Here's what the earnings report won't tell you: a company with excellent business performance can become a liquidity trap for minority shareholders. DHG Pharma (HoSE: DHG) is the clearest proof of this right now.

DHG — A Pharma Blue-Chip That Suddenly Lost Its Public Company Status

On March 25, 2026, DHG Pharma officially announced it no longer meets the requirements for public company status under Vietnam's 2019 Securities Law.MekongASEAN

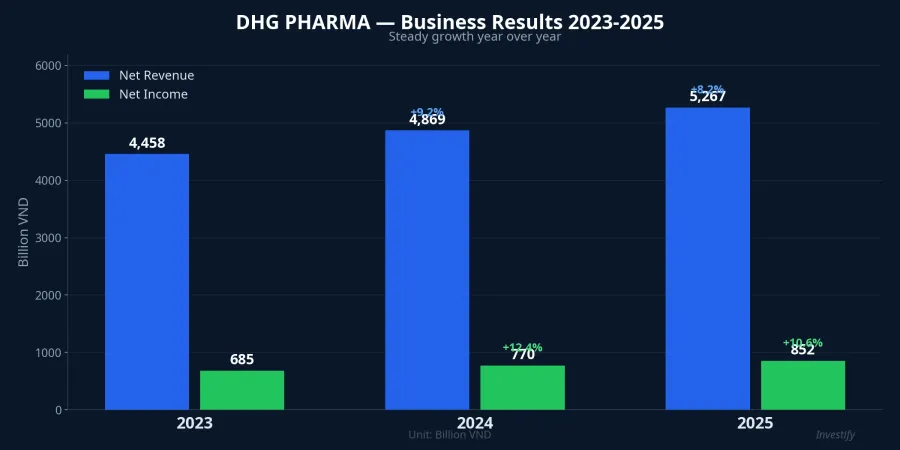

By the numbers, DHG is anything but weak: net profit of VND 852 billion in 2025, revenue exceeding VND 6,000 billion, and a 100% cash dividend — that's VND 10,000 per share. Trading at around VND 100,800, this stock has long been a favorite among pharmaceutical investors.

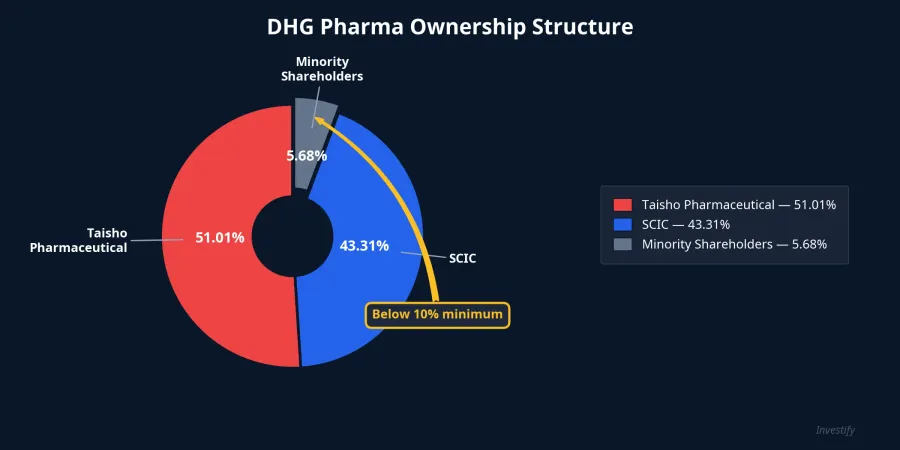

But who's paying the price? The 4,183 minority shareholders who collectively hold just 5.68% of the company — well below the 10% legal minimum.

Taisho's Decade-Long Acquisition: How Free Float Got Squeezed to Nothing

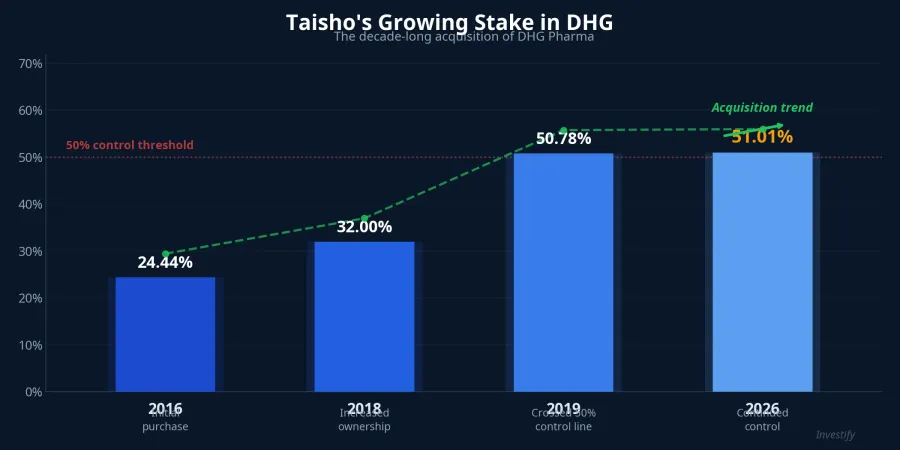

The real risk lies in a systematic, patient acquisition strategy. Japan's Taisho Pharmaceutical — a century-old pharma giant — steadily increased its DHG stake across three major phases:

- July 2016: Taisho invested approximately $100 million to acquire 24.44% of DHG at a 20–30% premium to market price.VnExpress

- 2018: Raised ownership to 32% after DHG lifted its foreign ownership cap.

