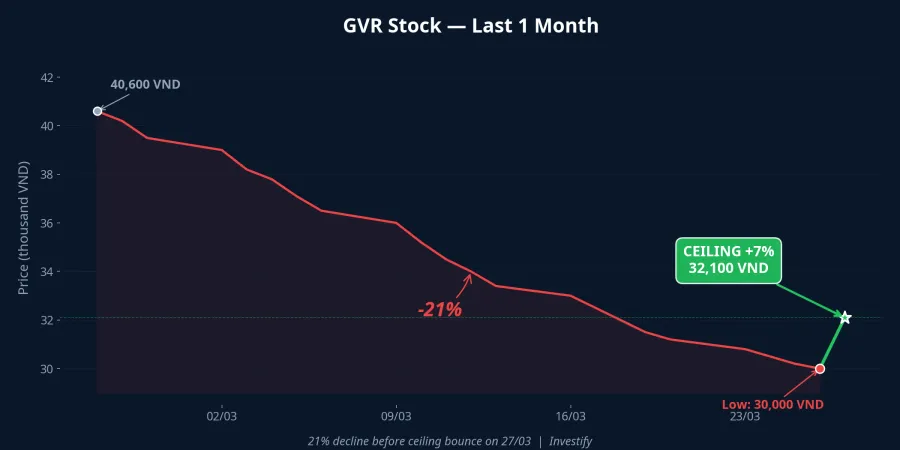

On March 27, 2026, GVR stock hit the 7% ceiling price at VND 32,100. Trading volume exploded to nearly 4.5 million shares, with over 2.3 million shares queued at ceiling price — sellers virtually "vanished."CafeF

But what the trading board doesn't tell you: this ceiling bounce happened right as the Government Inspectorate published findings detailing violations worth thousands of billions of dong. Bottom-fishing capital may have the timing right — but who takes the hit if these structural risks materialize?

Global Rubber Prices Breaking Records — Short-term Story or Long-term Trend?

The immediate catalyst behind GVR's ceiling surge was global rubber prices. On the TOCOM exchange, the April 2026 rubber contract rose 3.59% on March 27 to 361 yen/kg. Natural rubber prices peaked at 204.8 US cents/kg in early March.Doanh nghiệp Hội nhập

WTI crude oil surpassed $95/barrel, touching $100.85 on March 27 — when oil rises, synthetic rubber production costs increase, driving demand toward natural rubber. Sensitivity analysis shows a 10% rubber price increase could boost GVR revenue by approximately VND 1,470 billion and improve EBITDA by VND 430 billion.

The real risk lies here: the 12-month correlation between rubber and crude oil is only -0.03. Rubber follows its own supply-demand dynamics, not oil prices. And prices have already retreated from the 204.8 peak to 197.8 cents/kg by late March — a sign that momentum is fading.

Record 2025 Profits — But That's the Past

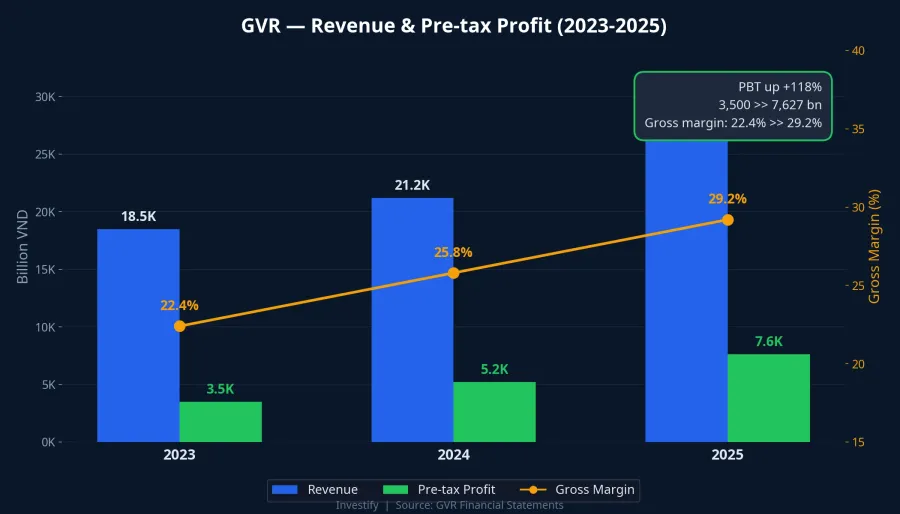

In 2025, GVR posted its best-ever results: pre-tax profit reached VND 7,627 billion, up 36% year-over-year.Tin nhanh CK Net revenue hit VND 28,939 billion, with gross margin improving from 22.4% (2023) to 29.2%. Total assets at year-end reached VND 86,514 billion.Doanh nghiệp Hội nhập

