The big picture looks alarming

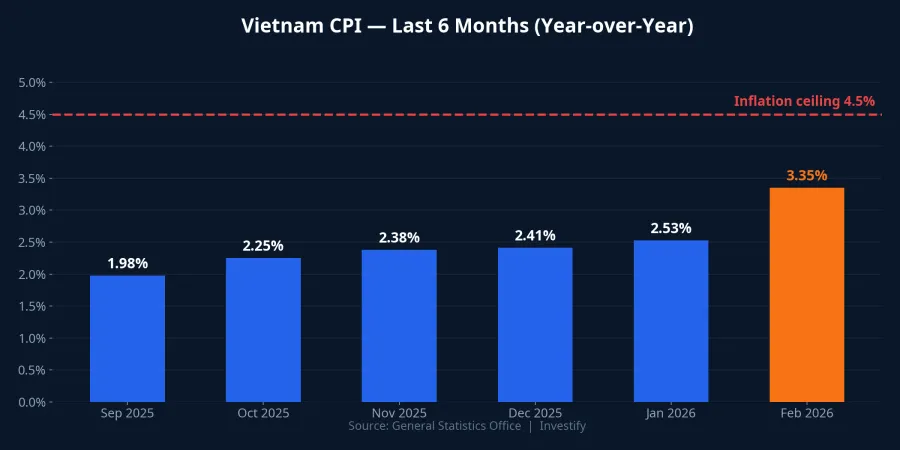

Capital flows are shifting — and not in the direction anyone hoped. Within just four weeks, three major macro events struck almost simultaneously: February CPI jumped to 3.35% year-over-year (up from 2.53% in January)Thanh Nien, Brent crude surged from below $75/barrel to nearly $115/barrel, and Vietnam's Big 4 banks simultaneously pushed deposit rates to their highest levels in over a year.

Each piece alone was concerning. But together, they paint the picture that international analysts describe with a dreaded term: stagflation — inflation running hot while economic growth slows down.

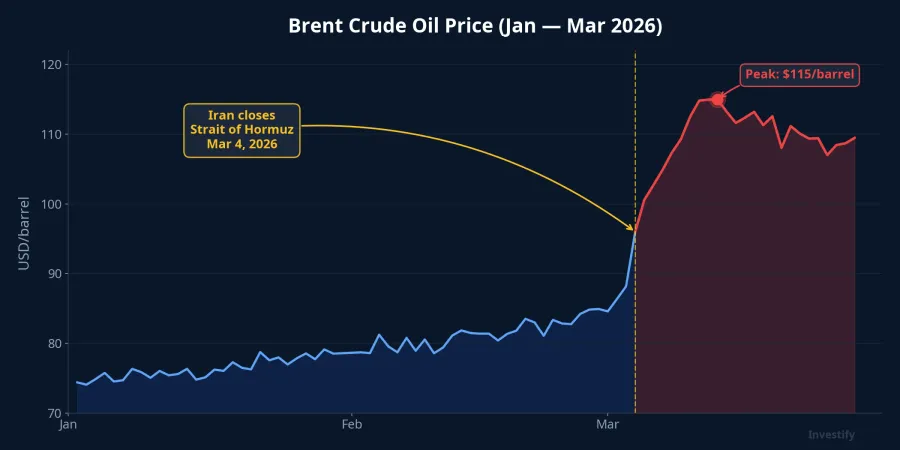

The Strait of Hormuz — a detonator from the Middle East

The direct catalyst pushing oil to its highest level since July 2024 was Iran's decision to close the Strait of Hormuz on March 4, 2026 to vessels from US and Israeli allied nationsSputnik. This strait carries approximately 20% of global crude oil shipments.

The result: Brent crude averaged about $97/barrel in March, a 33% increase from February. On March 9, Brent briefly spiked to $114.36/barrel — the largest single-day jump since 1988Bao Moi.

Goldman Sachs raised its 2026 average Brent forecast from $77 to $85/barrel, warning that in a prolonged high-risk scenario of 10 weeks, prices could reach $135/barrelCafeF.

Vietnam — an economy vulnerable to oil shocks

What makes Vietnam particularly sensitive is its heavy dependence on Middle Eastern supply. In the first 11 months of 2025, Vietnam imported approximately 12.3 million tons of crude oil, with Kuwait alone supplying 9.9 million tons — over 80% of total imports. The two refineries, Nghi Son and Binh Son, meet 70-80% of domestic fuel demand but rely entirely on imported crude.

