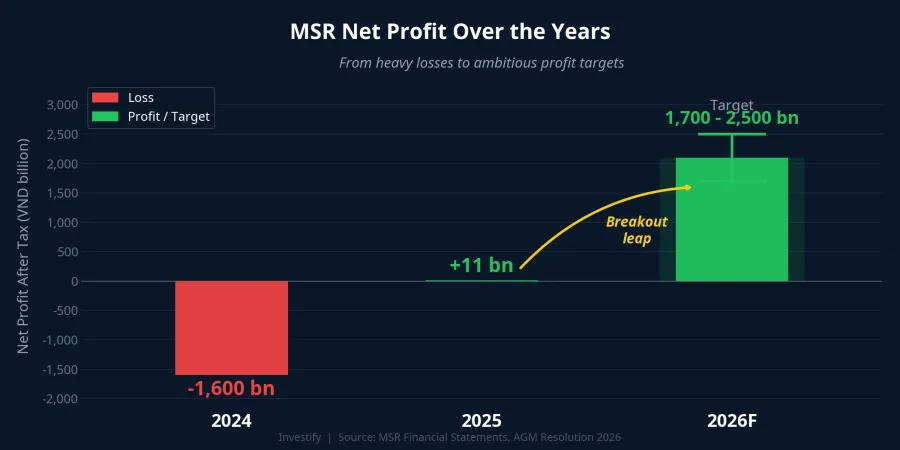

Looking at the numbers, Masan High-Tech Materials' (MSR) 2025 story is shocking in both directions. The company posted a mere VND 11 billion in full-year net profit — hard to believe for an enterprise that owns the world's largest tungsten mine outside China. Yet for 2026, management has set a net profit target of VND 1,700–2,500 billion, an increase of hundreds of times.CafeF

What stands out: this target is not wishful thinking. It is built on an assumed APT (ammonium paratungstate) price of just 1,080–1,325 USD/MTU — less than half the current market price.

From Billion-Dollar Losses to a Record Q4

Throughout 2023–2024, MSR was deep in the red — losing nearly VND 1,600 billion in 2024 alone. The turning point came in the second half of 2025 as international tungsten prices began surging.

2025 Financial Results:

| Metric | Figure |

|---|---|

| Full-year revenue | VND 7,443 billion (+18.8%) |

| EBITDA | VND 2,175 billion (+22%) |

| Full-year net profit | VND 11 billion |

| Q4/2025 net profit | VND 222 billion — highest since 2022 |

| Tungsten segment revenue | VND 4,458 billion (+33%) |

Q4/2025 delivered VND 222 billion in net profit — the highest since 2022Vietnambiz, signaling that the "engine" has truly started. The reason full-year profit was only VND 11 billion was the burden of accumulated financing costs from prior periods — not because core operations were weak.

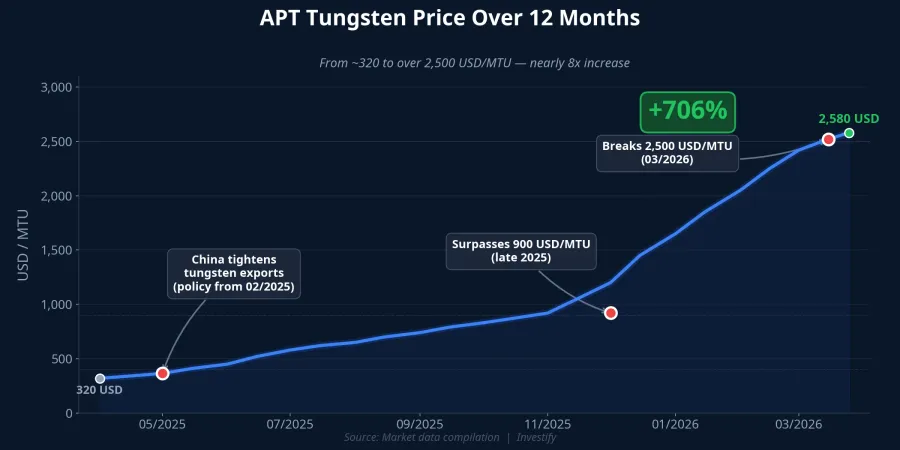

Tungsten Prices Up 706% — The Rally Shows No Signs of Cooling

The biggest driver behind MSR's story is the global mineral war. APT prices surged approximately 557% since China imposed export controls in February 2025Yahoo Finance, and by March 2026 had broken through 2,500 USD/MTU — a historic record.Fili

The supply-demand picture tilts heavily in MSR's favor:

- China controls 82% of global tungsten production and nearly 90% of APT processing capacity. Export quotas for H1 2026 were cut another 12% year-over-year.Dai bieu Nhan dan

- The US imposed a 25% tariff on Chinese tungsten, driving up import costs.