The original target was only VND 5,840 billion — GVR exceeded its plan by 52%. Impressive numbers, but this creates a high comparison base for 2026. If rubber prices can't hold near their peaks, earnings will face significant deceleration pressure.

Three Risks That Bottom-Fishing Capital May Be Ignoring

1. Government Inspectorate Findings — Violations Worth Thousands of Billions

The Government Inspectorate issued Notice No. 475 on its inspection of capital and state asset management at GVR.Bao Chinh phu What the stock tickers don't show:

- Irregular capital advances: The parent company advanced capital to 17 subsidiaries totaling over VND 2,304 billion — without written agreements as required by law.Dan Viet

- Land encroachment: 1,634 hectares of land encroached upon or disputed, with 585.63 hectares already ordered for recovery but not yet returned.

- Outstanding tax liabilities: The Inspectorate demanded review of approximately VND 894 billion in outstanding land lease payments, plus VND 13.4 billion in additional corporate income tax.

- Inefficient investments: Multiple subsidiaries operating at sustained losses, posing risk of state capital erosion.The Leader

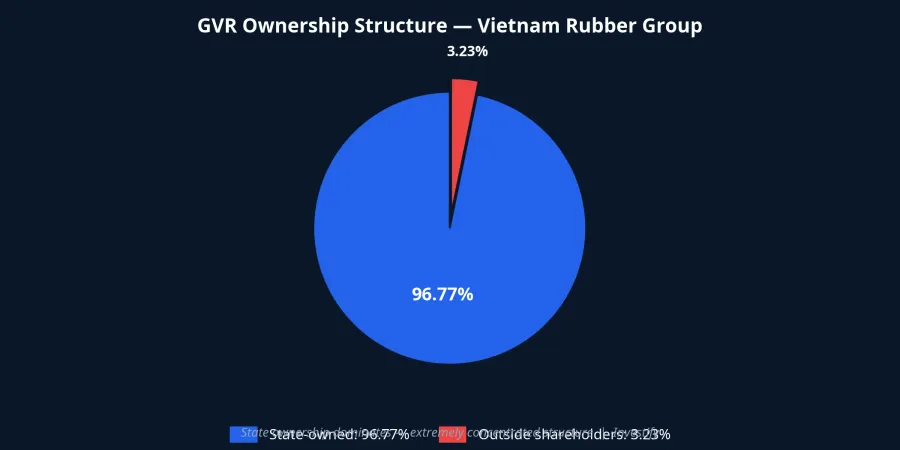

2. Risk of Losing Public Company Status

Under the amended Securities Law, public companies must maintain at least 10% freely tradable shares. Currently, the State holds 96.77% of GVR's VND 40,000 billion charter capital.Nguoi Quan sat Only 3.23% belongs to outside shareholders.

To comply, the State needs to divest at least 6.77% — approximately 271 million shares. Without a clear divestment roadmap, GVR faces the risk of losing its public company status and being delisted, similar to what is happening with BSR, PV GAS, and ACV.CafeF

3. Rubber Price Reversal Risk

If US-Iran tensions ease and oil prices reverse course, commodity market sentiment will shift rapidly. Rubber has already retreated from 204.8 to 197.8 cents/kg — a small gap, but enough to signal waning momentum.

What Should Investors Do?

GVR stands at the crossroads of two opposing narratives: on one side, record profits, peak rubber prices, and the potential of its industrial park segment with over 400,000 hectares of land; on the other, damning inspection findings, delisting risk, and a commodity cycle that may be turning.

Three factors to watch closely: progress on addressing the inspection findings, the State's divestment roadmap, and global rubber price trends. Bottom-fishing capital may be right in the short term — but ignoring these structural risks could easily turn "catching the bottom" into "catching a falling knife."