The bigger picture shows the market is sending two conflicting signals in a single trading session. VN-Index surged powerfully, yet behind that bright green board is an interest rate race that has only just begun.

March 25 Session: A Sea of Green, but Foreign Investors Keep Selling

VN-Index closed the March 25, 2026 session at 1,658 points, jumping 43.42 points (+2.69%) — its strongest session in two weeks.VnExpress Market breadth was overwhelmingly positive: 276 stocks advanced versus just 60 decliners, with all 21 sector groups in the green. HOSE turnover reached nearly VND 23 trillion, 10-15% higher than the previous session.

The main drivers came from large-cap stocks. VIC alone contributed 7.82 points and VHM added 4.66 points — these two Vingroup stocks pulled the index up by over 12 points. The power sector group including NT2, REE, PC1, TV2, TTA, and GEG all hit their ceiling prices.Vietnambiz

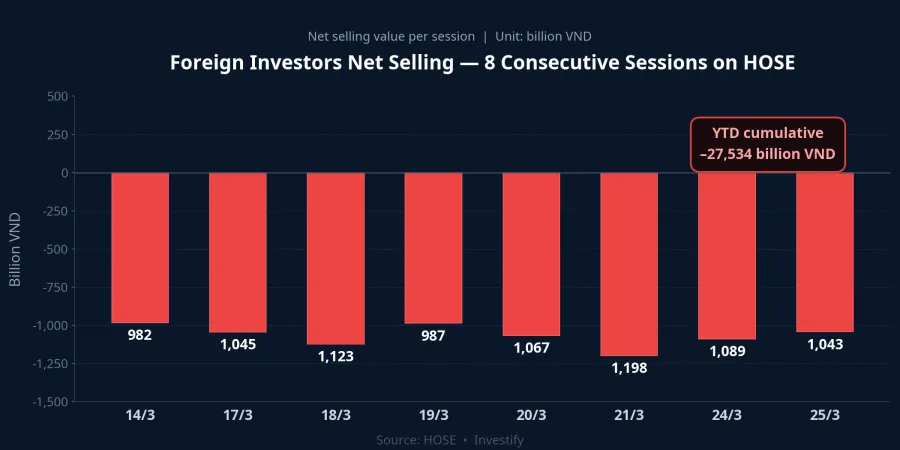

However, capital flows are moving in a worrying direction. Foreign investors continued net selling roughly VND 1 trillion on HOSE alone — marking the 8th consecutive session. Year-to-date, foreigners have withdrawn over VND 27.5 trillion, equivalent to approximately USD 1.1 billion.

The Interest Rate Race: Big 4 Banks Join In

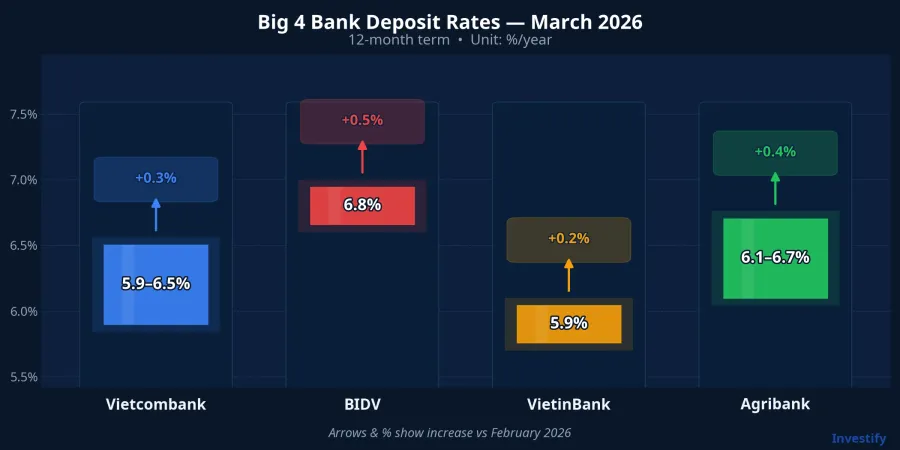

On March 25, all four state-owned banking giants simultaneously raised deposit rates:Dan Tri

- Vietcombank: 12-month term up to 5.9%/year; 24-month term increased by 1 percentage point to 6.5%/year.

- BIDV: Highest listed rate at 6.8%/year for 12-month terms and above.

- VietinBank: Maintained 5.9%/year for 12-18 month terms.

- Agribank: Raised 24-month term by 0.7 percentage points to 6.7%/year.