- Defense demand is forecast to grow 12% in 2026 — tungsten is essential for weapons and ammunition manufacturing.

Nui Phao Mine — An Irreplaceable Strategic Asset

The Nui Phao mine in Thai Nguyen province — with reserves of 66 million tons of ore, accounting for roughly 33% of tungsten reserves outside China — is becoming a strategic asset of international significance.

MSR's competitive advantages:

- Fully integrated value chain: From mining to deep processing (APT, tungsten oxide, carbide powder) — selling high-value products rather than raw ore.

- Low-cost producer: One of the lowest-cost producers globally.

- Multi-product: Beyond tungsten, the mine also produces fluorspar, bismuth, and copper.

- Long mine life: Expansion plans extend operations through 2036.

As the US, Europe, and Japan are forced to reduce dependence on China, Nui Phao becomes one of very few alternative sources with sufficient scale. Combined with plans to transfer the listing from UPCoM to HOSECafeF, MSR is positioning itself as a future "mineral blue-chip."

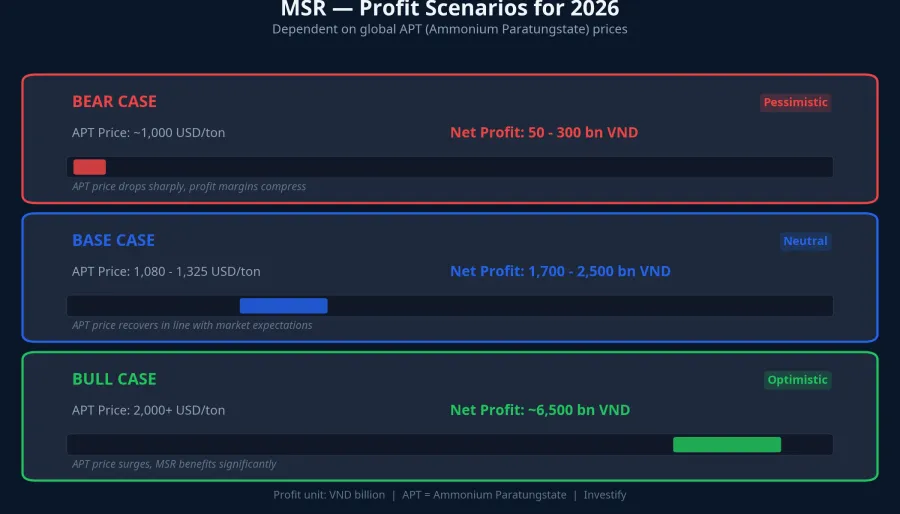

Three Profit Scenarios for 2026

The most notable detail in this financial report: the VND 1,700–2,500 billion target is built on an assumed APT price of just 1,080–1,325 USD/MTU — less than half the current market price.

If APT prices hold around 2,000 USD/MTU, estimated profits could reach VND 6,500 billion — nearly three times the upper target. This is why MSR stock has risen approximately 148% over the past 12 months, with market capitalization exceeding VND 53,000 billion (nearly USD 2 billion).

Where Does the Real Risk Lie?

The numbers look attractive, but investors need to stay clear-headed about three major risks:

1. Complete dependence on tungsten prices. If China relaxes export controls or trade negotiations progress, APT prices could drop sharply. In the bear case, MSR's profit falls to just VND 50–300 billion — a massive gap from the best-case scenario.

2. Expectations are already priced in. With a 148% gain over 12 months, any negative signal — a tungsten price correction, production falling short of targets — would create significant downward pressure.

3. Geopolitical risk cuts both ways. The trade war is both an opportunity and a risk. China could release strategic reserves to crash tungsten prices at any time.

Conclusion

MSR is in the most favorable position in its history: record tungsten prices, China restricting supply, the West needing alternative sources, and Nui Phao being virtually the only option at scale. The growth story is real.

But investors should clearly distinguish between "a good company" and "a good price." With MSR's market cap already approaching USD 2 billion, the margin of safety has narrowed considerably. This is a highly cyclical stock — suited for investors who understand commodity price volatility, not for a "buy and forget" strategy.