- 2019: Launched a public tender offer for 20.6 million additional shares, pushing ownership above 50.78%. DHG officially became a Taisho subsidiary.

Throughout this process, SCIC maintained its 43.31% stake and has no divestment plans. Under the 2026–2030 strategy, SCIC will keep its DHG holding unchanged. The "lockup" by two major shareholders has crushed the free float to alarming levels.

Legal Consequences: One Year to Fix It or Leave the Exchange

Under Article 32 of the 2019 Securities Law, a public company must have at least 10% of voting shares held by a minimum of 100 non-major shareholders. DHG has only 5.68%.

The company has a maximum of one year to remedy the situation. If it fails, the consequences are severe:

- Loss of public company status

- Delisting from HoSE

- End of mandatory financial disclosure

DHG says it's working with Taisho and SCIC on a remediation plan, expected to be discussed at the April 21, 2026 general meeting. But the question remains: do two shareholders controlling 94.32% of the company truly want to solve this problem?

Minority Shareholders — "Passengers Without Seats"

If DHG gets delisted, over 4,000 shareholders will face three serious risks:

- Frozen liquidity: Once off the main exchange, trading becomes nearly impossible.

- Loss of information access: The company would no longer be required to publish periodic financial reports.

- Neutralized voting rights: With 94.32% held by two major shareholders, all resolutions are decided without meaningful minority input.

The painful irony: DHG continues to perform excellently — net revenue of VND 5,267 billion, profit growth of 9.4%Kinh te Do thi, with a 2026 target of VND 1,007 billion in pre-tax profit. Investors are being pushed out not because the company is failing — but because it's so attractive that it got fully absorbed.

The Public Company Crisis Is Spreading

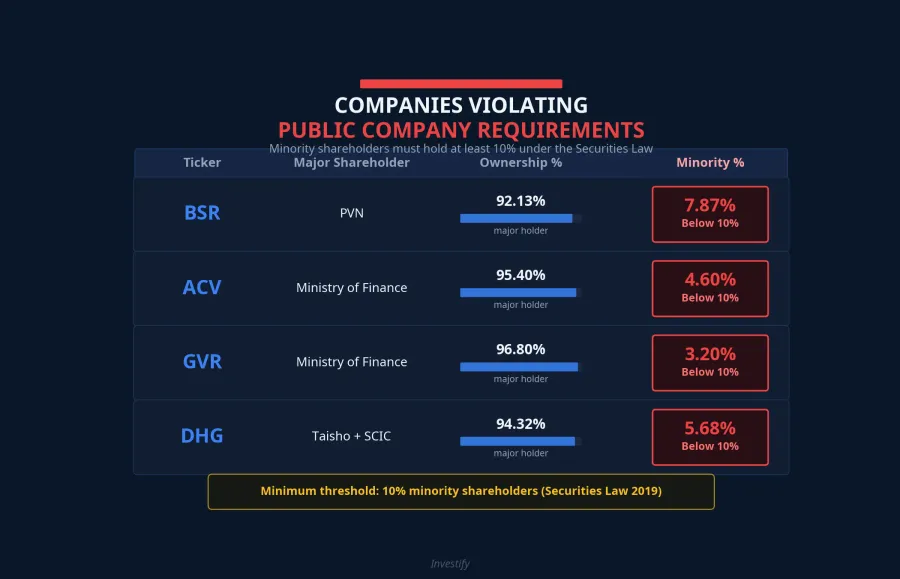

DHG is not alone. In March 2026, multiple major companies found themselves in the same predicamentDan Viet:

- Binh Son Refining (BSR): PVN owns 92.13%, putting over 56,000 shareholders at risk.Znews

- Airports Corporation of Vietnam (ACV): Ministry of Finance holds 95.4%.

- Vietnam Rubber Group (GVR): Ministry of Finance owns 96.8%.

- BIDV (BID): State Bank of Vietnam 79.7%, KEB Hana Bank 14.8%.

The State Securities Commission has launched a broad review, confirming this is a systemic issue — not just isolated cases.

Remediation Options: A Nearly Unsolvable Problem

To raise the minority shareholder ratio from 5.68% above 10%, at least one major shareholder would need to sell approximately 4.32% of shares. But:

- SCIC selling down? Aligns with state divestment policy, but the 2026–2030 strategy doesn't include DHG on the divestment list.

- Taisho selling down? Highly unlikely after spending hundreds of millions of dollars over 10 years to achieve control.

- Issuing new shares? Would dilute both parties' ownership and requires mutual consent — essentially a non-starter.

Lessons for Investors

The DHG story is a clear warning: strong business performance doesn't guarantee a safe investment. When major shareholders acquire enough to crush the free float, minority shareholders become "passengers without seats" on their own flight.

If you hold stocks where foreign or state ownership exceeds 80%, ask yourself: do you truly own something, or are you sitting on a chair that's about to be pulled away?