Ask most individual investors in Vietnam why they are still holding equities when valuations are no longer cheap, and the answer tends to orbit the same assumption: the Fed will cut rates in the second half of 2026, the dollar will weaken, and global capital will rotate back toward risk assets and emerging markets. That assumption is not unreasonable. The Fed has held rates steady in the 3.5–3.75% range for several consecutive meetings, and the April policy statement still contained the phrase “easing bias”: language the market read as confirmation that cuts remained on the table.

The detailed minutes of that same meeting, published on the evening of May 20 U.S. time by the Federal Reserve, tell a different story entirely.Fed

The Sentence That Changed the Calculus

Bloomberg, CNBC, and several major wire services highlighted the same passage from the minutes:CNBC

“A majority of participants highlighted that some policy firming would likely become appropriate if inflation were to continue to run persistently above 2 percent.”

The operative word is “firming”: additional tightening, not a hold. This marks the first time since the tail end of the 2023 rate-hike cycle that FOMC minutes have used this verb in a forward-action sense, signaling that a hike is a live option, not just a theoretical backstop.

The same minutes also noted that “several” participants wanted to drop the “easing bias” language from the official statement outright at the April meeting itself. In other words, the very phrase the market has been clinging to as evidence that cuts are coming was already considered outdated by a significant internal faction, even at the time of the meeting.