According to analytical models, every $10/barrel increase in oil prices adds 0.25-0.55 percentage points to Vietnam's CPI, while dragging GDP down by 0.15-0.35 percentage points. With a nearly $40/barrel surge since early March, the inflationary impact could reach 1-2 percentage points — directly threatening the 4.5% inflation ceiling approved by the National AssemblyVietnamPlus.

The State Bank of Vietnam — caught in a classic dilemma

The big picture reveals monetary policy trapped in a textbook bind. On one hand, rapidly rising inflation demands tightening. On the other, the National Assembly has set a minimum GDP growth target of 10% for 2026The Investor — an ambitious figure that requires cheap credit.

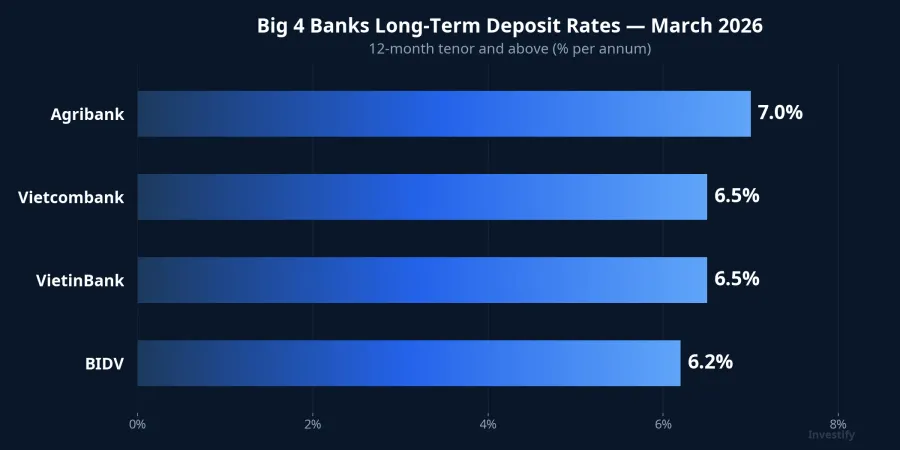

In practice, the Big 4 banks have already raised deposit rates in unison during MarchVietnam.vn. Vietcombank and VietinBank pushed long-term rates to 6.5% per annum, while Agribank surged by 0.7 percentage points to 7.0% per annum for long tenors. In total, 18 banks raised deposit rates in March alone.

Rising funding costs mean lending rates will soon follow, putting pressure on businesses and the real estate market. The State Bank has lowered the credit growth ceiling to around 15% for 2026, prioritizing macro stability. But if inflation continues climbing, it may be forced to raise policy rates — a move that would severely strain the growth target.

Winners and losers in a stagflation scenario

In a stagflation environment, sector divergence becomes stark:

Winners:

- Oil & gas — BSR, GAS, PVS, PVD, PLX benefit directly from rising oil prices. On March 27, PLX gained 5.89%.

- Commodity exports — Agricultural products and raw materials benefit from rising global commodity prices.

- Defensive sectors — Food, utilities, healthcare — demand remains stable regardless of economic cycles.

Losers:

- Real estate — Hit by the double blow of rising rates and credit tightening.

- Retail and discretionary consumption — Purchasing power erodes as inflation eats into income.

- Airlines and transportation — Fuel costs feed directly into operating expenses.

- Banking — Net interest margins (NIM) compress as deposit rates rise faster than lending rates.

Capital flows are shifting — don't be on the wrong side

Stagflation does not happen overnight, but the warning signals are unmistakable. Core CPI at 3.74% shows price pressures spreading into the real economy, not just confined to fuel. The VN-Index still rose strongly to 1,672.8 points on March 27VietnamPlus, but capital flows are clearly diverging — concentrated in oil & gas and speculative real estate rather than spread evenly.

The appropriate strategy for this period: reduce exposure to interest-rate-sensitive sectors, increase allocation to energy beneficiaries and defensive plays. Most importantly, watch two key variables closely: developments in Hormuz strait negotiations and the State Bank's policy rate decision in Q2.