When the Market Ignores the Warning Signs

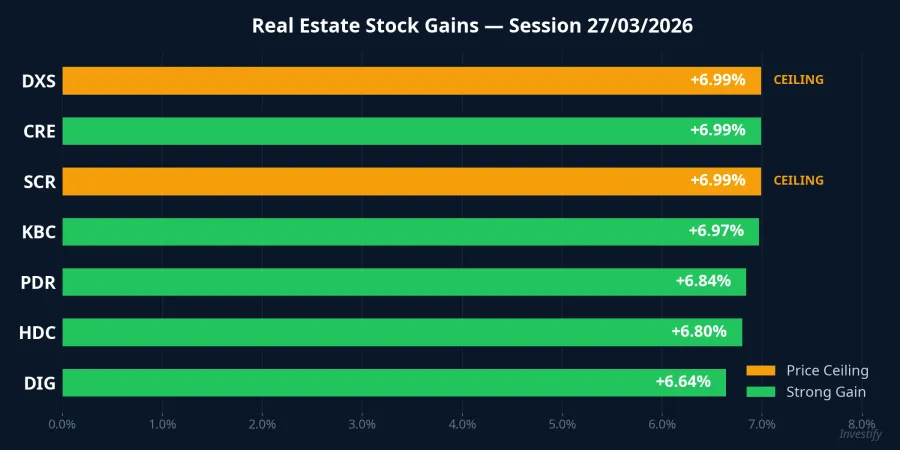

The March 27, 2026 session was exactly the kind that lures retail investors in. VN-Index surged 28.17 points (+1.71%) to 1,672.8, with real estate stocks stealing the spotlight as 13 tickers simultaneously hit price ceiling.Thoi bao Tai chinh

KBC gained 6.97%, CRE surged 6.99%, PDR rose 6.84%, DIG climbed 6.64%, HDC jumped 6.8%. DXS and SCR both locked at ceiling. Liquidity exploded: DXG led the entire market with over 41.7 million shares matched, PDR hit 26.4 million, DIG reached nearly 24.7 million. Total HOSE trading value reached approximately 23,270 billion VND.

But what the reports don't spell out — who is actually driving prices, and does this rally have any foundation beyond herd mentality?

Domestic Retail Investors Lead, Foreign Funds Stay Selective

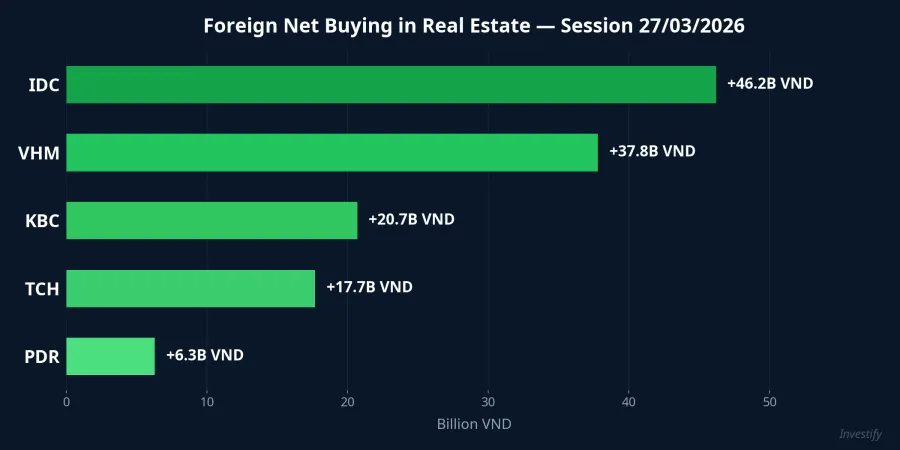

Foreign investors net sold approximately 155 billion VND on HOSE during the March 27 session.CafeF However, within the real estate sector, they deployed capital selectively: net buying IDC (+46.2B VND), VHM (+37.8B), KBC (+20.7B), TCH (+17.7B), and PDR (+6.3B).

The real risk lies here: the force pushing dozens of mid and small-cap stocks to ceiling doesn't come from institutional funds — it comes from domestic retail investors. When DXS and PDR hit ceiling, the spillover effect dragged IDJ, SDU, PLA, NHA, and VHD along for the ride. This is a textbook sign of short-term speculative waves.