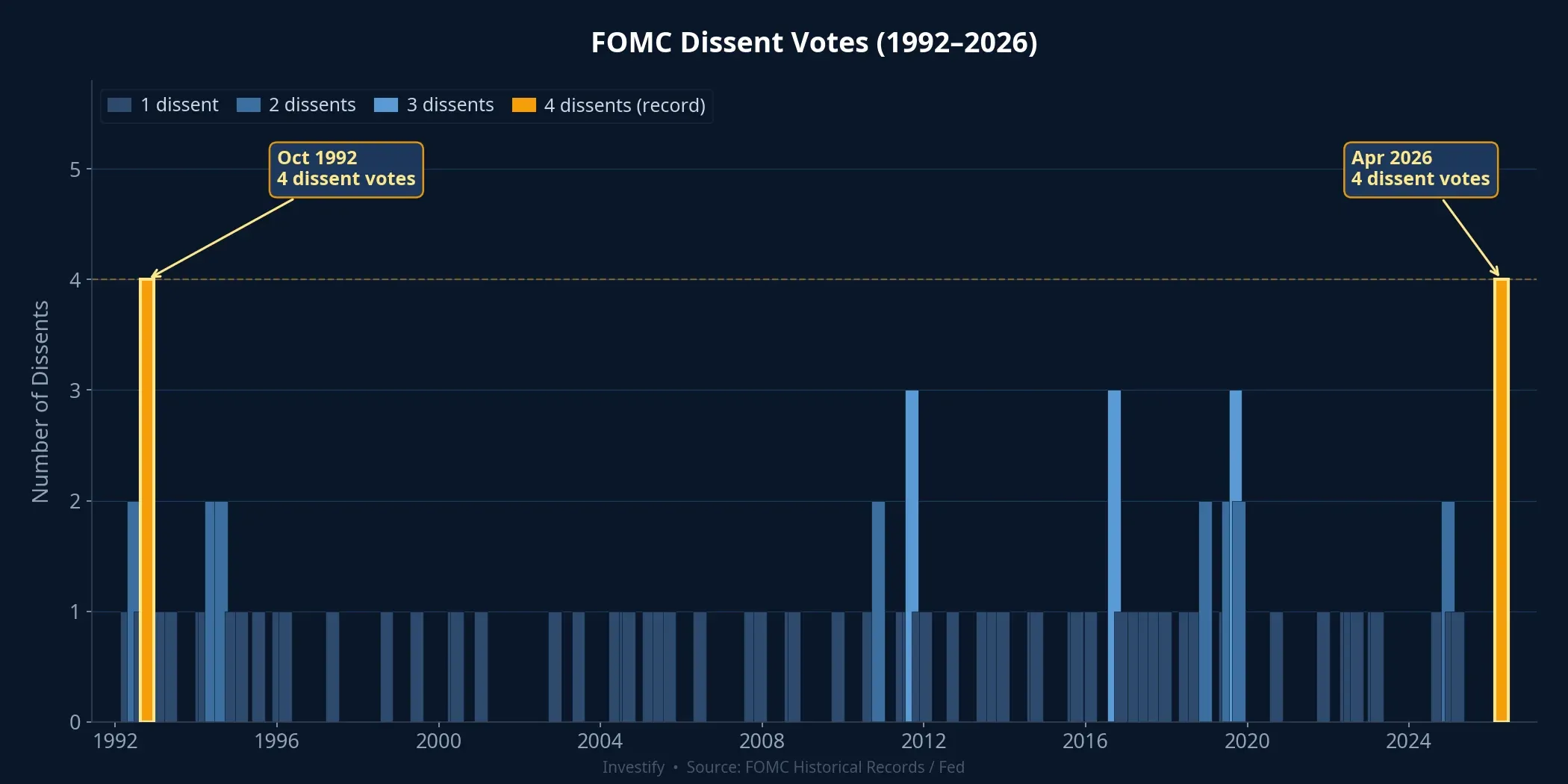

Four Dissents: The Most in 34 Years

The April 28–29 meeting concluded with an 8–4 vote to hold rates steady. Four dissenting votes is the highest level of internal disagreement since October 1992, nearly 34 years ago.CNBC What makes the split particularly notable is that the four dissents came from two opposing directions.

On the hawkish side, three regional Fed bank presidents: Beth Hammack (President, Federal Reserve Bank of Cleveland), Neel Kashkari (President, Federal Reserve Bank of Minneapolis), and Lorie Logan (President, Federal Reserve Bank of Dallas). All three objected because they wanted the “easing bias” language removed, arguing that it no longer reflected inflation realities. On the dovish side: Stephen Miran, Governor of the Federal Reserve, dissented in the opposite direction, advocating for an immediate 25-basis-point cut at this very meeting.

When four dissents split between the two extremes, the real signal is not generic disunity. It is that the gap between two competing inflation narratives inside the Committee has widened materially. The hawks are worried that the Iran energy shock is keeping inflation persistently elevated. The doves are worried that holding rates too long will fracture the labor market. Neither camp believes in the “everything is self-correcting” scenario that markets have been pricing in.

How Iran Changed the Equation

Before Iran closed the Strait of Hormuz in late February, U.S. core inflation was tracking toward the 2% target. After the oil shock, most inflation measures have exceeded 3%, and the minutes note that officials expect elevated energy prices to continue putting upward pressure on inflation in the near term.Fox Business

This is the crux. Before Iran, falling inflation was the market’s baseline, and Fed rate cuts were the natural consequence. After Iran, inflation staying above 3% is the Fed’s own baseline. Further tightening has been named as an option in the minutes, even if it has not yet become an action. These two scenarios imply two very different portfolio postures.

