

A risk many overlook: without proper purchase agreements or capital contribution documentation, investors face the 2% tax on the entire transfer price — regardless of actual profit or loss. For high-value transactions, the resulting tax bill can be substantial.

OTC market liquidity may also decline in the short term as sellers become more cautious and buyers demand price adjustments to offset the new tax costs.

Investors should take these steps now:

- Audit your records immediately — gather all documentation proving cost basis for every unlisted share investment.

- Recalculate your profit model — factor the new tax costs into valuations when negotiating OTC deals.

- Monitor the policy timeline — the draft is in the public comment phase, and the official implementation date may shift.

Though still a draft, the signal is clear: the era of near-zero tax costs on OTC share transactions is drawing to a close. Investors who prepare proactively will have the advantage when the policy officially takes effect.