On March 26, 2026, fertilizer stocks exploded across the trading board — DCM up nearly 7%, DPM up nearly 6%, BFC up nearly 7%. Year-to-date, BFC has gained over 40%, DCM nearly 20%, DPM over 12%. The crowd is euphoric, money pouring in.

But who gets hurt buying at the top?

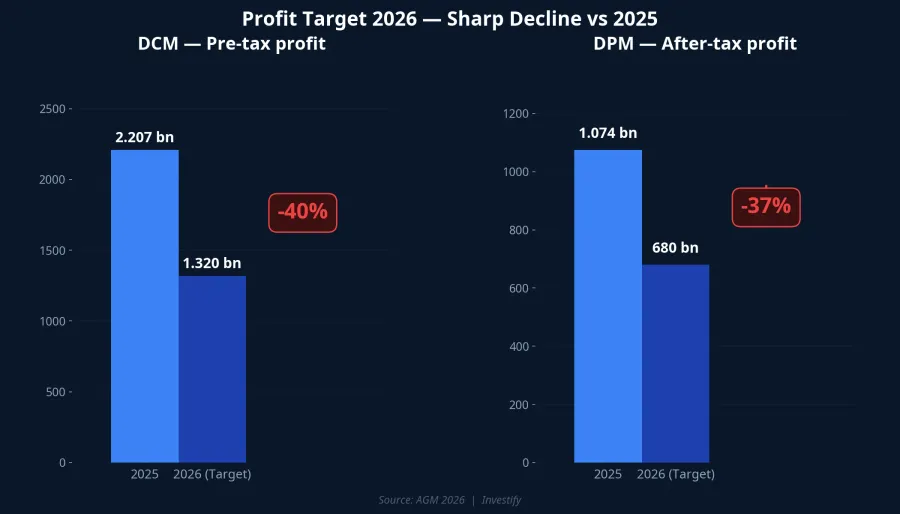

What the reports don't tell you: the management of both DCM and DPM — the people who understand these businesses better than anyone — have set 2026 profit targets 37-40% lower than last year. That's not a signal to ignore.

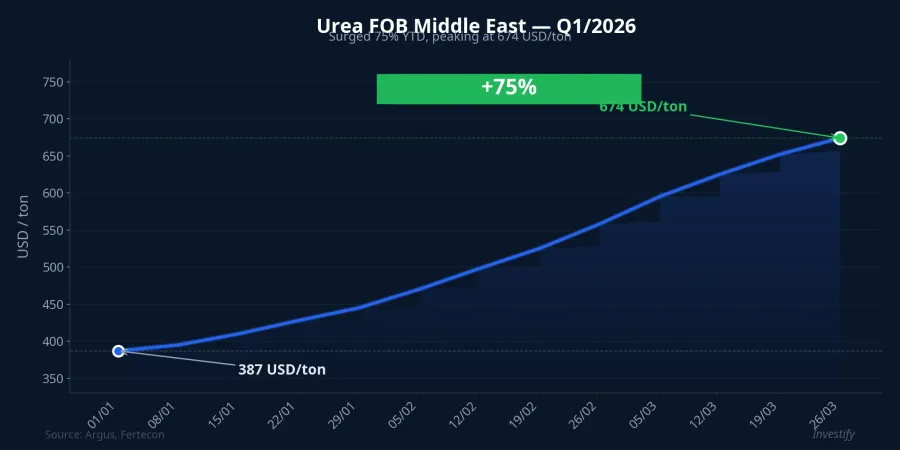

Urea Prices Up 75% — The Hormuz Strait Story

International urea prices (FOB Middle East) surged from around 387 USD/ton at end-2025 to 674 USD/ton by mid-March 2026 — a roughly 75% increase.Vietstock

The direct cause? Military conflict at the Strait of Hormuz — a shipping route carrying nearly half of global urea exports. This coincided with spring fertilizer season in the Northern Hemisphere, creating a perfect storm of surging demand and prices.

The crowd's logic is simple: urea prices spike, fertilizer companies profit, stocks must rise. But the real risk lies elsewhere.

