Vietnam's SSC Warns Against Tikop, Buff, Topi — What Millions of Investors Aren't Being Told

On March 26, 2026, Vietnam's State Securities Commission (SSC) issued yet another urgent warning about a wave of investment apps operating online. But the real question isn't "which apps were flagged?" — it's "if you lose your money, who will protect you?"

4 Years of Warnings, Apps Still Operating as Usual

What the reports don't make clear is that this is nothing new. Since 2022, the SSC has named a string of apps — Passion Invest, Finhay, Tikop, Infina, Savenow, BUFF — showing signs of operating fund management and portfolio management services without proper licensing.Thanh Nien

Warnings have been repeated continuously for 4 years. Yet these apps have continued to attract millions of users.Nguoi Quan Sat Tikop alone has over 1.5 million users, while Finhay has recorded over 2.7 million — mostly young people and new investors, with minimum investments as low as 50,000 VND (about $2).

The Legal Gray Zone — Where the Real Risk Lies

The latest warning on March 26, 2026 targets Tikop, Buff, Topi and similar platforms.Thời báo TCVN According to the SSC, these companies raise capital from investors through cooperative investment contracts (BCC), then entrust fund management companies to invest in financial products.

The critical point: this activity falls outside the SSC's regulatory scope and licensing authority. If disputes arise, investors will not be protected under securities law.

These apps operate under cooperative investment contracts governed by the 2015 Civil Code — not the Securities Law. The platform acts as an intermediary distributing contracts, while a separate legal entity (usually a fund management company) manages the capital. Investors contribute money and receive returns based on contractual ratios.

But who bears the loss when this model collapses?

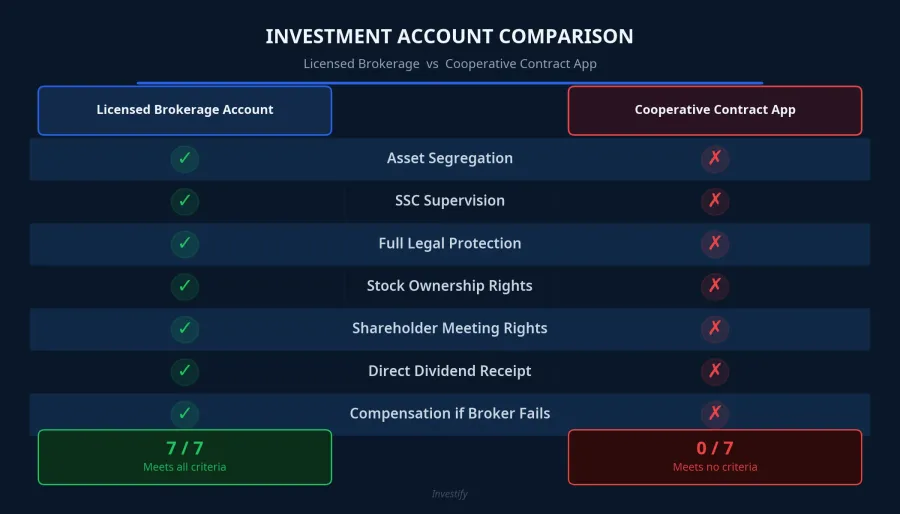

The Core Difference: Brokerage Account vs Investment App

When placed side by side, the differences between the two models are alarmingly clear:

- Funds are not held in the investor's name

- No asset segregation mechanism — money is pooled under the representative's name

- No SSC supervision

- Disputes are governed only by Civil Law rather than Securities Law

The Passion Invest Lesson — History Could Repeat Itself

In 2018, Passion Invest poured capital into VPB stock and suffered losses of hundreds of billions of VND.Tin nhanh CK The company once advertised "20 million VND/year x 10 years x 20% returns = 623 million VND" — figures that the SSC said could mislead investors.

The biggest risk? The chance of recovering your money is extremely low. Investors can only protect their interests through civil litigation — a process that is lengthy, expensive, and dependent on whether the violating party still has any assets.

What Investors Should Do Right Now

The SSC's recommendations are clear:

- Verify licensing on the official portal before depositing money

- Only transfer funds to accounts matching the legal entity named in the contract — never send money to personal accounts

- Keep complete records: contracts, transfer receipts, transaction history

- Thoroughly research the business model and profit-sharing mechanism before investing

A Fragile Line

Not every fintech app is a scam. However, Vietnam's regulatory framework for fintech remains incomplete, making the line between legal and illegal operations extremely thin.

What the reports don't say — but investors need to understand — is this: clearly distinguish between investing through a licensed securities company (with asset segregation, supervision, and legal protection) and investing through intermediary apps using civil cooperative contracts (no segregation, no supervision, no protection).

The question isn't "will this app make me money?" — it should be "if I lose my money, who will protect me?"