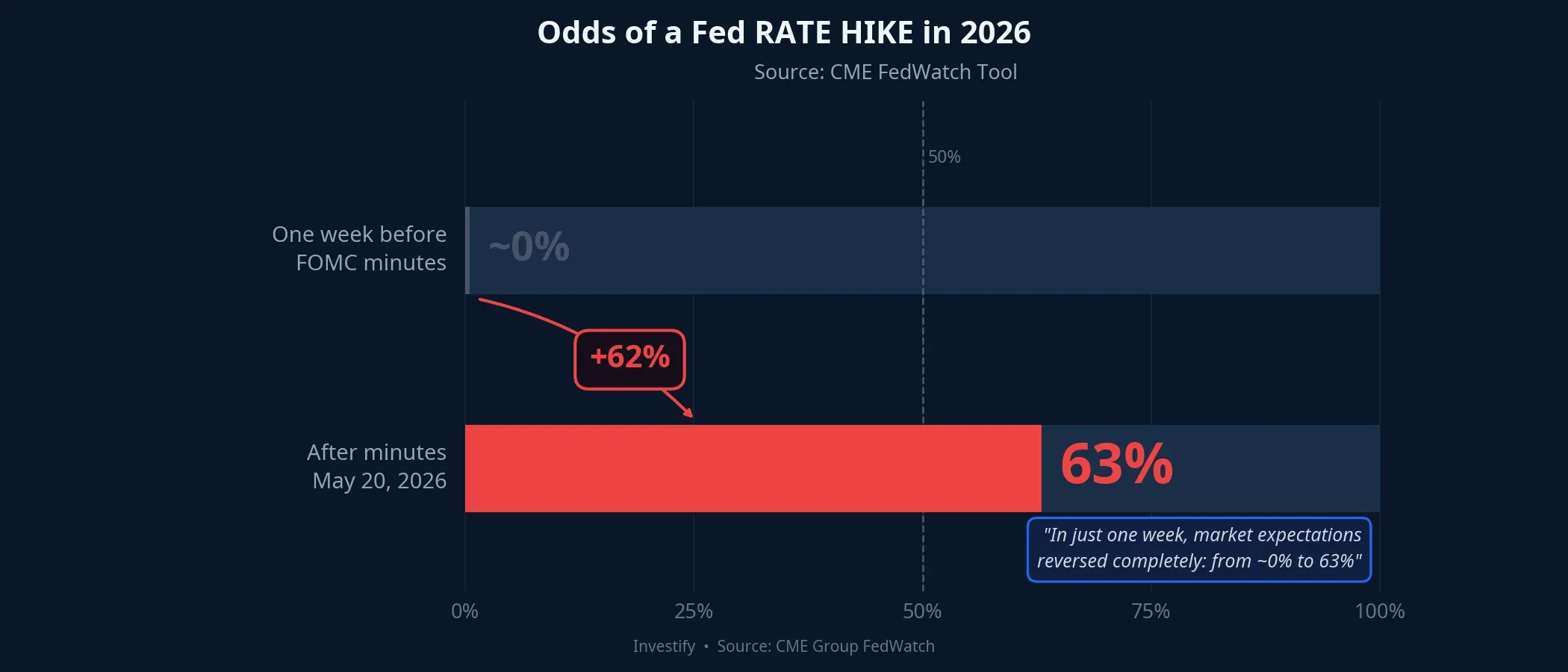

How the Markets Repriced: CME FedWatch

The most striking development came from interest rate futures markets. Following the minutes release, according to the CME FedWatch Tool, traders raised the implied probability of at least one Fed rate hike in 2026 to approximately 63%. One week earlier, that figure was close to zero.CNBC

For the specific June meeting, expectations still lean toward a hold (roughly 70%), with a minority pricing in a cut (roughly 28%). Markets are not yet pricing a hike at the next meeting, but they are pricing the possibility of a hike sometime this year. This means the “Fed cuts H2/2026” thesis — which had been serving as a key psychological support for high-valuation equity portfolios — is no longer the market’s sole base case.

Two Transmission Channels to Watch in Vietnam

When expectations of Fed tightening re-emerge, capital flows into emerging markets typically pause. For Vietnam specifically, there are two concrete transmission channels worth monitoring.

The exchange rate channel. The USD/VND rate was trading around VND 26,367 on May 20, near multi-year highs. If the Fed tightens further, pressure on the dong persists, making it harder for the State Bank of Vietnam to ease domestic policy even if it wants to support growth. The 12-month deposit rate at Vietnam’s Big 4 state-owned banks currently sits at 5.9% per annum, and room for further cuts is narrowing in this environment.CafeF

The risk-asset valuation channel. On May 21, the VN-Index closed at 1,896.89 points, down 16.34 points from the prior session, with 171 tickers declining versus 145 advancing, on the day following the overnight FOMC minutes release. The U.S. 30-year Treasury yield is hovering around 5.18%, a 19-year high. With the global risk-free rate anchored at that level, the hurdle for justifying elevated equity valuations rises accordingly.

Rethinking the Portfolio Thesis

If the “Fed cuts H2/2026” scenario has been the primary load-bearing column in a high-valuation equity position, now is the time to stress-test that column.

High-growth and technology stocks trading at forward P/E multiples of 20-plus tend to be the most sensitive to changes in the risk-free rate. When U.S. rates stay higher than expected for longer, those valuations become difficult to sustain unless earnings growth actually fills the discount gap. This is precisely why stocks with genuine free cash flow and stable dividends are more resilient in this environment: their intrinsic value does not depend heavily on a lower discount rate arriving on schedule.

On the fixed-income side, 12-month deposits at the Big 4 currently offer 5.9% per annum, while fixed-income products from reputable distributors are yielding roughly 7–11% per annum, depending on the issuer. In a scenario where the Fed holds or tightens further, these instruments offer a more attractive risk-adjusted return relative to high-valuation equities waiting for a rate-cut catalyst that may not arrive on the old timeline.

This is not a call to sell equities. It is a call to stress-test the thesis. If the reason for holding equities was “the Fed is about to ease,” that reason just weakened materially. The replacement thesis needs to be grounded in concrete corporate earnings growth. Macro expectations that are actively shifting cannot carry the weight.

Three Data Points to Watch Before the June Meeting

Three pieces of incoming data will determine which scenario prevails over the coming weeks.

Core PCE inflation for May (released in late June): if it stays above 3% rather than drifting back toward 2.5–2.8%, the hawkish bloc on the FOMC gains additional firepower to push for further tightening.

Developments at the Strait of Hormuz and Brent crude: if geopolitical escalation with Iran pushes oil back toward $110 per barrel, the case for persistently elevated inflation strengthens.

Fed Chair remarks ahead of the June 16–17 meeting: whether the language around “policy firming” reappears in any public speech. The last time the Fed used this terminology consistently before a meeting, markets repriced before the official decision was announced.

Until these three data points resolve, the rational base case for Vietnamese investors is not “the Fed will cut soon.” The evidence-consistent base case is that the Fed will wait for more data, and that the probability of a hike in 2026 is no longer zero. Portfolios built on the old macro expectation need a new load-bearing column.