What Does Management Say? Profit Targets Plunge

In stark contrast to market euphoria, management at both industry leaders have set unusually cautious 2026 targets:

Ca Mau Fertilizer (DCM): In 2025, pre-tax profit hit a record 2,207 billion VND on revenue of nearly 16,961 billion VND.VnEconomy But the 2026 plan? Revenue up slightly to 17,615 billion VND, while pre-tax profit drops to just 1,320 billion VND — down 40%.Nguoi Quan Sat Dividend payout is also expected to halve from 20% to 10%.

Phu My Fertilizer (DPM): In 2025, revenue exceeded 16,000 billion VND with after-tax profit of approximately 1,074 billion VND.Vietstock The 2026 plan: revenue of 17,600 billion VND but after-tax profit of only 680 billion VND — down roughly 37%.CafeF

The key question: why would revenue rise while profits fall so sharply?

Three Reasons Margins Are Getting Squeezed

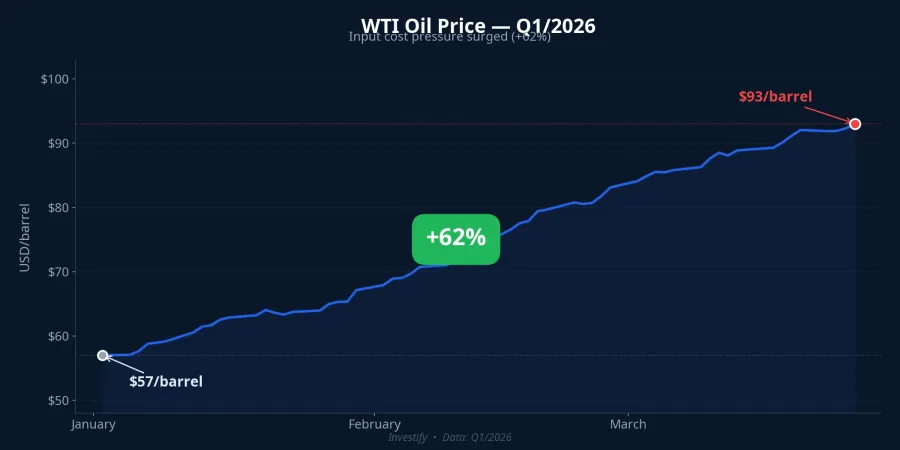

1. Natural gas input costs track oil prices

Natural gas — the primary raw material for urea production — is priced at roughly 46% of Singapore fuel oil. When WTI oil prices surged from $57/barrel to $93/barrel in Q1/2026 (up over 62%), gas input costs rose in lockstep.

Rising urea prices boost revenue, but costs climb just as fast. Profit margins narrow significantly, especially during periods when oil prices outpace urea. Estimates suggest a 20% oil price increase could reduce DPM's pre-tax profit by over 30%.Elibook

2. Urea prices could cool rapidly

Current urea prices sit at conflict-driven peaks — they could reverse quickly if geopolitical tensions ease. MB Securities forecasts full-year 2026 average urea prices could return to the 400-450 USD/ton range, far below the current 674 USD/ton.

Management builds plans on full-year average prices, not short-term peaks. They understand what the crowd is overlooking.

3. VAT 5% benefit — already priced into 2025

The 5% VAT policy on fertilizers (effective July 1, 2025) allowed companies to claim input tax credits, saving an estimated 200 billion VND for DCM and 400 billion VND for DPM. However, this benefit was fully reflected in 2025 results and is no longer a new growth driver for 2026.

Lessons from Oil & Gas Stocks — A Familiar Pattern

This paradox is nothing new. Just weeks earlier, Brent crude rose 45% but oil and gas stocks like GAS and BSR fell 30%. Same story: commodity prices surge on short-term geopolitics, input costs and operational risks follow, eroding actual profits.

Fertilizer stocks are repeating this exact pattern: prices rise first, risks arrive later.

Who Should Investors Listen To?

Actual benefit depends on profit margins, not just revenue. When management themselves target 37-40% profit declines, that's a signal deserving respect.

- Short-term trading: Urea prices pull stocks up on sentiment. Profits are possible if you exit in time, but risk is very high when the conflict cools.

- Long-term investing: Must be based on actual profits and management guidance. A 40% profit decline target is as clear a warning as it gets.

In the battle between "the optimistic market" and "the cautious insiders," history shows the insiders are usually right. The real risk is this: who are you listening to — the trading board, or the people signing the financial statements?