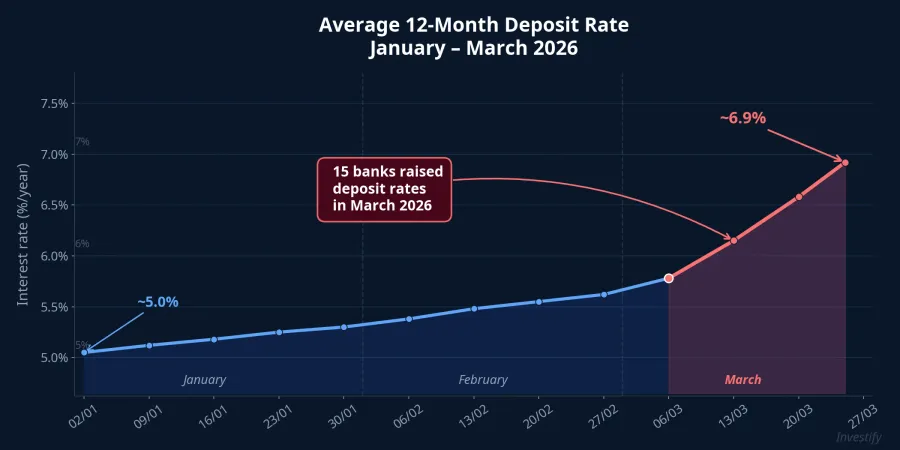

Since early March, 15 banks have raised deposit rates.VnEconomy Cake by VPBank even reached 9%/year for 10-36 month terms.VietnamNet The core reason: deposit growth of just 0.8% significantly lagged credit growth of 1.4% in the first two months of the year — forcing banks into a race for deposits.

The Paradox: Markets Surge While Risks Quietly Accumulate

Capital flows are shifting, and rising interest rates create three major pressures investors should not ignore:

First, money is being pulled back toward savings deposits. When 12-month deposit rates commonly range 6-7%/year, the yield spread between equities and deposits narrows significantly. For many cautious investors, this is reason enough to reallocate assets.

Second, corporate borrowing costs will rise. Lending rates lag deposit rates by 1-2 quarters. Real estate, construction, and highly leveraged companies will face margin compression in the second half of 2026.

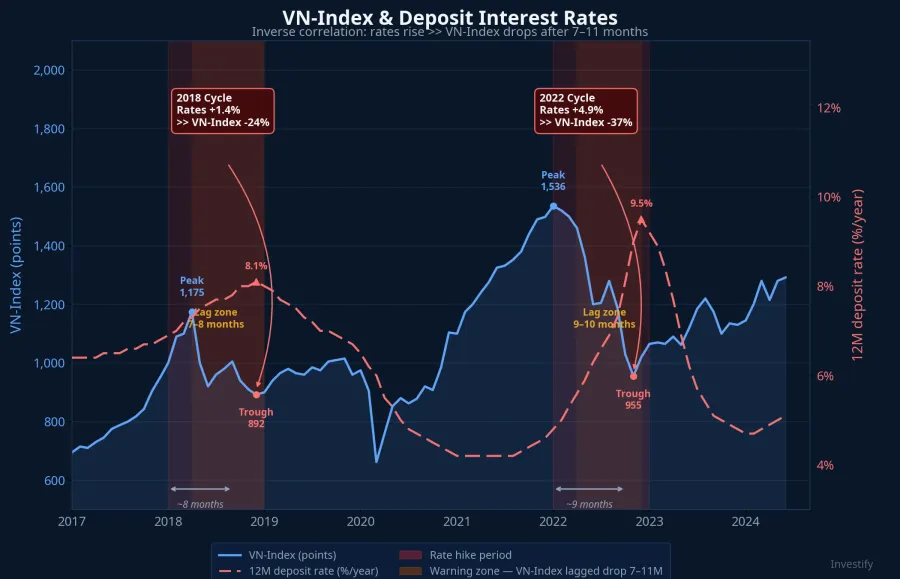

Third, history provides a clear warning. The interest rate hike cycles of 2018 and 2021-2022 both led to deep VN-Index corrections with a 7-11 month lag. An additional rate increase of 1-1.2% could push the index into high-risk territory in the latter half of 2026.

Power Sector Hitting Ceiling Prices: Real Opportunity or Short-Lived Wave?

The power sector's fundamentals are solid: national electricity demand is projected to grow 11-12% in 2026; REE targets tripling capacity by 2030; PC1 holds a record backlog exceeding VND 7.5 trillion; NT2 offers an expected dividend yield of 9.8%.

However, performance has been uneven. REE, GEG, and TTA gained 6-10% in March, but NT2, PC1, and TV2 experienced correction phases. The ceiling-price surge on March 25 was largely driven by technical factors and AGM season expectations. TV2 trades at a P/E premium to the sector average, warranting caution.

Sector Divergence and Strategy in a Rising Rate Environment

In a rising rate environment, the divergence between sector groups will become increasingly pronounced:

- Beneficiaries: Banking (widening net interest margins), insurance (improved investment yields), cash-rich companies.

- Under pressure: Real estate, construction, discretionary consumer spending, and companies with large short-term borrowings.

January 2026 CPI rose 2.53% year-on-year, with core inflation at 3.19%. The Ministry of Finance's three inflation scenarios for 2026 range from 3.6-4.6%,Government Portal indicating very limited room for monetary easing.

The March 25 session was a positive short-term signal, but do not let one green day obscure the reversal in interest rate trends. Prioritize fundamentally strong banking stocks, exercise caution with highly leveraged companies, and be selective with power sector trades. The 8-session consecutive net selling streak by foreign investors is a warning signal that should not be ignored.