A Dangerous Contradiction: Money Flows Against SBV Policy

This is the most concerning part. While money floods into real estate stocks, the State Bank of Vietnam is simultaneously tightening credit to this very sector with aggressive measures:Bao Dau Tu

- Growth cap: real estate credit growth at each bank cannot exceed that bank's overall credit growth rate.

- Quarterly limits: outstanding loans in the first 3 months cannot exceed 25% of the annual target.

- Higher risk weights: luxury and speculative segments now face 40–56% risk weights.

- LDR adjustment: Treasury deposits excluded from the denominator, forcing banks to limit risky lending.

- Portfolio target: maintain real estate exposure at 24–25% of total outstanding loans.

In plain terms: the SBV is channeling capital toward social housing and genuine demand while restricting luxury, resort, and speculative segments. The market's money is betting against policy.

Why Is Money Still Pouring In?

Four factors explain why money is "front-running policy":

- Deep discount valuations: many real estate stocks have dropped 30–50% from their peaks, creating expectations of technical recovery. CRE bounced from 6,830 to 7,650 in 10 sessions, DIG from 13,450 to 14,450.

- Legal expectations: three new laws (Land, Housing, Real Estate Business) are taking effect, opening expectations of regulatory breakthroughs for frozen projects.

- Short-term speculation: as market liquidity improves sharply, hot money naturally seeks mid-cap real estate names with high volatility.

- Selective foreign deployment: KBC benefits from FDI and industrial park expectations, VHM attracts buying thanks to strong fundamentals.

But who bears the cost when speculative waves break? The answer is always late-arriving retail investors.

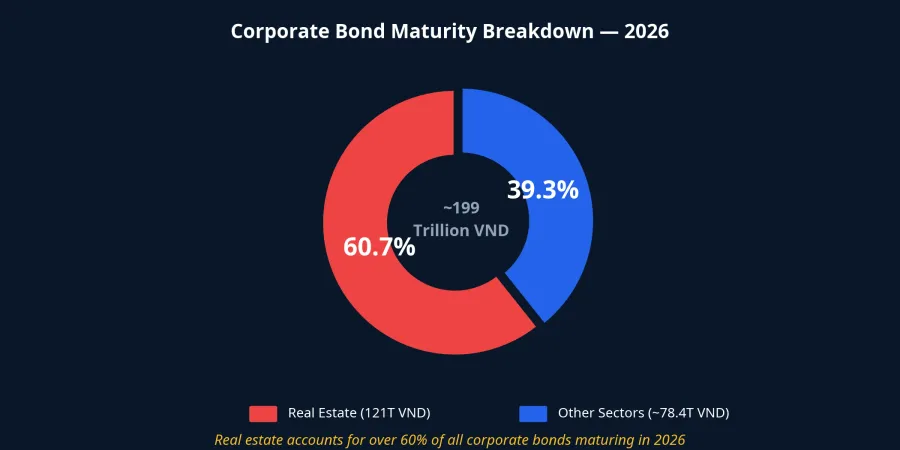

The 121 Trillion VND Bond Maturity Wall — The Risk Nobody Talks About

A fact most investors overlook: in 2026, real estate corporate bonds maturing total approximately 121 trillion VND — accounting for over 60% of all corporate bonds maturing this year.CafeF Pressure concentrates in Q2 and Q4.

With bank credit tightened, bond rollovers becoming difficult, and lending rates potentially rising 0.5–0.7% per year — real estate companies face dual pressure from both funding sources. In Q1 2026, the wave of bond payment deferrals has already spread widely.

A Warning Signal from the Market Itself

One detail many overlook: during the March 27 session, banking stocks — traditionally an early indicator for credit flows — did not rally alongside real estate. Market history shows that when banks are weak while real estate is strong, this is typically a sign of short-term speculative waves, not sustainable uptrends.

The market's money is front-running policy. But when policy catches up, who will be left holding the bag?

What Should Investors Do?

- Short-term: if participating in the real estate wave, prioritize high-liquidity names (PDR, DIG, KBC, DXS), set tight stop-losses since the rally is primarily sentiment-driven.

- Medium-term: focus on sector leaders with healthy financials (VHM, KDH, NLG) — benefiting from legal reforms and genuine housing demand.

- Long-term: closely monitor Q2–Q3 real estate credit quotas, legal progress on major projects, Q4/2026 bond maturity deadlines, and lending rate developments.

The rational strategy is to ride the momentum while never ignoring macro risks — especially when real estate credit remains tightly controlled and the 121 trillion VND bond maturity wall is closing in.